Choosing the right mortgage broker software in 2025 can transform your business. Compare LOS, CRM, PPE, and POS tools to find the perfect match for your workflow.

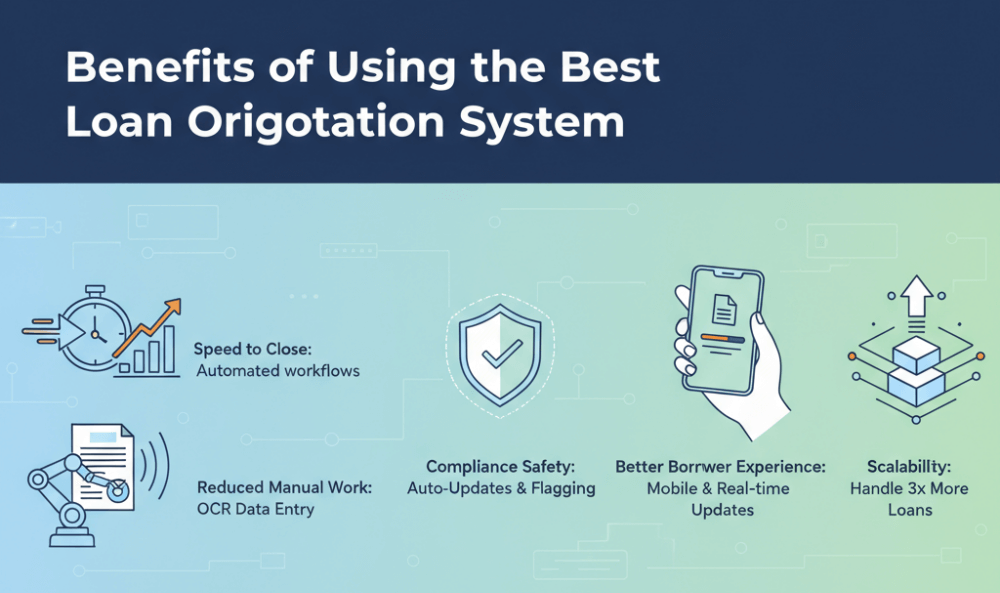

An outstanding mortgage software solution can deliver comprehensive improvements for mortgage brokers. Through process automation and end-to-end standardization, it significantly reduces document processing time, accelerates loan approvals, and minimizes manual input errors and compliance risks. By centralizing client and business data management, it also streamlines team collaboration and enhances customer relationship management efficiency.

For a mortgage broker, a high-quality software platform can not only improve operational efficiency but also increase loan approval rates.

So, what features should an excellent mortgage broker tool include?

Core Systems and Platform Support

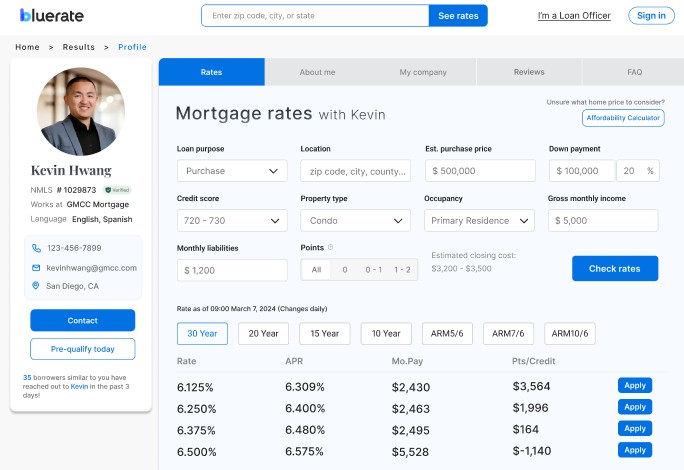

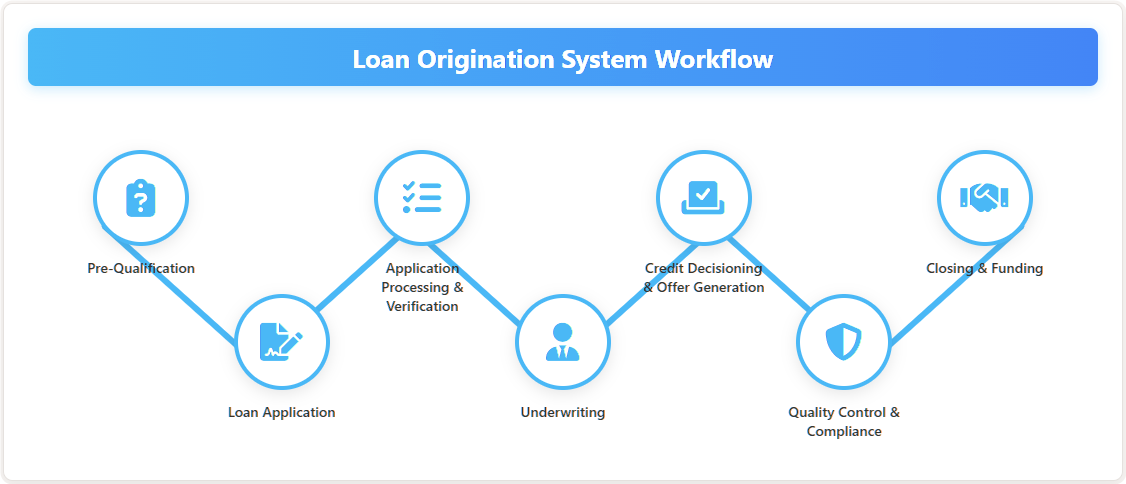

An effective mortgage broker platform connects its core systems so the entire lending journey flows without friction. The Loan Origination System (LOS) oversees every stage—from the initial application and underwriting to document processing and final closing—while the Point of Sale (POS) portal offers borrowers a simple, modern way to apply online, upload required documents, and check their progress anytime. All client data is organized within the Customer Relationship Management (CRM) system, which also automates communications and reminders to keep deals moving forward. Working in sync, the Product & Pricing Engine (PPE) instantly compares rates and loan products from multiple lenders, enabling brokers to deliver the most competitive options to their clients.

Automation and Efficiency Tools

Advanced automation features streamline operations so brokers can handle more deals in less time. Application and pre-approval automation enables borrowers to complete applications in just minutes, achieving over a 90% completion rate, with built-in income and DTI calculations and instant pre-approval letter generation. Document processing with OCR automatically collects, recognizes, and verifies files, then produces standardized 1003/FNM 3.4 forms without manual input. Meanwhile, workflow automation handles task reminders, status updates, and condition checks, ensuring every step moves forward smoothly and nothing slips through the cracks.

Compliance and Knowledge Management

Built-in compliance and knowledge tools help brokers stay ahead of complex regulations and product guidelines. An AI-powered loan guide delivers instant answers across programs including Fannie Mae, Freddie Mac, FHA, VA, USDA, and Non-QM, reducing the time spent searching through manuals. For enterprise teams, a customizable rules engine allows the creation of tailored compliance logic and pricing rules, ensuring every loan meets both regulatory requirements and internal business standards.

Client Engagement and Experience Enhancement

A well-designed platform elevates the borrower experience while helping brokers build stronger relationships. The borrower portal provides real-time rate quotes, affordability calculators, and full process transparency so clients always know where they stand. Automated communications send timely reminders and status updates at key milestones, keeping borrowers informed without adding to the broker’s workload. To support growth, personalized websites and marketing tools give loan officers their own branded site and lead-generation resources, helping them attract, engage, and convert more clients.

Data and Analytics Capabilities

Robust data tools give brokers the insights they need to work smarter and grow faster. A loan tracking dashboard provides real-time visibility into each loan’s progress while automatically prioritizing daily tasks for maximum efficiency. For business growth, the Growth Hub offers lead-generation and market-connection features, helping brokers identify new opportunities, expand their network, and drive consistent pipeline growth.

Scalability and Integration

A versatile platform supports a wide range of loan types—including Conventional, FHA, VA, USDA, Jumbo, Non-QM, and commercial loans—to meet diverse business needs. It also integrates seamlessly with third-party systems such as pricing engines, e-signature solutions, and credit reporting services, ensuring brokers can build a connected, end-to-end workflow without sacrificing flexibility or performance.

Although there are many Mortgage Broker Tools on the market, very few mortgage software solutions truly meet the real needs of mortgage brokers. We’ve conducted an in-depth review of the 10 most popular Mortgage Broker Tools—let’s find out which one is the best fit for you.

List of the Best Mortgage Broker Tools for 2025

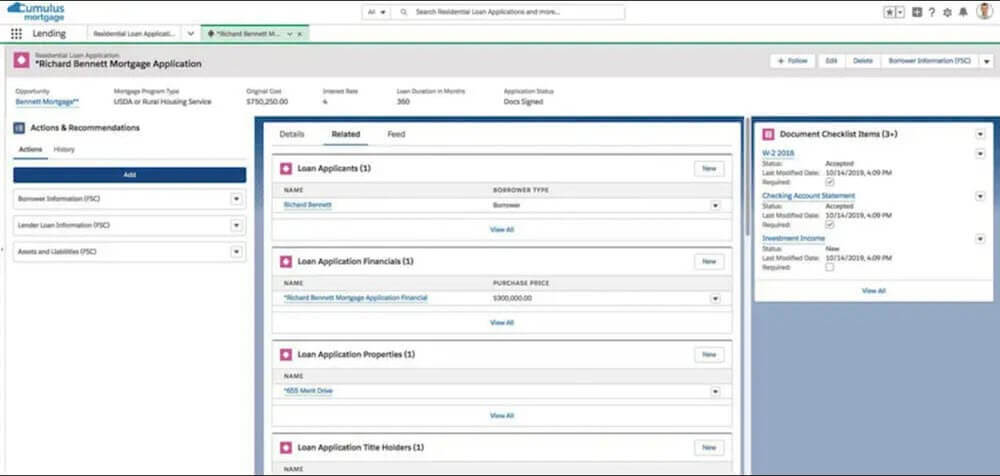

Encompass

Encompass is an end-to-end LOS designed for retail, wholesale, and correspondent lending. It consolidates application intake, underwriting, closing, and secondary market delivery into a single platform.

Key features: Loan underwriting, full origination and servicing tools, POS and PPE integration, document management with e-signature, analytics, secondary market delivery, API-based workflow customization.

Pros: All-in-one design eliminates the inefficiencies of juggling multiple systems. Automation and compliance tools improve throughput without sacrificing accuracy. Flexible integrations adapt to different lending models.

Cons: Steeper learning curve and higher implementation costs than lighter LOS options. Some users note a dated interface.

Pricing: Typically $500–$1,000 per user/month (“per user + per loan” model). No free trial; demos available.

Calyx Point

A long-standing LOS for mortgage brokers and small lending teams, Calyx supports the full loan process from application to closing.

Key features: Pipeline tracking, document storage, borrower templates, e-signature, audit trail, reporting, underwriting automation, integrations with 200+ vendors including Salesforce.

Pros: Easy to learn, familiar workflow, and affordable for small brokerages.

Cons: Outdated interface, not fully cloud-based, occasional delays in compliance updates.

Pricing: Estimated $300–$500 per user/month. No free trial; demos available.

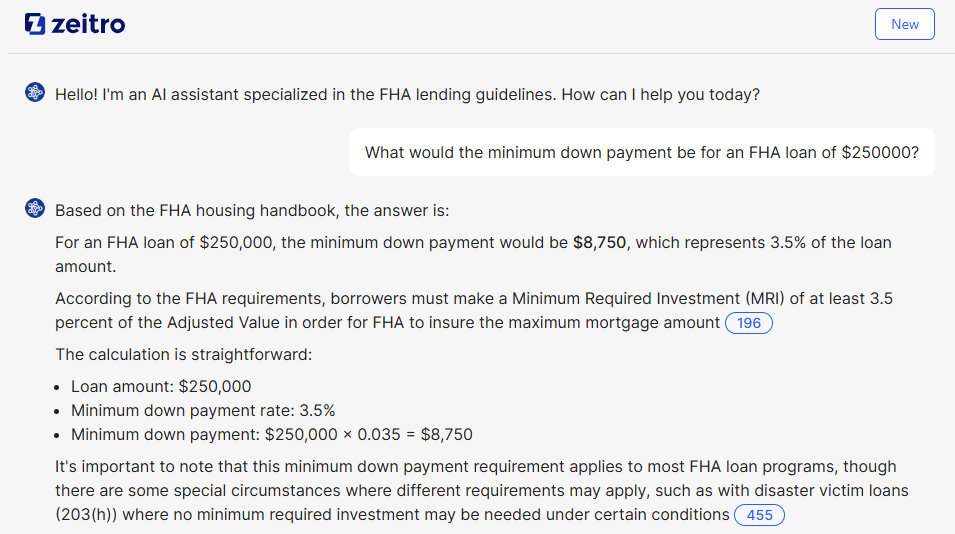

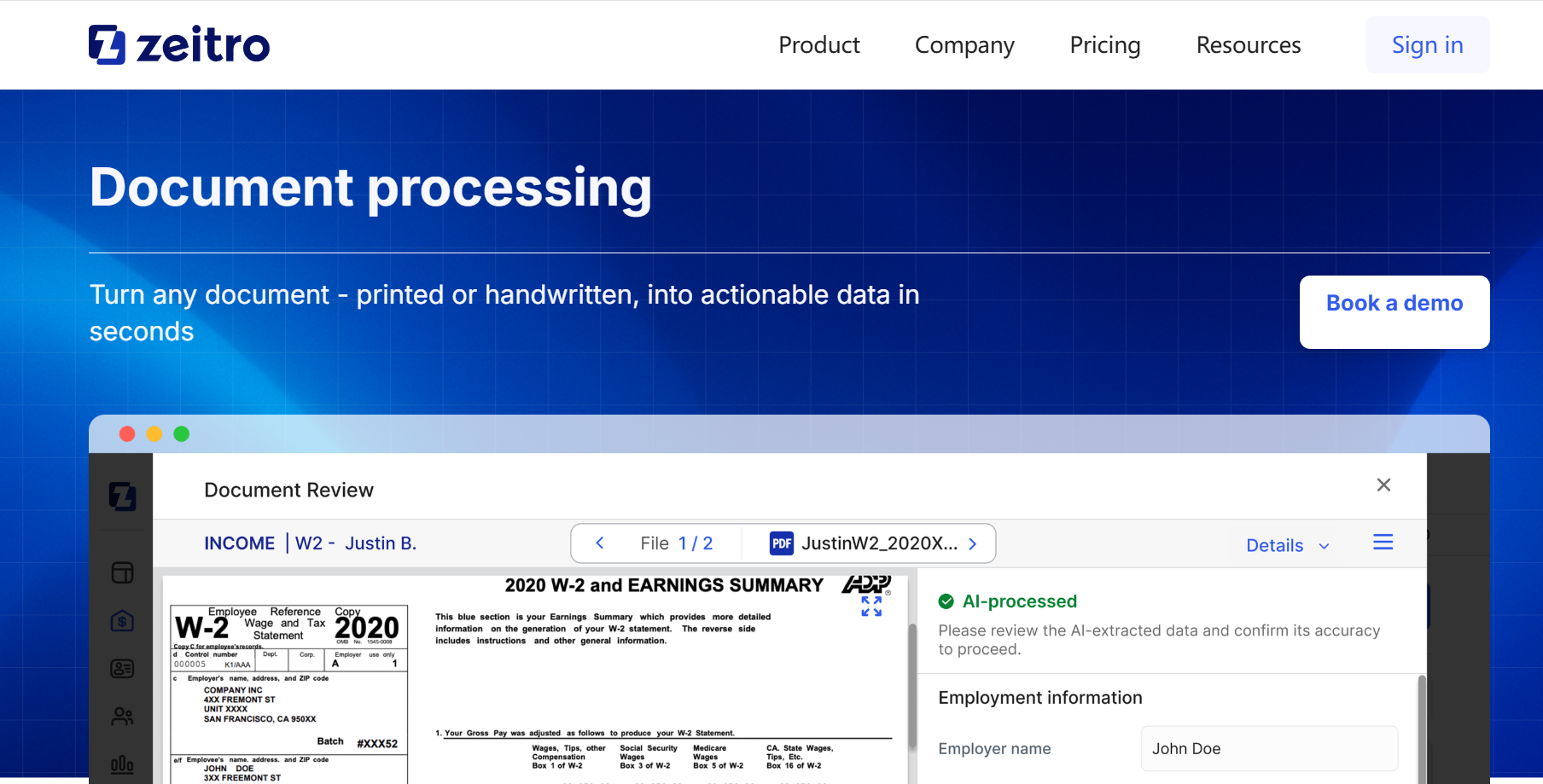

Zeitro

An AI-native, all-in-one mortgage platform built for brokers, loan officers, and mortgage companies.

Key features: AI-driven application processing, real-time pricing engine (30+ lenders), GuidelineGPT for compliance, AI document verification, borrower and LO portals, lead generation tools, SOC 2–grade security.

Pros: Mobile-first borrower experience, automation enabling higher loan volumes, AI tools reducing errors and compliance burdens.

Cons: May require workflow adjustments for legacy system integration.

Pricing:

- Explorer: Free for life

- Individual: $8/month per LO

- Business: $35/month per company

- Enterprise: Custom pricing

Blue Sage

A fully cloud-based lending platform unifying origination and servicing with configurable workflows and API-first design.

Key features: LOS, digital servicing platform, consumer POS, broker and LO portals, workflow automation, pricing engine, role-based security, Fannie Mae Income Calculator integration.

Pros: Multi-channel lending, high speed and security, productivity gains up to 85%, flexible customization.

Cons: Newer in the LOS market, limited public case studies, learning curve for legacy system users.

Pricing: Not publicly disclosed; contact vendor.

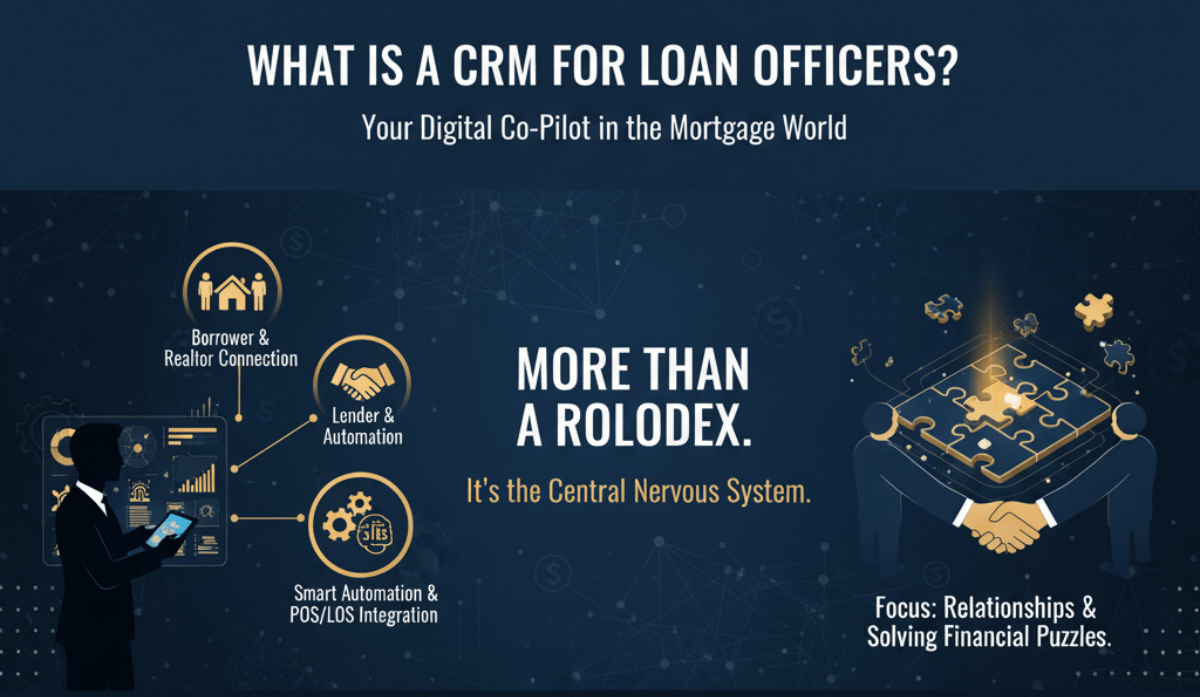

BNTouch Mortgage CRM

A mortgage-specific CRM and marketing automation platform.

Key features: Email/SMS automation, video marketing, borrower POS, prebuilt templates, lead management, follow-up automation, digital 1003 support, LOS integrations.

Pros: Mortgage-focused interface, strong automation, effective client engagement tools.

Cons: Can be overwhelming at first, dated interface elements, occasional lag.

Pricing:

- Individual: $165/user/month + activation fee

- Team: $190/month for 2 users + $95/additional user

- Enterprise: Custom pricing

No free trial; demos available.

MeridianLink Mortgage

A cloud-native LOS for banks, credit unions, and mortgage lenders.

Key features: Loan origination, borrower/agent portals, POS, pricing engine, automated underwriting, e-doc generation, vendor integrations with 250+ partners, open API.

Pros: Comprehensive automation, broad integrations, strong customer support.

Cons: High starting cost (~$20,000), some dated UI elements.

Pricing: Starts at ~$20,000. No free trial; demos available.

TurnKey Lender

An AI-powered platform covering origination, underwriting, servicing, and collections.

Key features: Instant AI credit decisioning, configurable workflows, multi-product lending, risk management, multilingual support, open API integrations.

Pros: Unified lending cycle, highly customizable, strong analytics.

Cons: Complex reporting, advanced customization can raise costs.

Pricing: Starts at ~$500/month; free trial available.

LendingPad

A modern, cloud-based LOS for brokers, lenders, and credit unions.

Key features: Multi-user processing, borrower POS, wholesale integration, advanced document management, real-time notifications.

Pros: User-friendly, responsive support, excellent document handling.

Cons: Some missing functionality, POS usability issues.

Pricing: Broker Edition ~$40/user/month; no free trial.

Floify

A borrower-focused POS and LOS solution.

Key features: Customizable 1003 application, secure borrower portal, automated notifications, e-signature, multilingual support, broad integrations.

Pros: Simplifies document collection, improves communication, reliable automation.

Cons: Limited mobile app functionality, some dated UI elements.

Pricing: Starts at $79/user/month; enterprise pricing on request.

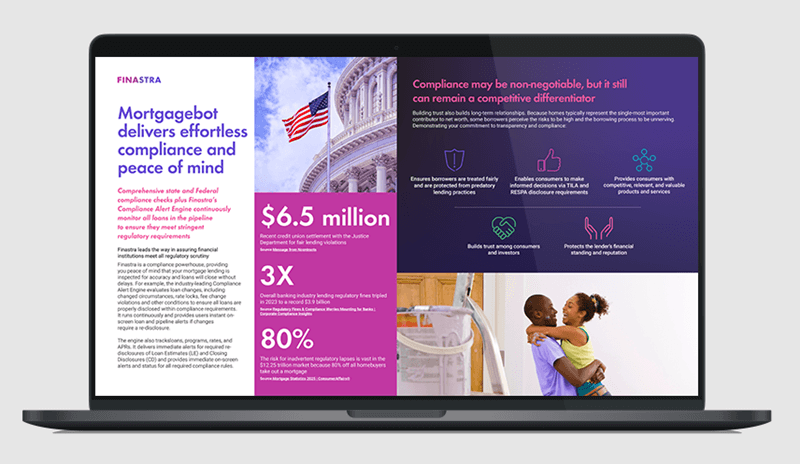

Finastra

A global financial software provider offering end-to-end lending platforms like Mortgagebot LOS.

Key features: Mortgage, commercial, and consumer loan origination; configurable workflows; compliance tools; analytics; FusionFabric.cloud integration.

Pros: Scalable for small to global institutions, strong cloud architecture.

Cons: Can be rigid with non-standard loan products, complex reporting.

Pricing: Custom quotes only.

With so many capable LOS, CRM, PPE, and POS options now on the table, the next challenge is knowing how to pick the one that will truly work for your business. Each platform we’ve discussed has its own strengths and trade-offs—what matters most is aligning those with your operational needs, budget, and growth plans. The following framework will help you make that decision with clarity.

How Should a Mortgage Broker Choose the Right Software?

From the above overview, we now have a clearer picture of these 10 mortgage tools. The next question for brokers is: how do we choose the one that best fits our needs?

1.Define Your Requirements

First, clearly outline your business needs. Map out your workflow, including loan types (FHA Loan, Conventional Loan, VA Loan, etc.), application channels, client base and growth projections, and whether you already have a CRM or LOS system in place. Based on these functional requirements, rank which features are “must-have” and which are “optional.” With that list, you can then choose the mortgage software that best fits your needs.

2.Evaluate User Experience and Technical Compatibility

During the selection stage, don’t just review the feature list—test the software yourself to assess its ease of use and technical compatibility in real-world operations. Below are some common evaluation details we’ve identified.

Hands-on Testing of POS and Back-End Systems

The POS (Point of Sale) interface, as the borrower-facing front end, should ensure that loan applications, document uploads, and progress tracking are intuitive and smooth, while maintaining a consistent experience across different devices. The back-end system should feature a clear menu structure, seamless navigation between functions, and quick-access operations to reduce training costs and enable the team to get up to speed quickly.

Mobile Access and Cross-Device Support

A quality loan software solution should offer a mobile app or responsive web version, allowing loan officers to process applications, respond to clients, and check approval statuses anytime, anywhere. It should also ensure compatibility across platforms such as iOS, Android, Windows, and macOS, preventing usage issues caused by device differences.

Workflow Customization

The system should allow customization of approval steps, application forms, and document checklists to meet specific business needs. For large teams, it should provide multi-level approvals, automated task assignments, and conditional triggers to match loan processes of different scales and models.

Third-Party Integrations

The platform should integrate directly with credit scoring agencies, pricing engines (PPE), e-signature solutions, CRM systems, and accounting software. High integration reduces duplicate data entry, minimizes error rates, and improves overall operational efficiency.

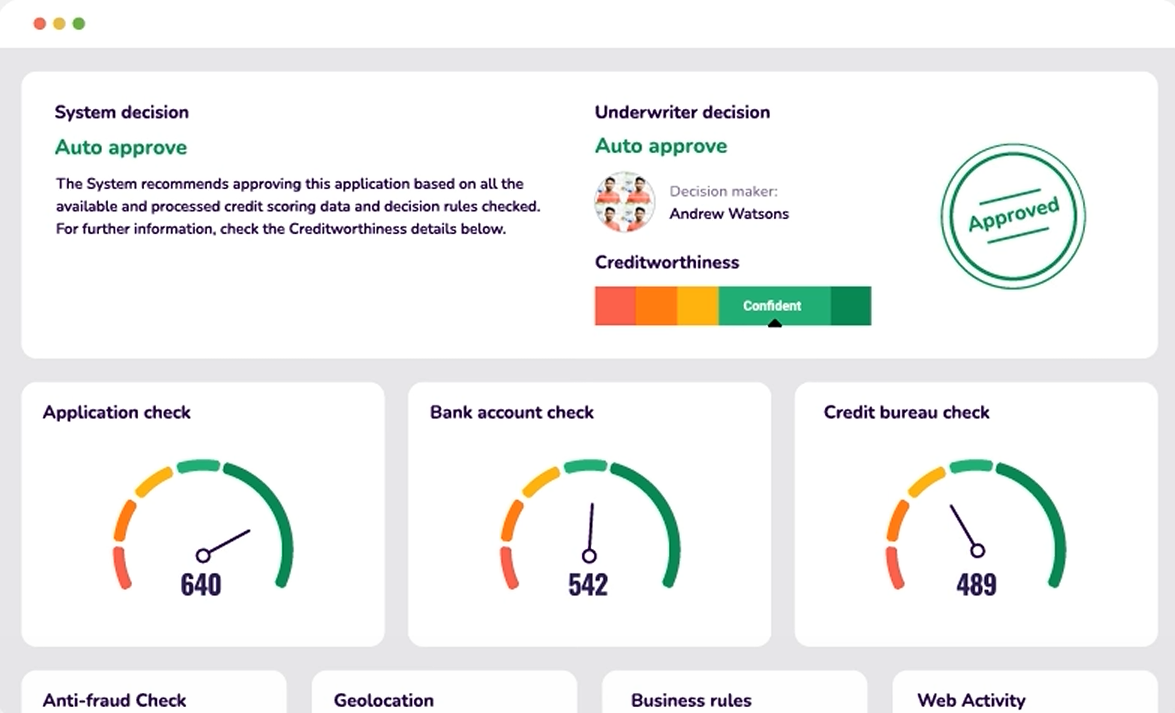

Real-World Testing of Key Features

It’s essential to test the speed and accuracy of automated scoring and decision-making, the efficiency of the approval process, the ease of document management, and whether compliance checks can automatically detect issues and issue timely alerts—ensuring the system truly enhances efficiency and compliance in practice.

Consider Pricing and Affordability

When choosing loan software, brokers and loan officers should view pricing and affordability as one of the key decision factors. Software costs have a direct impact on operating margins and long-term sustainability. As we’ve seen from the overview of the 10 solutions above, pricing varies widely—some platforms may even be prohibitively expensive for certain brokers.

Selecting a reasonably priced, functionally practical solution is therefore critical. In many cases, a SaaS platform with a monthly subscription model is the most suitable option for brokers. This approach allows for flexible, scalable plans that enable cost control during fluctuations in business volume—reducing expenses in slow seasons and scaling up during peak periods—ensuring maximum efficiency in capital utilization.

Why Is Zeitro the Right Choice for Brokers in 2025?

From a functionality standpoint, Zeitro covers every scenario a broker needs. As an all-in-one, AI-powered mortgage platform, it deeply integrates the four core systems—LOS, POS, CRM, and PPE—enabling end-to-end management from lead generation, application, underwriting, and pricing, to loan closing. It streamlines efficiency and accuracy with automated application and pre-qualification, OCR-based document processing, and intelligent task and compliance engines. At the same time, its modern borrower portal, personalized websites, and marketing tools enhance client experience and drive business growth. Zeitro also provides real-time rate comparison, loan progress dashboards, and business analytics, while supporting all loan types and third-party integrations—helping brokers upgrade operational efficiency, client conversion, and market expansion in one unified solution.

From a pricing perspective, Zeitro adopts a SaaS subscription model that’s ideal for brokers. Users can choose a plan that fits their needs or customize a dedicated package. The pricing is highly competitive—paid plans start at just $8 per month, and even the Business version costs only $35 per month—making it affordable for any broker or loan officer. As one of the fastest-growing mortgage software solutions, Zeitro is rapidly capturing market share with its attractive pricing and exceptional product performance.

Among all the options, Zeitro stands out by combining LOS, CRM, PPE, and POS into one AI-powered platform—without the hefty price tag of traditional systems. By closing the gaps left by other tools, it enables brokers to deliver better service, close loans in less time, and grow their bottom line. If you’re ready to outperform the competition, now is the time—start your free trial with Zeitro today.

![[Proven] How to Generate Mortgage Leads for Free? 6 Methods](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69329d01f2ad175a87d0d88b_how-to-generate-mortgage-for-free.png)