When I first considered transitioning into the mortgage industry, my biggest question was simple: how do loan officers actually get paid, and is the income as high as everyone says? If you are looking to change careers or become a licensed loan officer, understanding the commission structure is crucial. Let's dive straight into how much you can realistically earn and how those paychecks land.

Key Takeaways

- Commission Structure: Most loan officers earn a percentage of closed loans, typically ranging from 0.5% to 2.5%.

- Diverse Pay Models: Compensation ranges from pure commission to salary-plus-commission.

- Regulatory Limits: Federal laws prevent pay variations based on loan interest rates.

- Realistic Income: Average annual earnings span from $74,000 to over $180,000 based on loan volume.

Do Loan Officers Get Commission?

Yes, the vast majority of mortgage loan officers are compensated primarily through commissions. In my experience, this commission-driven model is what attracts top-tier talent, as it directly ties your hard work to your earning potential. Depending on the company you work for, you will typically encounter one of three main compensation structures:

- Commission-Only: Common at independent brokerages. You receive no base salary, but you earn the highest possible percentage of the loan amount.

- Salary Plus Commission: Salary, salary-plus-bonus, fixed-per-loan pay, and commission-based models may all be used at banks and credit unions.

- Flat Fee: Some lenders use a fixed amount per loan, and whether that model applies to junior originators depends on the employer.

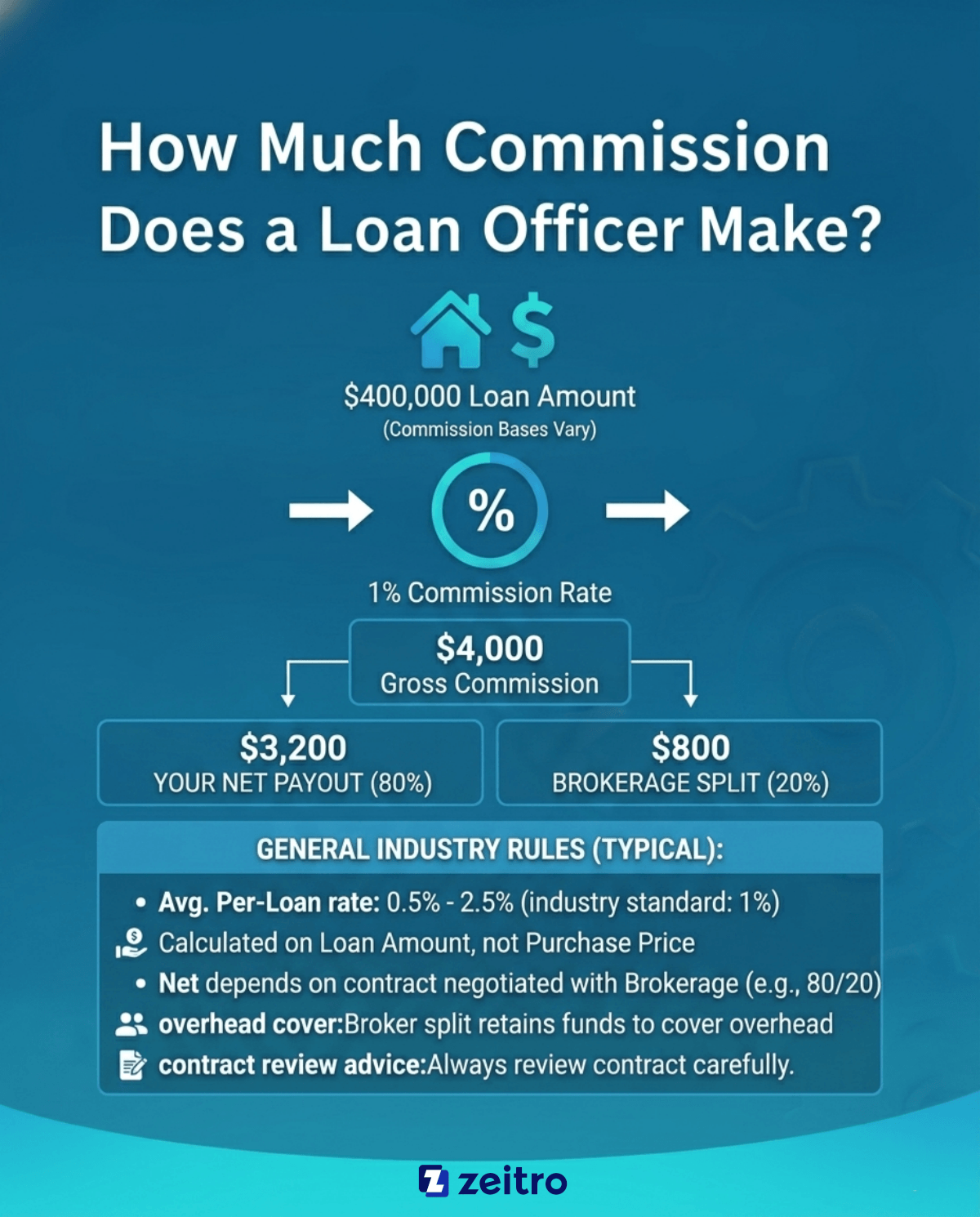

How Much Commission Does a Loan Officer Make?

On average, a loan officer earns between 0.5% and 2.5% in commission per closed loan, with 1% being the typical industry standard. In many cases, commission is calculated based on the loan amount rather than the purchase price, though pay structures vary by lender.

To see how the math works, imagine you close a $400,000 mortgage. At a 1% commission rate, the gross commission paid to your brokerage is $4,000. However, you don't pocket all of it. Your net payout depends on your negotiated commission split. If you have an 80/20 split with your broker, you will take home $3,200, while the brokerage retains $800 to cover overhead. In my early days, negotiating a fair split was just as important as generating the leads themselves, so always review your brokerage contract carefully.

Average Salary of Loan Officers

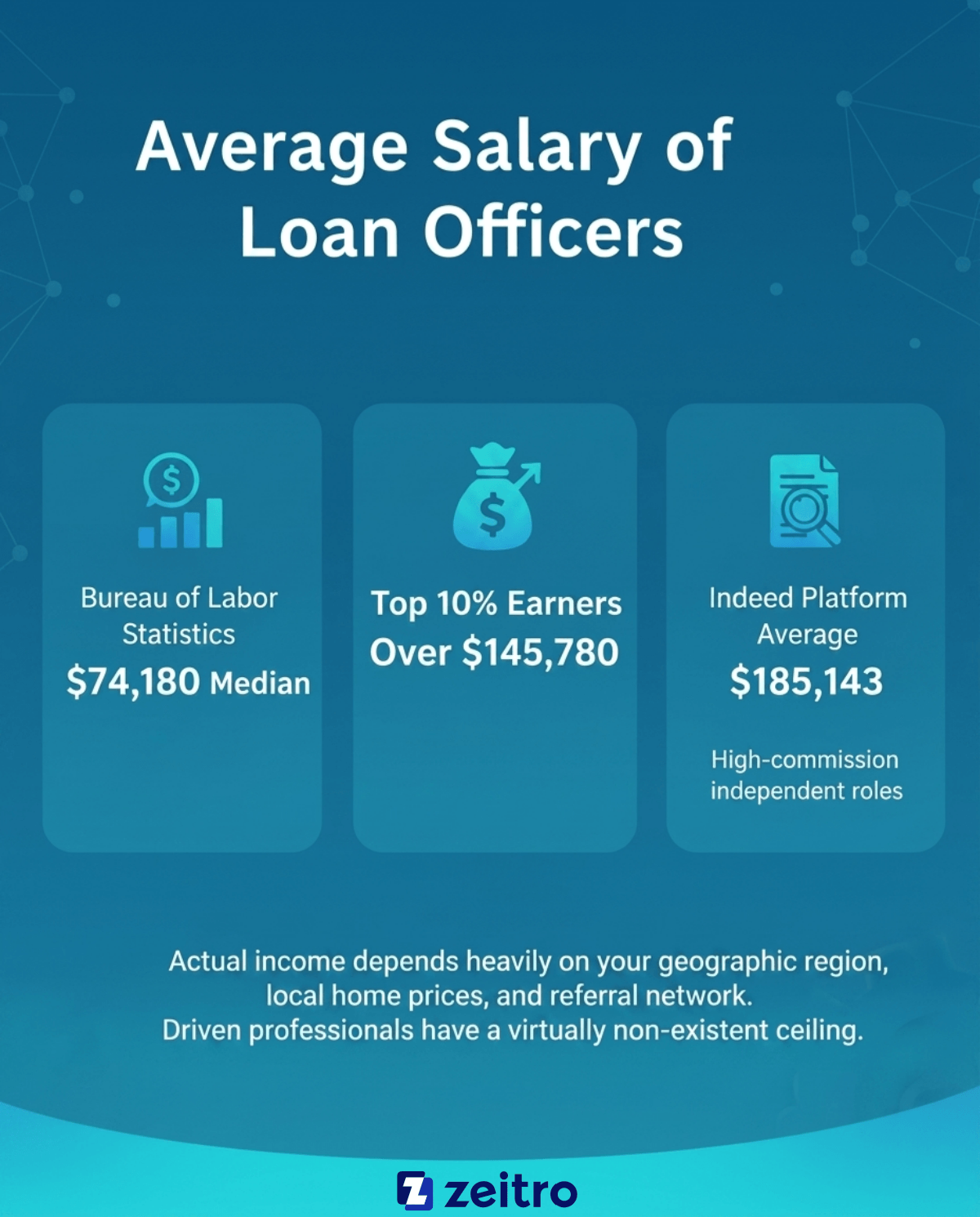

Because commissions fluctuate with the housing market, annual earnings vary widely. According to the U.S. Bureau of Labor Statistics, the median annual wage for loan officers is $74,180, with the top 10% of earners clearing more than $145,780. Meanwhile, job platforms like Indeed report average annual salaries exceeding $185,000, heavily driven by high-volume, commission-only originators.

From what I've seen in the field, your actual income depends heavily on your geographic region, local home prices, and your referral network.

- Bureau of Labor Statistics Median: $74,180

- Top 10% Earners: Over $145,780

- Indeed Platform Average: $185,143 (reflecting high-commission independent roles)

This wide spectrum proves that while the floor is low for those who struggle to find clients, the ceiling is virtually non-existent for driven professionals.

Also Read: Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

How Does a Loan Officer Get Paid?

In many commission-based roles, pay is triggered when the loan closes and funds, but some lenders use salary or hybrid compensation structures. Once the loan is funded, the closing agent distributes the gross commission to your brokerage, which then processes your split.

Many brokerages utilize a "draw against commission" system. This means they provide you with a regular advance payment to cover living expenses, which is later deducted from your earned commissions. Federal rules prohibit mortgage loan originator compensation from varying based on loan terms or conditions, including interest rate, fees, or other covered terms.

FAQs About Loan Officer Commission

Q1. How much commission do loan officers make on a $500,000 loan?

On a $500,000 loan, a standard 1% commission generates $5,000 gross. If your contract dictates an 80/20 split, you will personally earn $4,000. Under a bank's salary-plus-commission model, you might earn a much lower flat bonus, such as $500 to $1,000, but with a guaranteed base.

Q2. Will MLO be replaced by AI?

No, AI will not replace mortgage loan officers. While automated systems are excellent for processing paperwork, uploading documents, and verifying credit scores, borrowers still demand human guidance. Navigating a mortgage is highly emotional and legally complex. Real estate agents and buyers want a trusted human professional to solve sudden underwriting issues, offer empathy, and negotiate complex financial scenarios.

Also Read: AI Mortgage Underwriting Explained: Will You Be Replaced?

Q3. Do loan officers get commission in California?

Yes, but California enforces strict labor laws. All California loan officers must receive at least the state's minimum wage of $16.90 per hour for all hours worked, regardless of closed deals. If an MLO is classified as non-exempt, employers must also pay overtime. Thus, pure commission plans in California are highly regulated to protect employee wages.

Q4. How much does a loan officer make per loan?

Typically, a loan officer nets between $2,000 and $5,000 per closed loan. This estimate assumes a standard loan size of $300,000 to $500,000 and a typical commission split, though high-end luxury loans can yield significantly higher single-payday results.

Q5. Do loan officers pay for their own marketing and leads?

It depends on your business model. In my experience, commission-only independent brokers must fund their own marketing, CRMs, and lead generation, which eats into their profits but offers higher commission splits. Conversely, retail bank loan officers receive company-provided leads and marketing support, but accept a much lower commission percentage in return.

Conclusion

Navigating the world of loan officer commission can seem complex at first, but it ultimately offers one of the most rewarding financial paths in the real estate sector. Whether you choose the stability of a retail bank or the unlimited earning potential of an independent brokerage, your success will depend entirely on your work ethic and ability to build strong referral relationships.

If you are ready to take control of your financial future, your next step is to research your state's licensing requirements and prepare for the National Mortgage Licensing System exam. The effort is significant, but the payoff is entirely in your hands.

People Also Read

- Best AI Mortgage Underwriting Software for Loan Professionals

- Mortgage Underwriter vs Loan Officer: Which Career Is Best?

- 11 Best Loan Officer Schools for Newbies: Online & Local

- [Guide] What is a Loan Officer License? How to Get It?

- Best Mortgage Loan Officer Training: Which to Pick?