When I first considered transitioning into the mortgage industry, my biggest question was simple: how do loan officers actually get paid, and is the income as high as everyone says? If you are looking to change careers or become a licensed loan officer, understanding the commission structure is crucial. Let's dive straight into how much you can realistically earn and how those paychecks land.

Key Takeaways

Commission Structure: Most loan officers earn a percentage of closed loans, typically ranging from 0.5% to 2.5%.

Diverse Pay Models: Compensation ranges from pure commission to salary-plus-commission.

Regulatory Limits: Federal laws prevent pay variations based on loan interest rates.

Realistic Income: Average annual earnings span from $74,000 to over $180,000 based on loan volume.

Do Loan Officers Get Commission?

Yes, the vast majority of mortgage loan officers are compensated primarily through commissions. In my experience, this commission-driven model is what attracts top-tier talent, as it directly ties your hard work to your earning potential. Depending on the company you work for, you will typically encounter one of three main compensation structures:

Commission-Only: Common at independent brokerages. You receive no base salary, but you earn the highest possible percentage of the loan amount.

Salary Plus Commission: Salary, salary-plus-bonus, fixed-per-loan pay, and commission-based models may all be used at banks and credit unions.

Flat Fee: Some lenders use a fixed amount per loan, and whether that model applies to junior originators depends on the employer.

How Much Commission Does a Loan Officer Make?

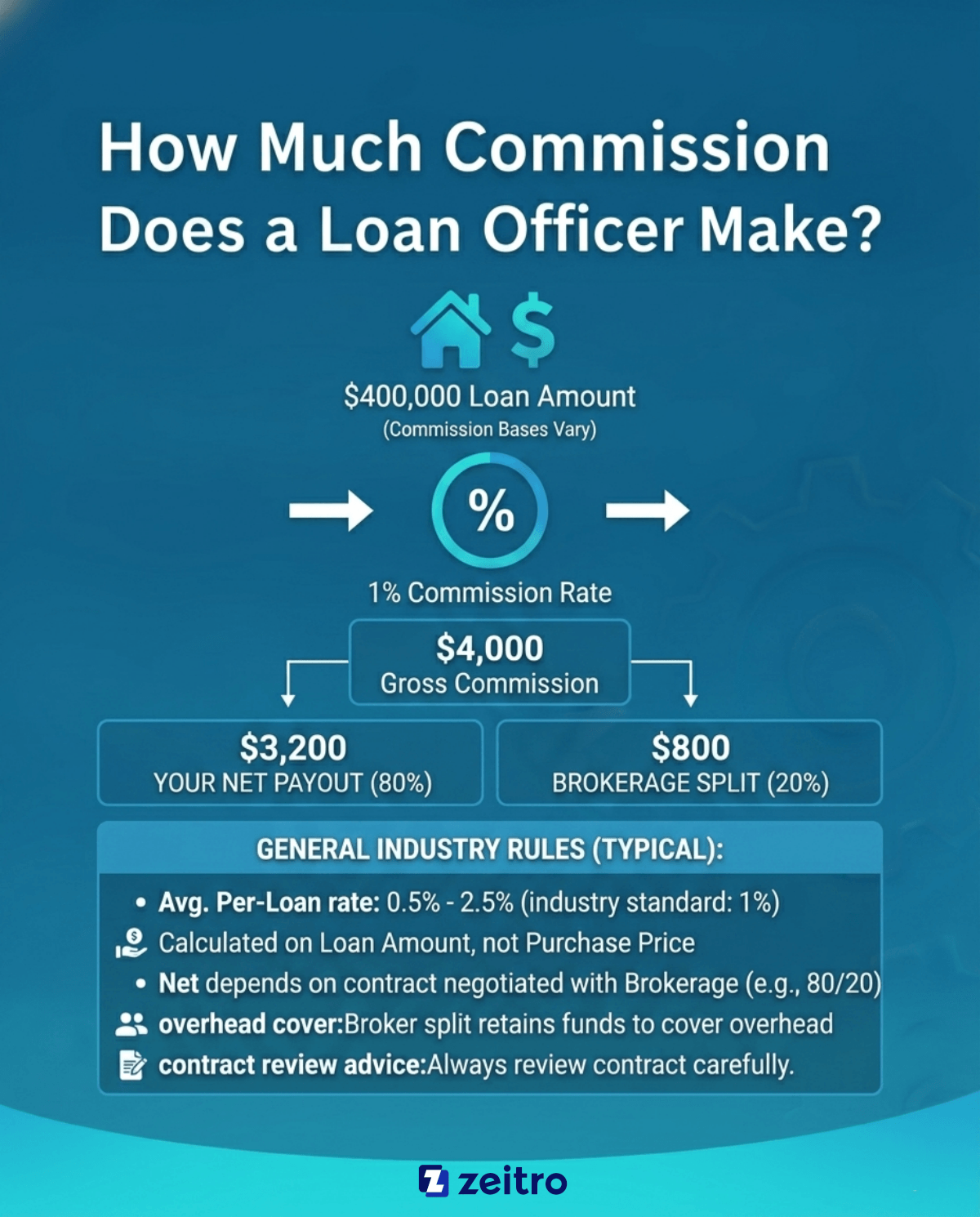

On average, a loan officer earns between 0.5% and 2.5% in commission per closed loan, with 1% being the typical industry standard. In many cases, commission is calculated based on the loan amount rather than the purchase price, though pay structures vary by lender.

To see how the math works, imagine you close a $400,000 mortgage. At a 1% commission rate, the gross commission paid to your brokerage is $4,000. However, you don't pocket all of it. Your net payout depends on your negotiated commission split. If you have an 80/20 split with your broker, you will take home $3,200, while the brokerage retains $800 to cover overhead. In my early days, negotiating a fair split was just as important as generating the leads themselves, so always review your brokerage contract carefully.

Average Salary of Loan Officers

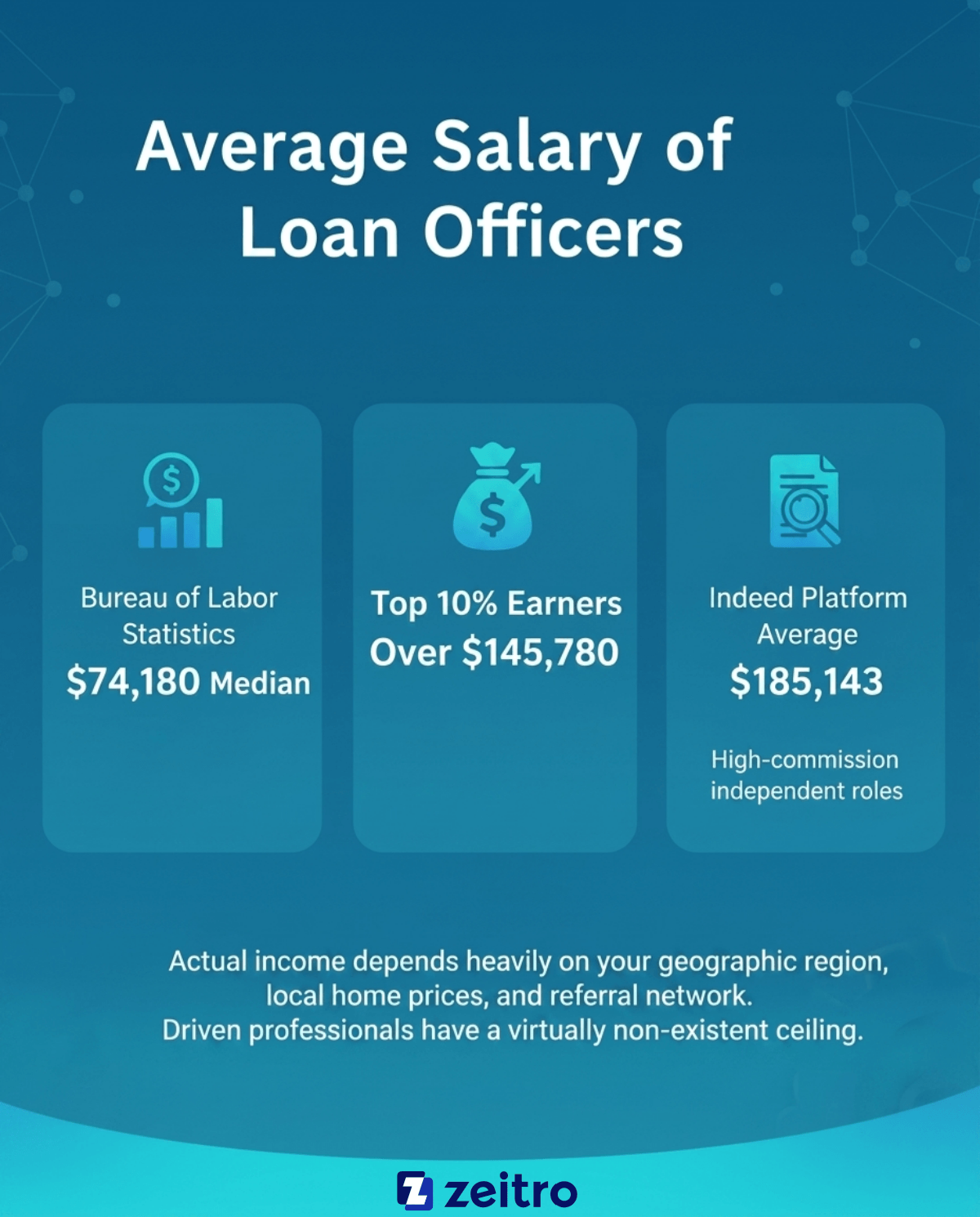

Because commissions fluctuate with the housing market, annual earnings vary widely. According to the U.S. Bureau of Labor Statistics, the median annual wage for loan officers is $74,180, with the top 10% of earners clearing more than $145,780. Meanwhile, job platforms like Indeed report average annual salaries exceeding $185,000, heavily driven by high-volume, commission-only originators.

From what I've seen in the field, your actual income depends heavily on your geographic region, local home prices, and your referral network.

This wide spectrum proves that while the floor is low for those who struggle to find clients, the ceiling is virtually non-existent for driven professionals.

In many commission-based roles, pay is triggered when the loan closes and funds, but some lenders use salary or hybrid compensation structures. Once the loan is funded, the closing agent distributes the gross commission to your brokerage, which then processes your split.

Many brokerages utilize a "draw against commission" system. This means they provide you with a regular advance payment to cover living expenses, which is later deducted from your earned commissions. Federal rules prohibit mortgage loan originator compensation from varying based on loan terms or conditions, including interest rate, fees, or other covered terms.

FAQs About Loan Officer Commission

Q1. How much commission do loan officers make on a $500,000 loan?

On a $500,000 loan, a standard 1% commission generates $5,000 gross. If your contract dictates an 80/20 split, you will personally earn $4,000. Under a bank's salary-plus-commission model, you might earn a much lower flat bonus, such as $500 to $1,000, but with a guaranteed base.

Q2. Will MLO be replaced by AI?

No, AI will not replace mortgage loan officers. While automated systems are excellent for processing paperwork, uploading documents, and verifying credit scores, borrowers still demand human guidance. Navigating a mortgage is highly emotional and legally complex. Real estate agents and buyers want a trusted human professional to solve sudden underwriting issues, offer empathy, and negotiate complex financial scenarios.

Q3. Do loan officers get commission in California?

Yes, but California enforces strict labor laws. All California loan officers must receive at least the state's minimum wage of $16.90 per hour for all hours worked, regardless of closed deals. If an MLO is classified as non-exempt, employers must also pay overtime. Thus, pure commission plans in California are highly regulated to protect employee wages.

Q4. How much does a loan officer make per loan?

Typically, a loan officer nets between $2,000 and $5,000 per closed loan. This estimate assumes a standard loan size of $300,000 to $500,000 and a typical commission split, though high-end luxury loans can yield significantly higher single-payday results.

Q5. Do loan officers pay for their own marketing and leads?

It depends on your business model. In my experience, commission-only independent brokers must fund their own marketing, CRMs, and lead generation, which eats into their profits but offers higher commission splits. Conversely, retail bank loan officers receive company-provided leads and marketing support, but accept a much lower commission percentage in return.

Conclusion

Navigating the world of loan officer commission can seem complex at first, but it ultimately offers one of the most rewarding financial paths in the real estate sector. Whether you choose the stability of a retail bank or the unlimited earning potential of an independent brokerage, your success will depend entirely on your work ethic and ability to build strong referral relationships.

If you are ready to take control of your financial future, your next step is to research your state's licensing requirements and prepare for the National Mortgage Licensing System exam. The effort is significant, but the payoff is entirely in your hands.

What is a bank statement, and why do lenders need it? Discover what's included, how to download e-statements, and how long to keep them for tax purposes

I still remember applying for my first apartment. The landlord casually asked for my "recent bank statements," and I honestly panicked a little. What exactly did he want to see? If you're trying to get a mortgage, secure a car loan, or even apply for a visa, you will run into this exact request.

Basically, a bank statement is just an official summary of the money moving in and out of your account. Let's break down exactly what's inside these documents, the easiest way to grab them, and why they matter so much.

Key Takeaways

It's a monthly snapshot from your bank detailing every deposit, withdrawal, and fee.

You can usually download digital versions (e-statements) for free through your bank's website or mobile app.

Lenders rely on them heavily to verify your income and track spending habits.

For tax-related records, keep them for at least three years, and longer in cases where the IRS retention period may extend to six or seven years.

What is a Bank Statement?

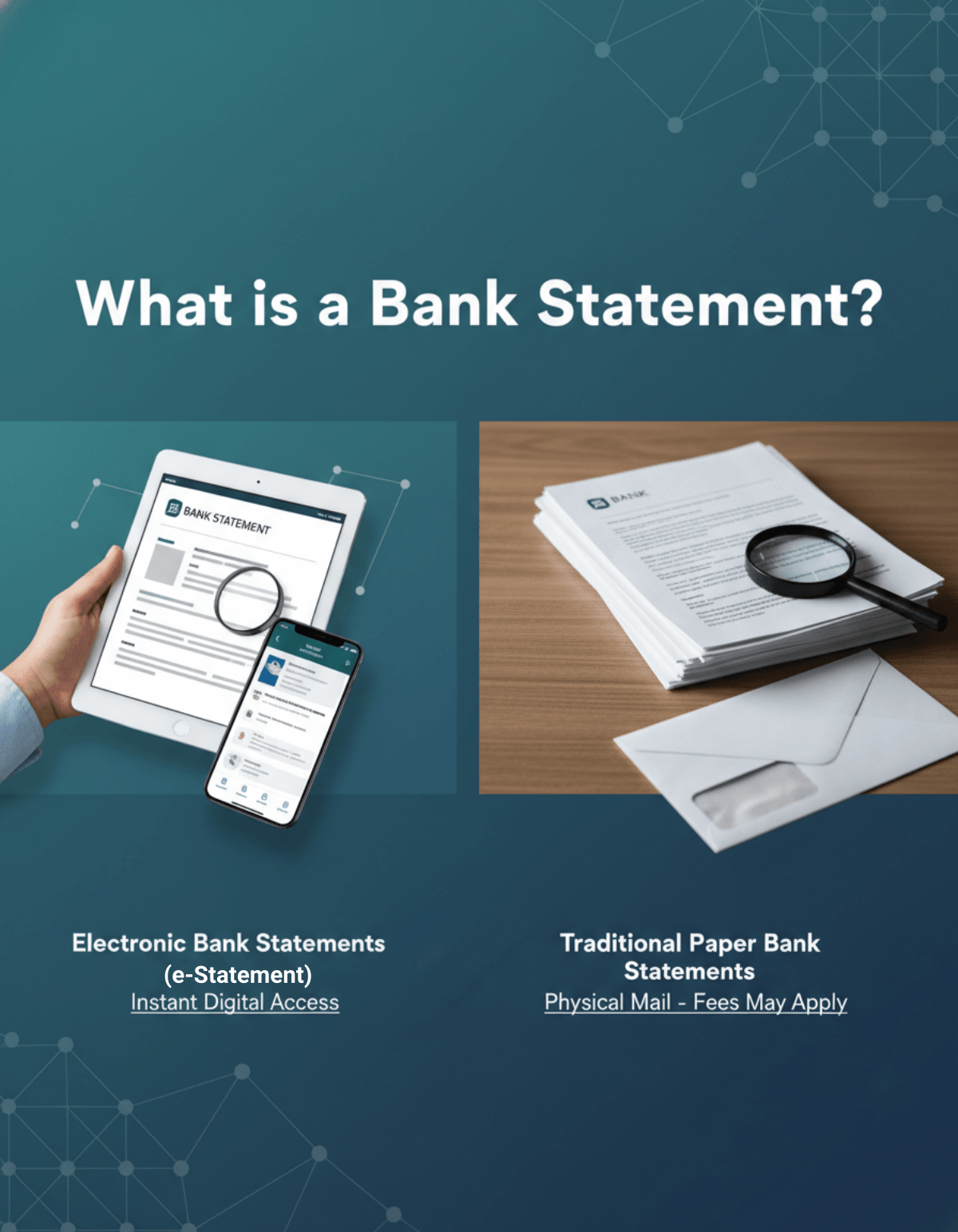

Think of it as a detailed financial report card. A bank statement is a formal document your bank or credit union issues, usually every single month, that tracks every penny moving through your account. Because it is issued by a financial institution, it serves as an official financial record.

Nowadays, you mainly deal with two versions. First up are Electronic Bank Statements (e-Statements). I honestly prefer these. They are digital PDFs you can download instantly, and they usually contain the same information as paper statements. Then you have traditional Paper Bank Statements. Sure, getting physical mail is nice, but be careful. Some banks charge a monthly fee for paper statements, but the amount varies by institution.

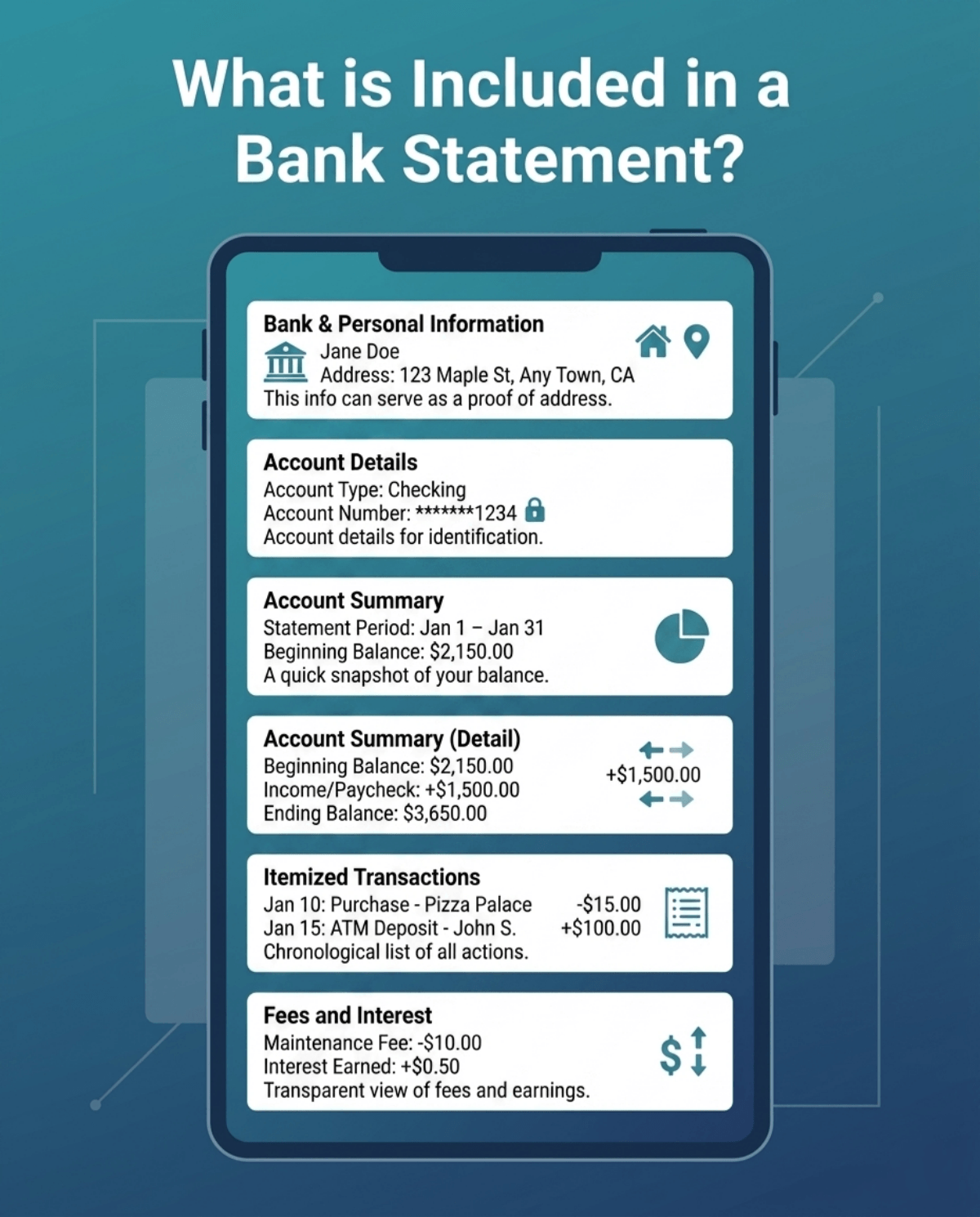

What is Included in a Bank Statement?

Opening a PDF packed with tiny numbers might trigger a headache, but the layout is surprisingly predictable once you know what to look for. Here is the standard breakdown:

Bank & Personal Information: Up top, you'll spot the bank's logo alongside your full name and registered home address. Because this info is verified, these documents can sometimes be used as proof of address if they show your name, current address, and a recent issue date.

Account Details: This section shows your account type (like checking or savings) and your account number, though they usually hide the first few digits for security.

Account Summary: A quick snapshot highlighting the specific dates covered (the statement period), exactly what you started with (beginning balance), and what you had left at the end.

Itemized Transactions: This is the main event. It's a chronological list of every single action—paychecks hitting your account, that late-night pizza slice, ATM trips, and Zelle transfers.

Fees and Interest: A transparent look at any maintenance fees, painful overdraft charges, or the APY interest your money earned that month.

What is a Bank Statement Used For?

You might wonder why anyone besides you cares about these logs. In the real world, these documents unlock a lot of doors. I've personally had to hand them over for a few major life events:

Mortgage & Loan Applications: When you apply for a mortgage, lenders review bank statements to verify the source of funds and check for irregular deposits, alongside other documents used to calculate your debt-to-income ratio.

Proof of Address: Government agencies and utility providers love seeing these because they instantly verify where you actually sleep at night.

Renting an Apartment: Landlords use them to double-check that you make enough money to cover the monthly rent without struggling.

Tax Preparation: Come April, your CPA will want these to verify self-employment income or prove those business expenses you're writing off.

The Importance of a Bank Statement

Even if you aren't trying to secure a loan right now, ignoring these monthly summaries is a bad idea. Making a habit of reviewing them is arguably the best thing you can do for your personal finances.

Security & Fraud Detection: Skimming your transactions is the fastest way to catch a stolen credit card number or weird subscription charges before they drain your account.

Budgeting & Cash Flow: It forces you to face reality. Seeing exactly how much you spent on takeout makes adjusting your budget much easier.

Accuracy: Banks aren't flawless. I've personally caught accidental double-charges and sneaky hidden fees just by paying attention.

Documentation: Having a solid paper trail saves you if you ever face a tax audit or need to prove a specific bill was paid on time.

Bank Statement Example

If you've never really examined one, picture a clean, highly structured letter. The top right corner proudly displays the bank's logo, while your name and address sit across from it on the left. Just below that personal info, a bolded summary box highlights the crucial math: your starting cash, total money in, total money out, and what's left.

The bottom portion takes up the most space. It's basically a massive, chronological receipt showing the exact date and amount for every coffee, paycheck, and bill payment.

How to Get a Bank Statement?

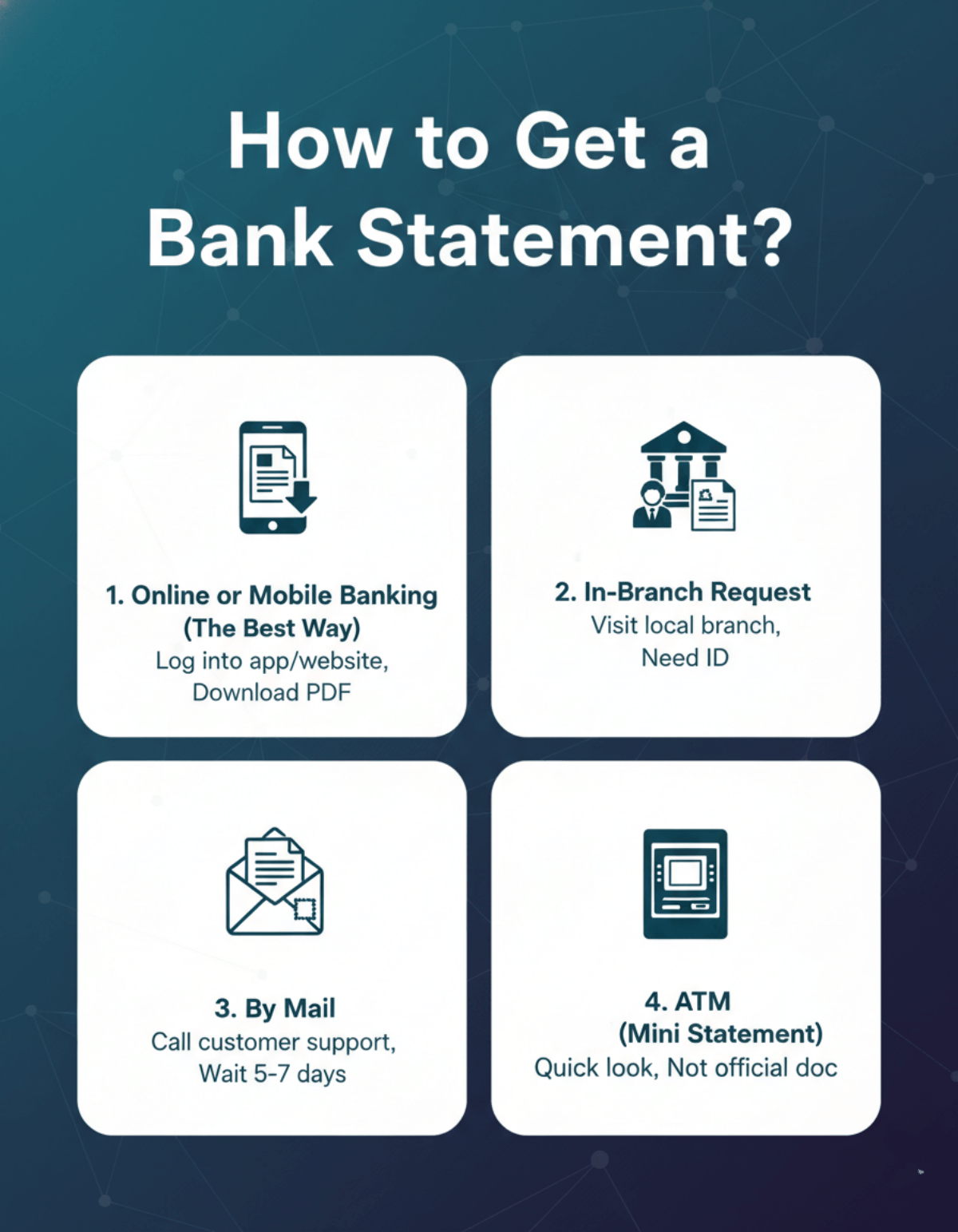

So, your lender needs your records by tomorrow. Don't panic. You have a few different ways to grab them, ranging from instant to waiting on the mailman:

Online or Mobile Banking (The Best Way): I rarely do things in person anymore. Just log into your banking app or website, find the "Statements & Documents" section, and pick the months you need. Always hit the download button to save an official PDF. Trust me, loan officers will immediately reject a rough screenshot from your phone.

In-Branch Request: If you happen to be near your local branch or need someone to physically stamp the paper, walk right in. Hand the teller your driver's license, and they'll print it for you. Just watch out. Some branches charge a couple of bucks per page.

By Mail: You can always call customer support and request a paper copy of a specific month. You could also tweak your account settings to get paper mail regularly again. Keep in mind, the postal service takes about 5 to 7 business days.

ATM (Mini Statement): Need something quick? ATMs can print a tiny receipt showing your last few transactions. Just remember, nobody accepts this as an official document.

How to Read a Bank Statement?

You definitely don't need an accounting degree to figure this out. I always start by glancing at the top: does the final balance actually match the cash I thought I had? From there, quickly scan your withdrawals. You are hunting for unusually large numbers, subscriptions you swore you canceled, or payee names you don't recognize.

This quick check-up is called "reconciling." You're just comparing your own mental notes or budget app against the bank's official log. If the math feels off, call them right away.

How Long Should You Keep Bank Statements?

I used to stuff every piece of financial mail into a shoebox until I finally learned the actual rules. For everyday checking accounts, keeping statements for at least one year is a common rule of thumb, though longer retention may be needed for tax or legal purposes.

However, taxes change the game. The IRS suggests holding onto them for three to seven years if they back up a business expense, home purchase, or major tax deduction. Instead of drowning in paper, I highly recommend downloading the PDFs and tossing them into a secure, encrypted cloud folder.

FAQs About a Bank Statement

Q1. What are bank statement mortgage guidelines?

When you apply for a house, lenders usually ask for two solid months of records. They often want to see every page, including any blank pages, to make sure nothing is missing and to check for stable paychecks and flag any mysterious large deposits.

Q2. Can a bank statement be used as proof of address?

Absolutely. Some DMV offices, government agencies, and landlords may accept bank statements as proof of address, provided they meet the organization's date and format requirements. Just make sure your name and address match your application perfectly and the date is recent (usually within 90 days).

Q3. Are screenshots of a bank statement acceptable?

Screenshots are usually not accepted because they are harder to verify than an official PDF from the bank.Mortgage brokers and government agencies will reject cell phone screenshots because they are too easy to fake in Photoshop. Always provide the unedited, official PDF directly from your bank's website.

Q4. Does everyone have bank statements?

Bank statements are issued for many types of financial accounts, including checking, savings, money market, and other eligible accounts. If you operate entirely in cash or use prepaid debit cards, you are considered "unbanked" and won't get these official summaries.

Q5. How often are bank statements issued?

Most of the time, they hit your inbox once a month. However, if you have a slow-moving savings or investment account that calculates interest differently, you might only see one every quarter (three months).

Q6. How to reconcile a bank statement?

It's just matching things up. Pull up your personal budget tracker or receipts and compare them against the bank's log line by line. You want to make sure no money vanished and no extra fees sneaked in.

Conclusion

Honestly, getting comfortable with these documents is a huge step toward taking control of your financial life. Whether you are prepping to buy your first home, trying to rent a better apartment, or just wanting to spot where your cash is leaking, these summaries tell the real story.

Do yourself a favor and switch to e-statements if you haven't already. It stops mail theft, saves trees, and keeps annoying fees out of your life. Take five minutes this week to download your latest copy and see exactly where you stand.

What is a WVOE (Fannie Mae Form 1005)? Discover why mortgage lenders require a Written Verification of Employment and how it impacts your home loan approval.

When I bought my first home, the mountain of paperwork felt endless. Just when I thought my standard paystubs and W-2s were enough to prove I could afford a mortgage, my loan officer asked for a WVOE. If you are going through the mortgage approval process right now, you might be wondering what this is.

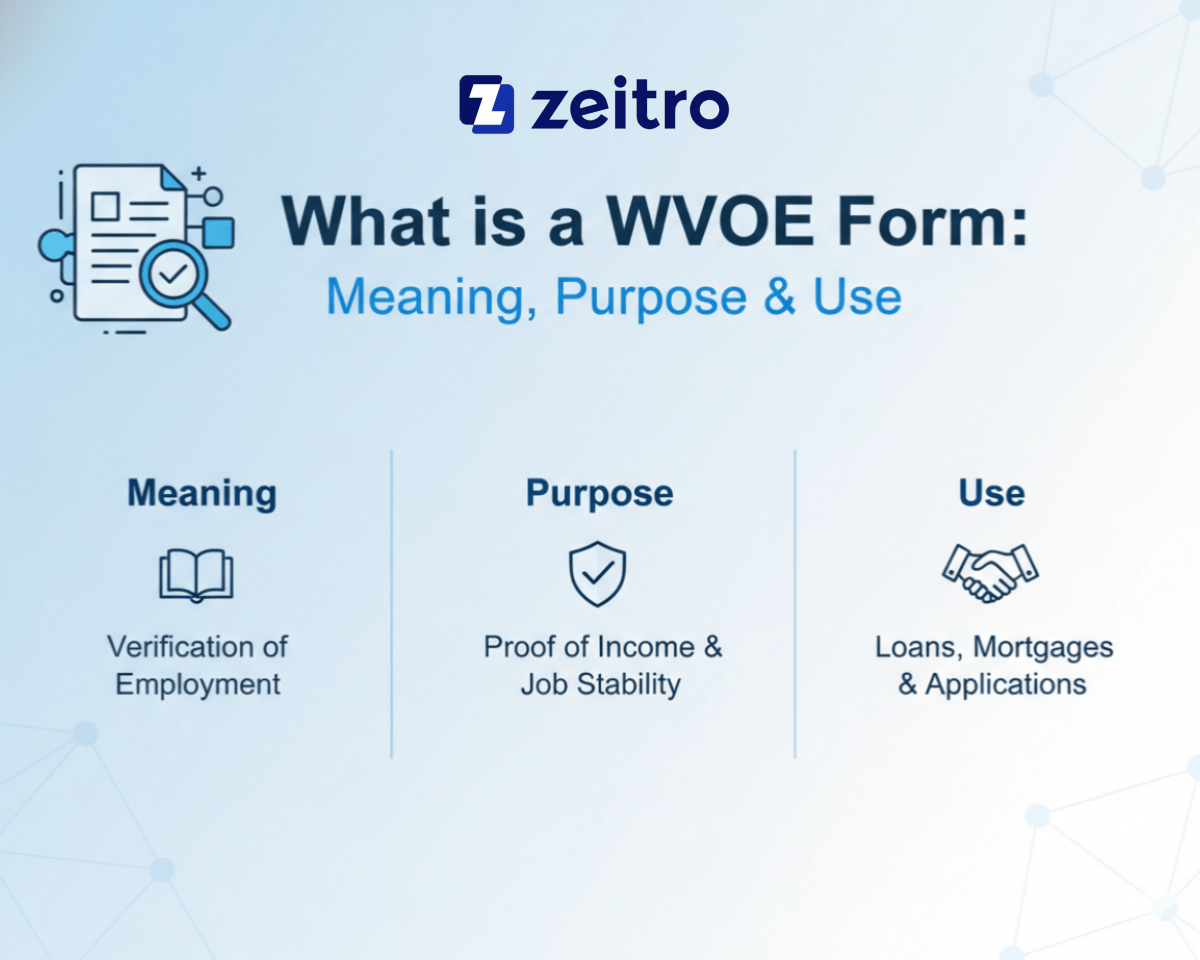

A WVOE, or Written Verification of Employment, is commonly documented using Fannie Mae Form 1005, the Request for Verification of Employment. It is a crucial document lenders use to confirm your job history and income directly with your employer. Understanding how it works can make your loan approval much smoother.

Key Takeaways

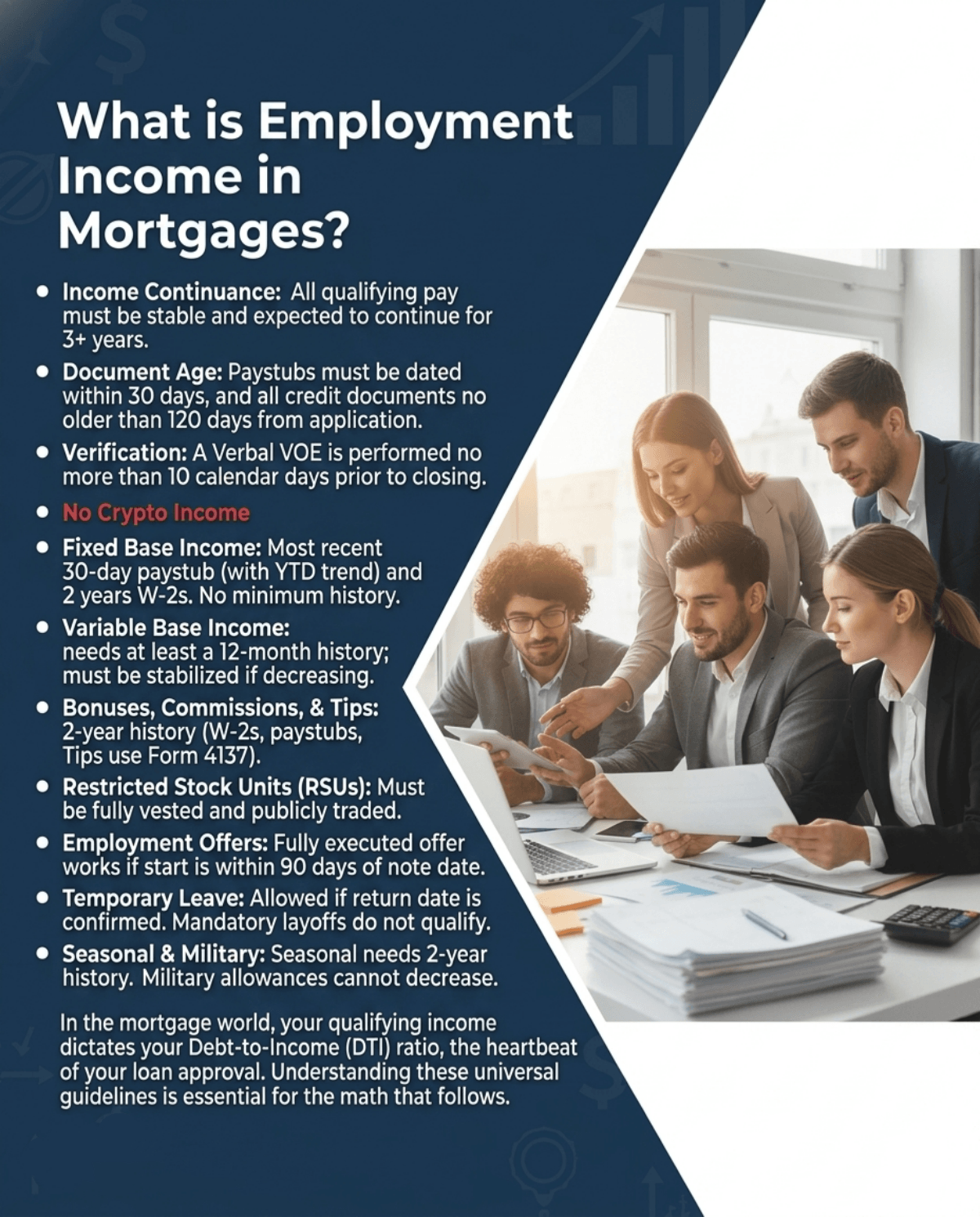

The Core Definition: A WVOE is an official document completed by your employer to verify your income and job status.

Direct Routing for Security: For first mortgages, the lender must send the form directly to the employer and receive it back directly; for some second mortgages, the borrower may hand-carry it to the employer.

Detailed Breakdown: It may verify base pay, year-to-date earnings, overtime, commissions, bonuses, and the probability of continued employment.

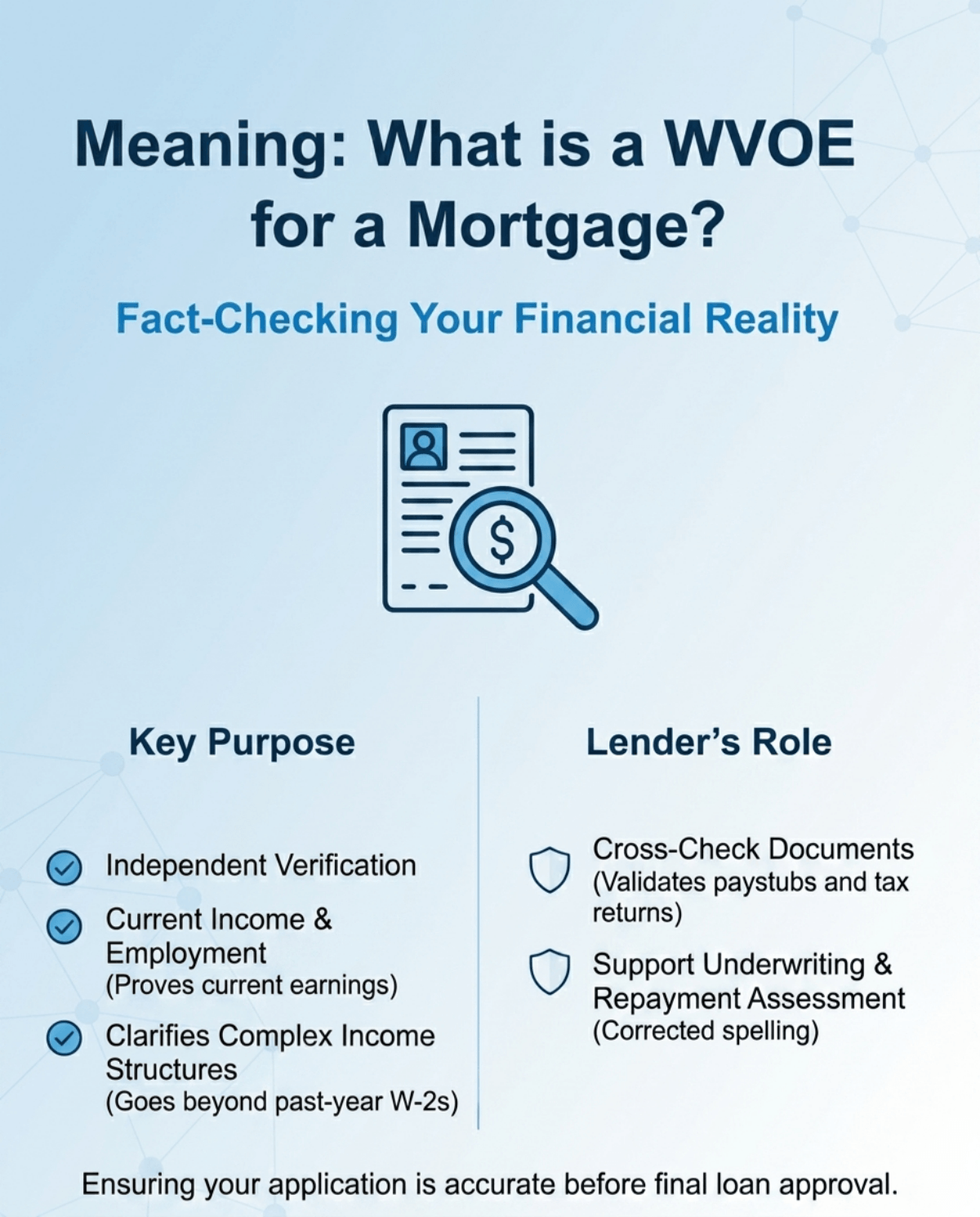

Meaning: What is a WVOE for a Mortgage?

So, what exactly does this form mean for your application? From an underwriting perspective, a WVOE serves as an independent, third-party cross-check of your financial reality.

You might be thinking, "I already handed over months of paystubs and tax returns. Why do they need this?" Lenders use the WVOE to help verify employment and income, which supports underwriting and repayment assessment.

While your W-2 shows what you made last year, the written verification proves what you are earning right now and clarifies complex income structures. It is essentially your lender's way of fact-checking your application before handing over hundreds of thousands of dollars.

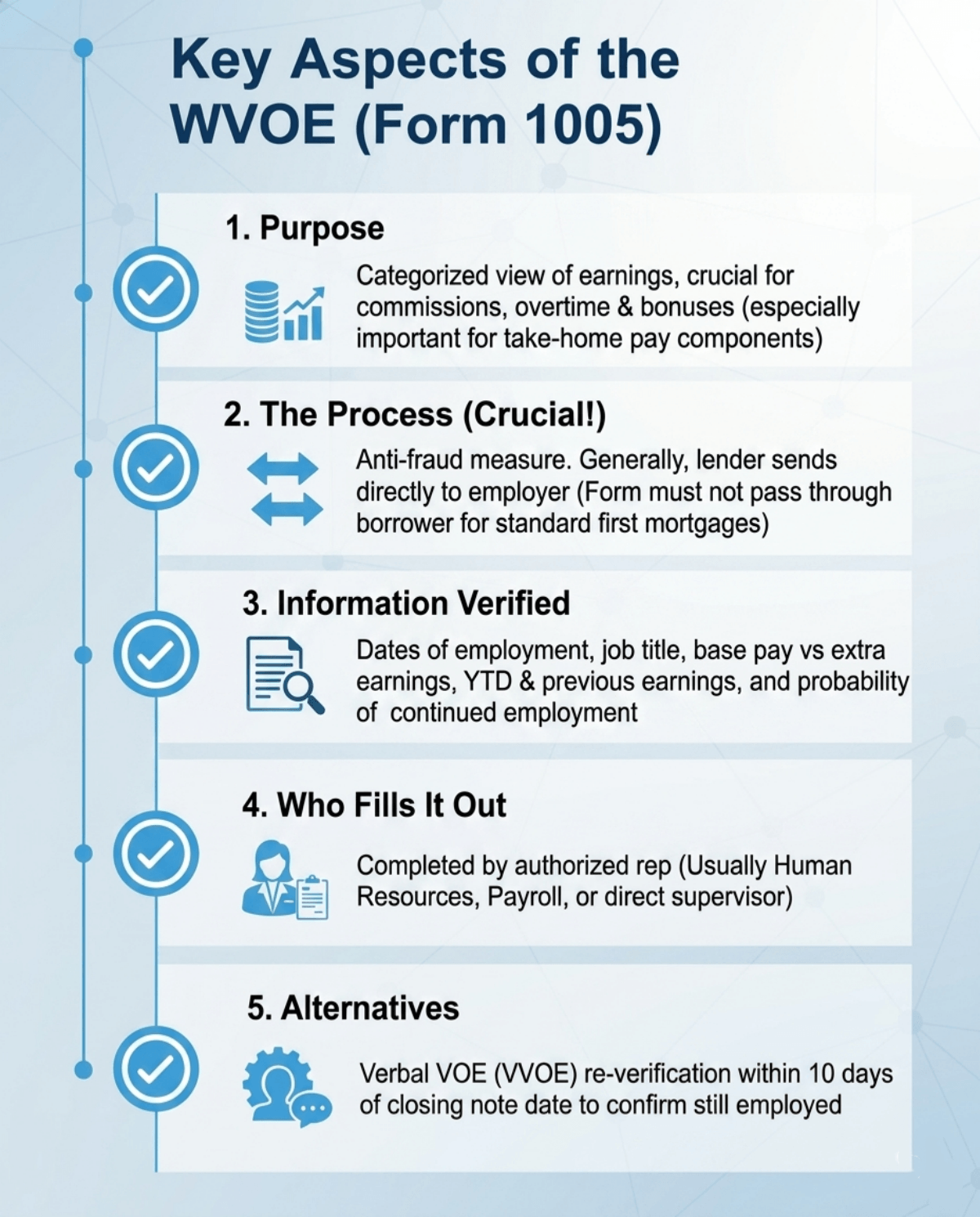

If you have never seen Fannie Mae Form 1005, it helps to know exactly what goes into it. Here is a breakdown of the core elements your lender is looking for:

Purpose: It gives underwriters a clear, categorized view of your earnings. This is especially important if a chunk of your take-home pay comes from commissions, heavy overtime, or annual bonuses.

The Process (Crucial!): This is a strict anti-fraud measure. For conventional first mortgages, the form should not pass through the borrower. However, second mortgages may allow the borrower to hand-carry the form to the employer.

Information Verified: It digs deep. The document confirms your exact dates of employment, current job title, a breakdown of base pay vs. extra earnings, year-to-date (YTD) income, previous years' earnings, and your probability of continued employment.

Who Fills It Out: It must be completed by an authorized company representative—usually someone in Human Resources, the payroll department, or your direct supervisor.

Alternatives: While written verifications offer historical depth, lenders also use a Verbal VOE (VVOE). A verbal re-verification is often completed within 10 daysbefore the note date to confirm the borrower is still employed.

When is a WVOE Used?

Not every single mortgage application requires a physical Form 1005, but you will definitely encounter it in several specific scenarios:

Variable Income Earners: If your paycheck fluctuates because you rely heavily on overtime, shift differentials, tips, or performance bonuses, lenders need the WVOE to calculate your qualifying average income.

Incomplete Documentation: Sometimes, your standard W-2s or recent paystubs might be smudged, missing pages, or simply don't provide a comprehensive financial picture.

Recent Job Changes: If you just switched companies or received a major promotion, lenders need this form to verify your new compensation structure and start date.

Specific Loan Types: Some government-backed loans may require employment verification, but lenders can use written VOE, verbal re-verification, or approved third-party electronic verification, depending on program rules.

Who Needs to Fill out a VOE Form?

I often see homebuyers get confused about their responsibilities here. Let me clear this up: you and your employer have two very distinct roles, and blurring them can pause your loan.

The Borrower (You): Your only job is to sign Part I of the form. Your signature acts as a legal authorization, giving your employer permission to release your private financial data to the lender.

The Employer (HR/Payroll): They handle Part II. An authorized representative must calculate your income data, fill out the specific financial fields, and sign the bottom to certify its accuracy.

Under no circumstances should you ever try to fill in your own income numbers.

How Can I Get an Employment Verification Form?

You won't have to hunt down this PDF yourself. Here is exactly how the WVOE workflow happens:

Authorization: Your lender will provide Form 1005. You just sign Part I to authorize the release of information.

Lender Dispatch: The mortgage company securely emails, faxes, or mails the request directly to your employer's HR department.

Employer Return: Once completed, your company sends the certified document straight back to the underwriter.

Today, many large companies use automated third-party verification systems like Equifax's The Work Number. If so, the physical paper process is completely replaced by instantaneous electronic data retrieval!

FAQs About WVOE Mortgage

Q1. What is a WVOE request?

A WVOE request is an official inquiry sent directly from a mortgage lender to a borrower's employer. Its purpose is to securely verify the applicant's job history, position, and detailed income breakdown to ensure they qualify for the home loan.

Q2. Is a WVOE different from a verbal VOE (VVOE)?

Yes. A WVOE is a detailed, written financial breakdown gathered early in underwriting. In contrast, a VVOE is usually just a quick, 5-minute phone call lenders make to your employer right before closing to ensure you are still actively employed.

Q3. Can a borrower fill out their own WVOE?

Absolutely not. You are only allowed to sign the authorization section. Filling in your own income figures or handling the completed document violates strict anti-fraud rules and can be considered mortgage fraud, instantly killing your loan approval.

Q4. How long does a WVOE stay valid?

Timing requirements vary by loan program, but FHA guidance requires employment re-verification within 10 days before the note date, and certain third-party electronic data must be current within 30 days. If your closing gets significantly delayed, the underwriter will likely need to request a fresh verification.

Q5. What happens if my employer refuses to fill out the WVOE?

If your HR department is unresponsive, don't panic. Lenders can usually pivot to alternative documentation. They might ask you for additional tax transcripts, extensive bank statements, or pull electronic data through third-party services like The Work Number to satisfy the requirement.

Final Word

Buying a house comes with a lot of paperwork, but the Written Verification of Employment is just a standard safety measure. It protects everyone involved by confirming you can comfortably handle the new monthly payments.

If I can leave you with one practical tip, it's this: give your HR department a quick heads-up early on. Tell them a mortgage company will be reaching out for a verification request. When they know to watch out for that specific email or fax, they'll handle it much faster, keeping your home closing perfectly on schedule!

Unsure if you should itemize your taxes this year? Discover the 2026 mortgage interest deduction rules, limits, and FAQs to see if it's worth it for you.

Paying off a house is tough enough without leaving money on the table come tax season. If you're a homeowner looking to maximize your 2026 tax refund, you've probably wondered how the mortgage interest deduction actually works this year.

With the recent 2025 tax extension legislation keeping many of the old rules in place, a lot of the provisions we thought were expiring just became our new normal. I've broken down exactly what the IRS expects from you for the 2026 tax year, so you can stop stressing and start saving.

Key Takeaways

Before we get into the weeds, here is exactly what you need to know:

You can write off interest on up to $750,000 of your loan or $1 million if you bought before Dec 16, 2017.

You must ditch the standard deduction and choose to itemize to get this benefit.

For 2026, the mortgage interest cap remains in effect, and the standard deduction has been adjusted upward for inflation.

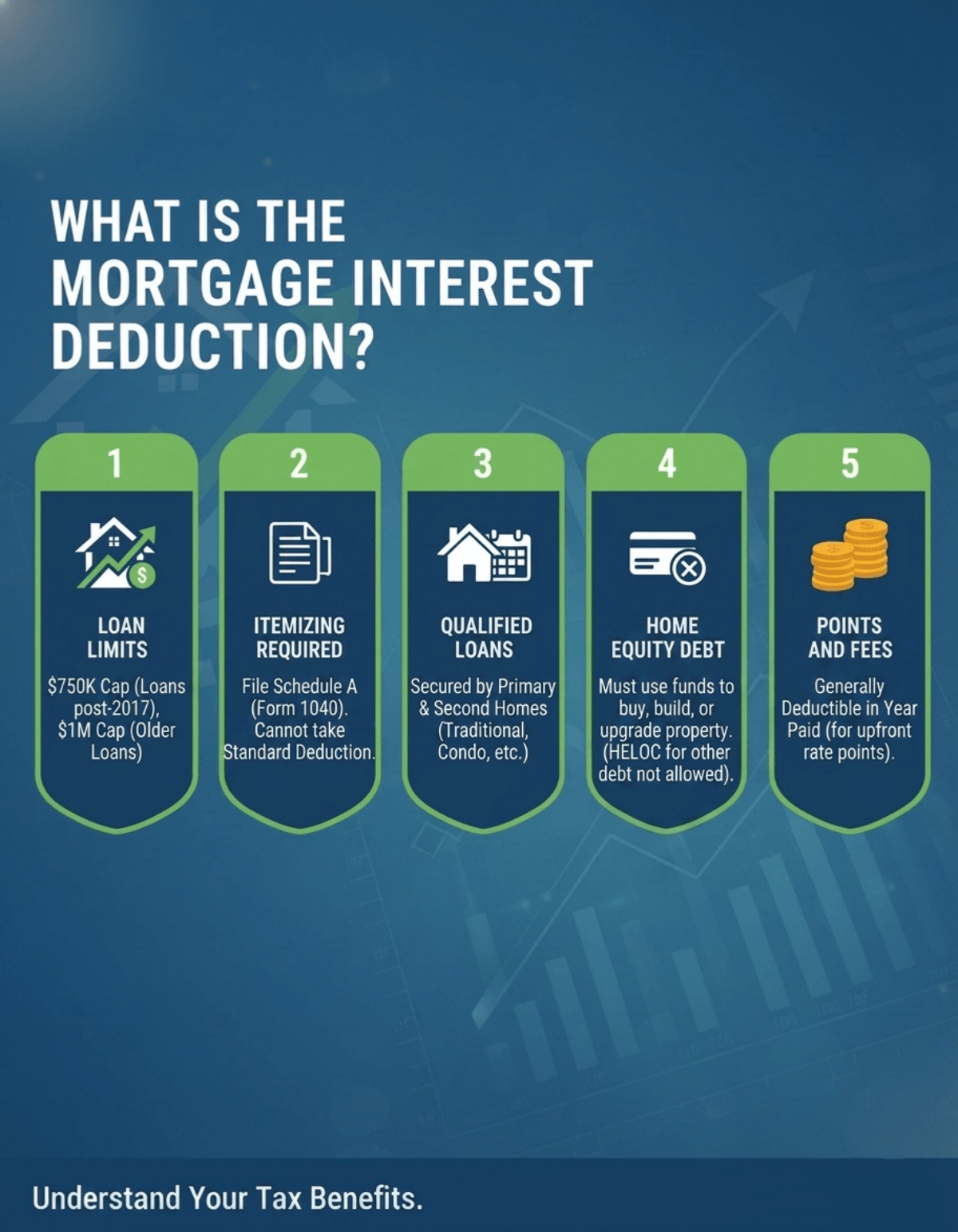

What is the Mortgage Interest Deduction?

This deduction is the government's way of rewarding you for buying a house. It lets you subtract the interest you pay on your home loan directly from your taxable income. But the IRS doesn't just hand this out freely—there are strict boundaries.

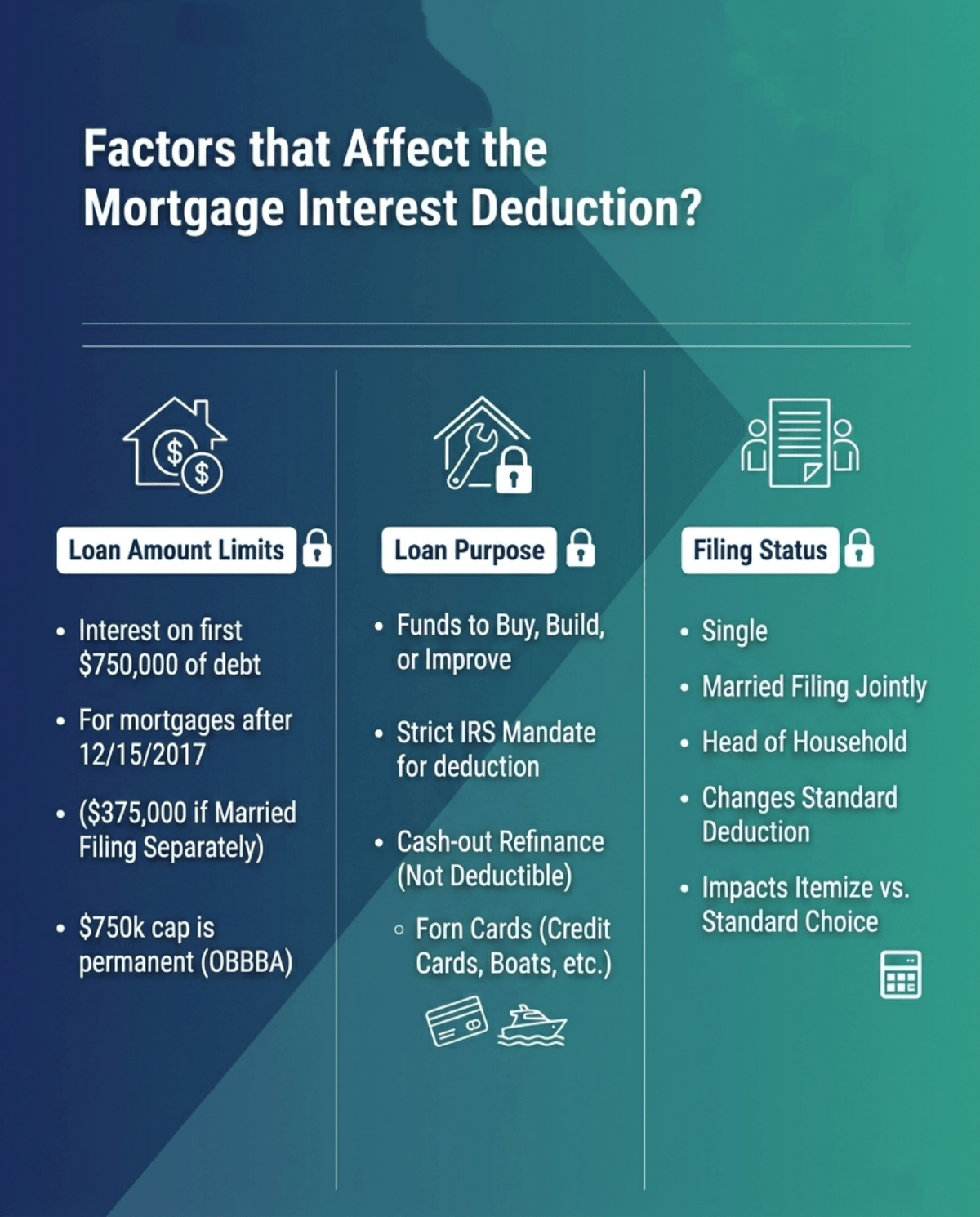

Loan Limits: If you took out your mortgage after December 15, 2017, the deduction is capped at the first $750,000 of your debt. Older loans still enjoy the legacy $1 million limit.

Itemizing Required: You have to file Schedule A (Form 1040). You can't take the standard deduction and claim your mortgage interest. It's one or the other.

Qualified Loans: The house has to actually secure the loan. This works for your primary residence and a second home, whether it's a traditional house, condo, or even a mobile home.

Home Equity Debt: Taking out a HELOC to pay off credit cards? That interest isn't deductible. The funds must be used to physically buy, build, or substantially upgrade the property.

Points and Fees: If you bought down your interest rate by paying "points" upfront, you can usually deduct those in the year you paid them.

How Does Mortgage Interest Deduction Work?

The whole thing is basically a math competition between two numbers: the standard deduction and your itemized expenses. Every year, the IRS gives everyone a flat baseline deduction. For 2026, a married couple filing jointly gets a standard deduction of $32,200. You only win if your specific, individual expenses add up to more than that baseline.

Let's say you and your spouse paid $18,000 in mortgage interest last year. You also paid $8,000 in state property taxes and gave $6,000 to your local food bank. Add those up, and you hit $32,000 in itemized deductions. Since $32,000 beats the standard deduction, you'd itemize. That extra difference is where your real tax savings kick in.

How Much Can You Deduct?

The amount you can wipe off your taxes relies entirely on when you borrowed the money and how much you still owe. If your mortgage debt qualifies and stays within the applicable limit, you may generally deduct all of the home mortgage interest you paid for the year. If your loan is bigger than that, you'll have to calculate a percentage.

Also, if you bought a place with a friend or partner (and you aren't legally married), the IRS only lets you claim the exact portion of interest you personally paid. Don't guess these numbers. In late January 2027, your lender will generally send you Form 1098 by January 31. That little piece of paper has the exact dollar amount you need to put on your tax return.

What Qualifies as Mortgage Interest?

I often see folks assume any money sent to their lender counts as a write-off. Unfortunately, the IRS is pretty picky. Here is what actually qualifies:

Primary loan interest: The actual interest charge on your main mortgage statement.

Home equity loan interest: Only if you used the cash to put on a new roof, remodel a kitchen, or make another major property improvement.

Late payment penalties: Late payment charges may be deductible as home mortgage interest if they are not for a specific service performed in connection with the mortgage loan.

Prepayment penalties: Prepayment penalties may be deductible as home mortgage interest if the fee is not for a specific service performed or cost incurred in connection with the loan.

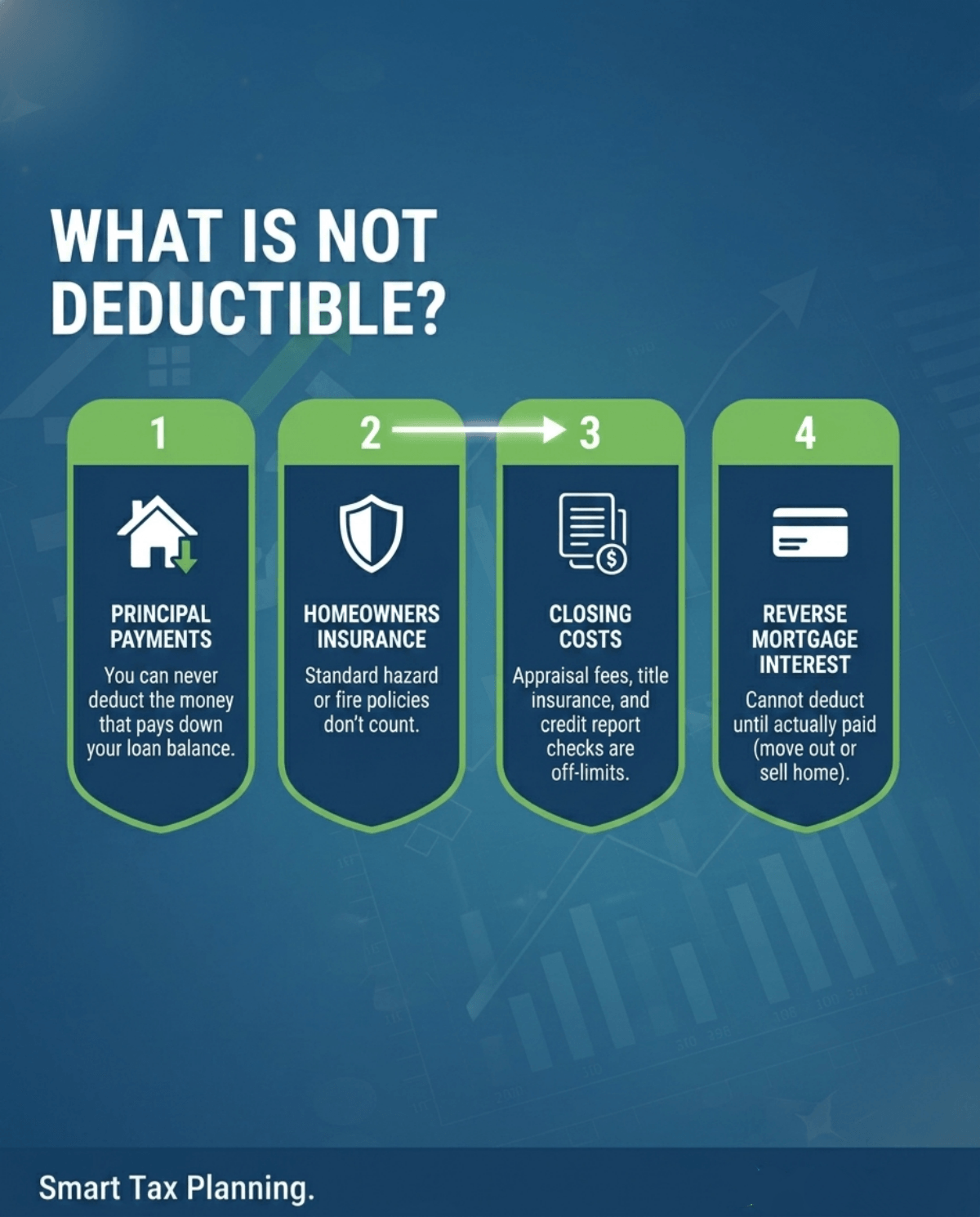

What Is NOT Deductible?

This is where people make the most expensive mistakes on their returns. The IRS will absolutely reject your deduction if you try to claim the wrong housing expenses. Here is what you cannot deduct:

Principal payments: This is the big one. You can never deduct the money that actually pays down your loan balance. Only the interest.

Homeowners insurance: Your standard hazard or fire policies don't count.

Closing costs: Appraisal fees, title insurance, and credit report checks are strictly off-limits.

Reverse mortgage interest: You can't deduct this until you actually pay it, which normally doesn't happen until you move out or sell the home.

How to Claim the Mortgage Interest Deduction for the 2026 Tax Year

Ready to actually do the paperwork? The process isn't as scary as it sounds. Here is the step-by-step workflow I use when gathering my own tax documents:

Track down your Form 1098: Keep an eye on your mail or your lender's online portal around late January. Look at Box 1—that's your official interest paid for 2026.

Tally your other write-offs: Don't file yet. Dig up your receipts for significant medical bills, your state and local taxes (SALT, which is currently capped), and any charitable donations you made during the year.

Run the numbers: Combine everything from Step 2 with your mortgage interest. Is that final number higher than the 2026 standard deduction for your filing status?

Fill out Schedule A: If your itemized total won the math battle, ignore the standard deduction. Report your mortgage interest on Schedule A (Form 1040) and attach it to Form 1040.

Should You Claim the Mortgage Interest Deduction?

It really depends on your lifestyle and where you live. Here is my general rule of thumb:

When to say Yes: You bought a pricey house recently (meaning your early payments are mostly interest), you donate a lot to charity, or you live in a state with very high income taxes. Itemizing will probably save you a ton.

When to say No: You're single with a small loan balance, or you've owned your house for 15 years and are mostly paying down the principal. The standard deduction is easier and will give you a bigger refund.

FAQs About Mortgage Interest Deduction

Q1. What loans qualify for a mortgage interest deduction?

You can write off interest from a primary mortgage, a second mortgage, or a HELOC. The main catch is that the loan must be legally secured by your primary or secondary home. Also, any home equity funds must be used for actual structural improvements, not personal expenses.

Q2. What are the pros and cons of the mortgage interest deduction?

The biggest pro is the potential to slash your taxable income by thousands of dollars, especially in the early years of homeownership. The downside? You have to keep meticulous receipts to itemize, and the financial benefit naturally shrinks over time as you pay off the principal.

Q3. Is home mortgage interest 100% deductible?

No, it's not unlimited. The IRS strictly caps how much debt qualifies. You can only deduct the interest tied to the first $750,000 of your mortgage balance. If you borrowed $900,000, you can only claim a prorated percentage of your total interest paid.

Q4. What are the new rules for mortgage interest deduction?

For 2026, the big news is that the $750,000 cap was recently extended instead of expiring. With the standard deduction remaining historically high, fewer people will naturally itemize, but high-cost area homeowners will still heavily rely on this deduction to lower their tax burden.

Q5. What is the mortgage interest deduction limit for a Single Person?

A single person has the exact same $750,000 loan limit as a married couple filing jointly. However, if you are legally married but decide to file separate returns, the IRS cuts your individual limit completely in half, dropping it down to $375,000.

Final Word: Is a Mortgage Interest Deduction Worth It?

Absolutely. If your total deductible expenses surpass the IRS standard deduction, claiming your mortgage interest is one of the smartest financial moves you can make. It's a completely legal way to shield thousands of your hard-earned dollars from the government. Just remember that it requires a bit of math and organization.

A quick heads-up: I'm sharing my personal understanding of these rules, but tax codes are notoriously tricky and change based on your location. Before you file your 2026 returns, please run your numbers by a licensed CPA or a qualified tax professional to make sure you're protected.

Do lenders use gross or net income for a mortgage? Discover why banks rely on gross pay for approval, how DTI is calculated, and how to budget safely.

I've seen countless homebuyers get confused during pre-approval. You look at your paycheck, see what actually hits your bank account, and think: "Why is the bank calculating a loan amount that seems way higher than what I can afford?"

The answer comes down to one simple rule. For many borrowers, lenders use gross income to calculate qualification, but income may be adjusted differently depending on the loan program and income type.

However, to avoid real-life financial stress, you must rely on your Net Income (your actual take-home pay) to build your budget. Let me show you exactly why banks do this and how it impacts your homebuying power today.

Employment type matters: W-2 workers and self-employed applicants face vastly different income evaluations.

Your budget relies on Net Income: While banks approve you based on gross pay, your take-home pay determines your true affordability. Don't borrow the maximum just because you can!

Do You Use Gross or Net Income for a Mortgage?

For standard home loans like Conventional, FHA, and VA mortgages, lenders use your Gross Monthly Income. That is the amount you earn before taxes, insurance premiums, and retirement contributions are deducted.

Why? Because it gives banks a fair, standardized baseline to compare your finances against other borrowers. Everyone has different tax brackets and optional deductions, like a 401(k) or health savings account (HSA). Using gross pay removes those variables, allowing underwriters to purely evaluate your overall earning power.

Core Differences: Gross vs. Net Income in Mortgage Applications

These two numbers play completely different roles in your homebuying journey. One is for the underwriter's spreadsheet, and the other is for your personal peace of mind. Here is how they compare.

Definition

Your Gross Income is the big number at the very top of your pay stub. It represents all the money you earned during a pay period before a single dime is taken out for federal or state taxes, Social Security, Medicare, union dues, or health insurance.

On the flip side, Net Income is what we often call your "take-home pay." It is the exact amount that eventually gets deposited into your checking account after all mandatory and voluntary deductions are stripped away. Understanding this distinction is step one, because mixing them up is the easiest way to derail an application right out of the gate.

Purpose in Loan Approval

Banks rely heavily on gross income because it acts as the denominator when calculating your Debt-to-Income (DTI) ratio. Whether they are looking at your front-end DTI (just your housing costs) or your back-end DTI (your housing costs plus credit cards, student loans, and auto loans), the math always starts with your pre-tax earnings.

This is the primary metric lenders use to assess your absolute highest repayment capacity. They essentially want to know your raw earning power before your personal lifestyle choices or tax strategies shrink that number down. If you make $8,000 gross a month, that is the exact figure the automated underwriting system uses to greenlight your file.

Non-Discretionary vs. Discretionary Deductions

Have you ever wondered why lenders don't just look at what hits your bank account? It is because many paycheck deductions are entirely voluntary, or "discretionary." For example, if you aggressively contribute 15% of your paycheck to a 401(k) or overpay your taxes to get a big refund, your net income looks artificially low.

A lender knows that, if push comes to shove and you need to make your mortgage payment, you could simply pause those retirement contributions. Because you have the power to control these optional deductions, banks feel comfortable basing your loan approval on your gross earning potential.

Budgeting Reality for Borrowers

Here is where I always warn my clients: just because the bank uses your gross income doesn't mean you should. This disconnect is exactly how buyers end up "House Rich, Cash Poor."

For example, if a lender approves you for a $4,000 monthly payment based on a $10,000 gross income, that is only an illustration, because actual approval also depends on taxes, insurance, debts, and loan program rules. They aren't considering the fact that your real take-home pay is only $6,500.

After you pay that mortgage, you might barely have enough left for groceries, gas, and emergencies. To protect your financial health, always run your personal living budget using your net income, regardless of the maximum loan amount you get approved for.

How Do Lenders Evaluate Income?

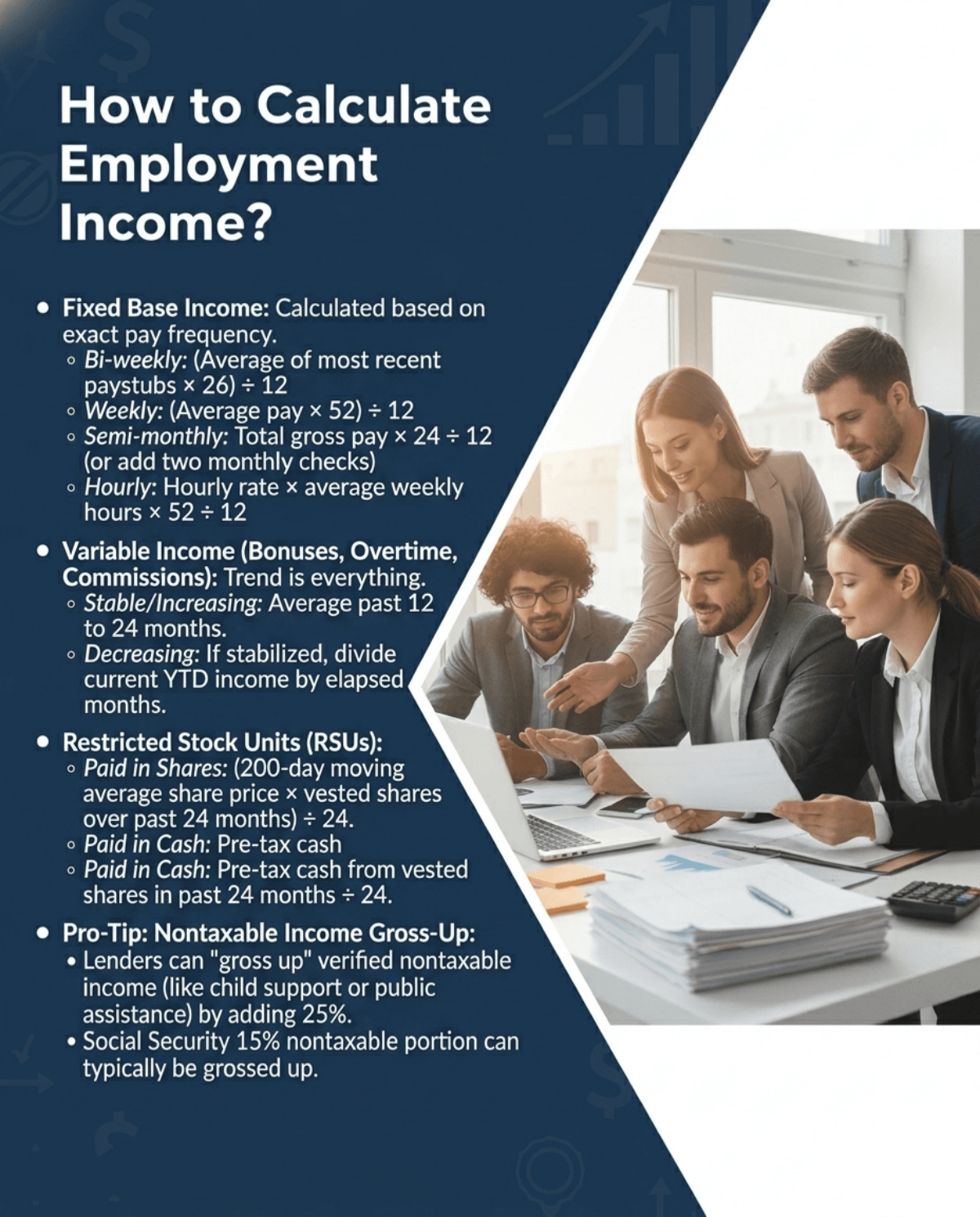

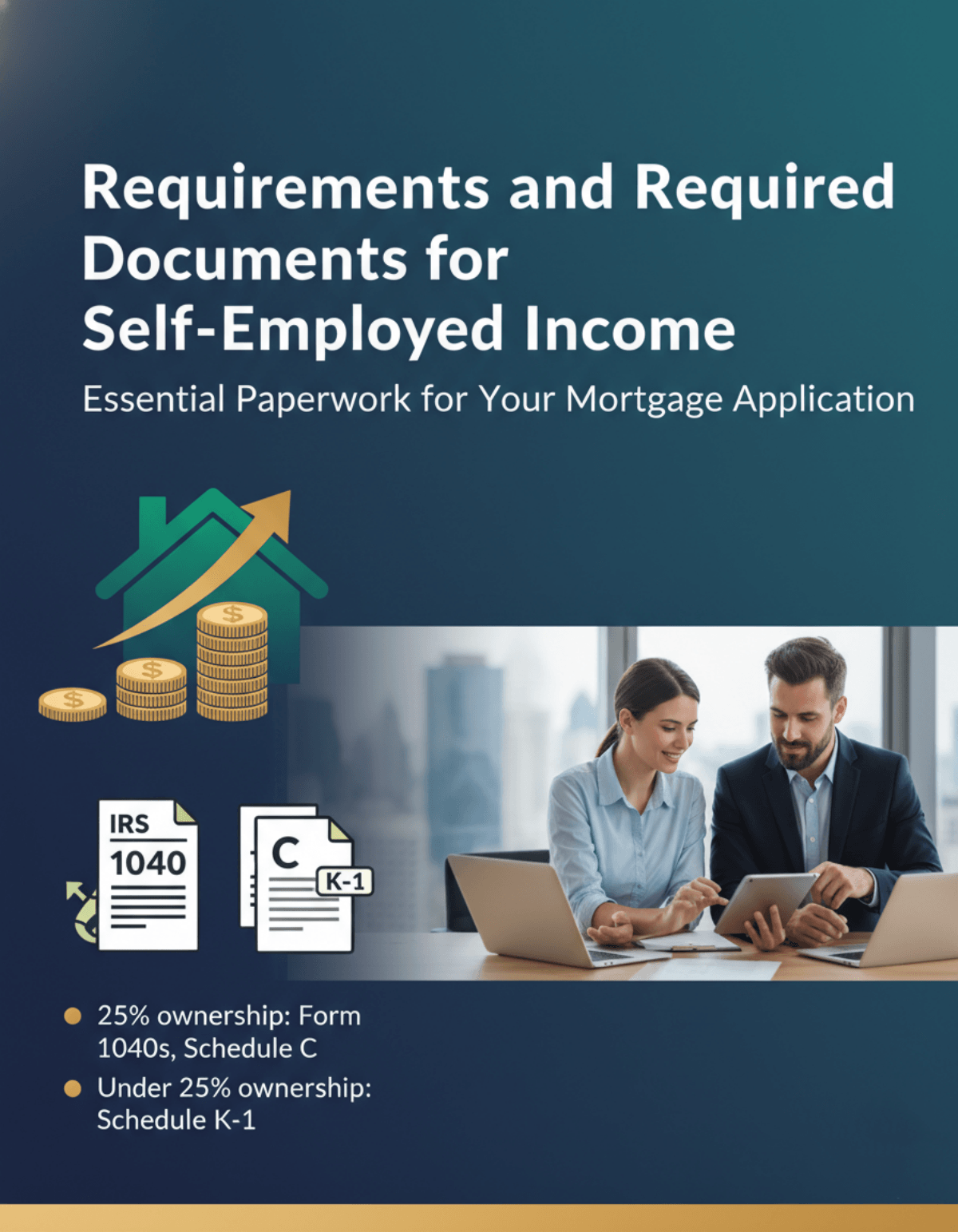

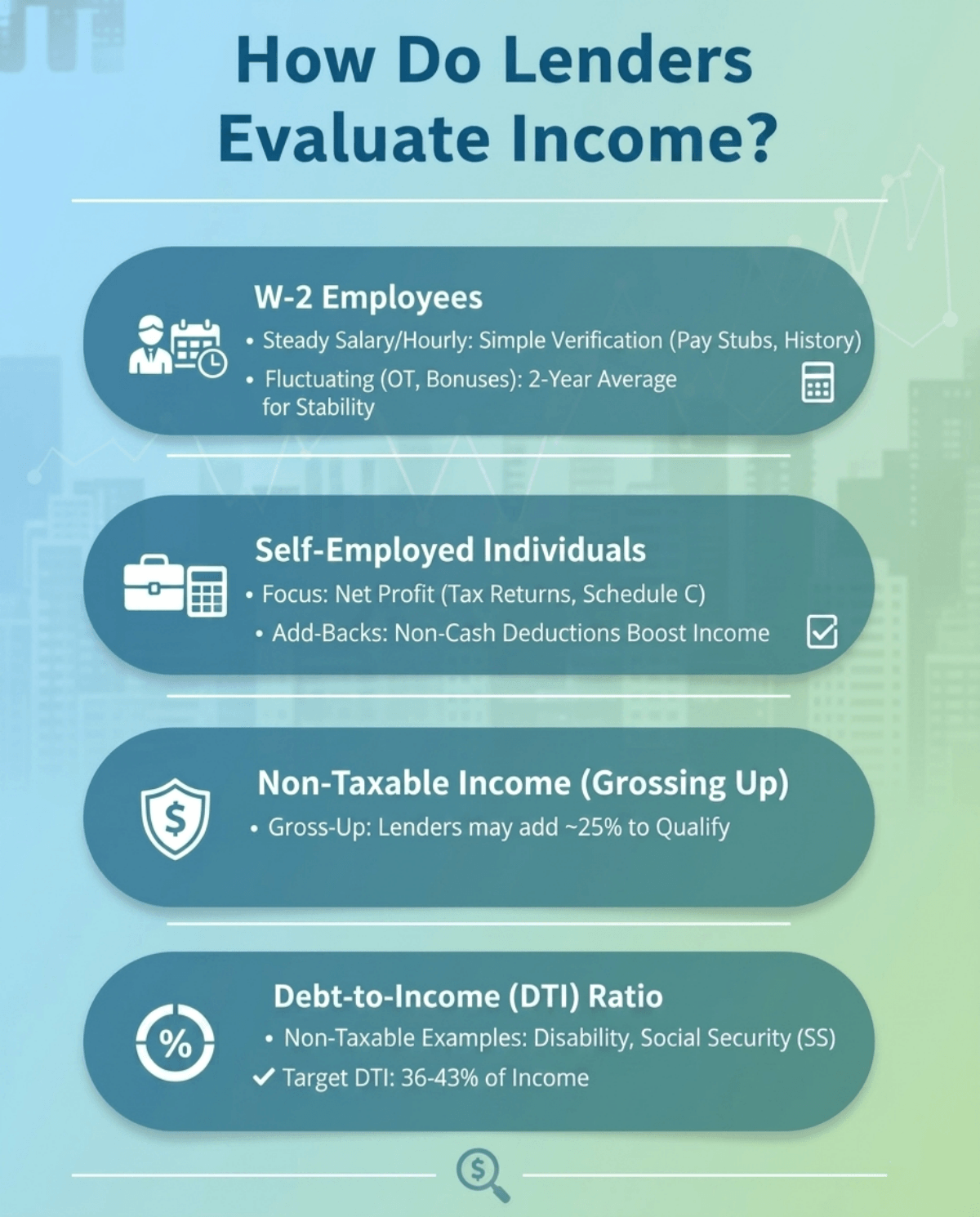

When an underwriter reviews your file, they don't just glance at a W-2 and call it a day. The way they calculate your qualifying income depends heavily on how you earn your money.

W-2 Employees: If you earn a steady salary or hourly wage, the process is usually straightforward, but lenders still verify employment history, recent pay stubs, and other supporting documents. But if your income fluctuates with overtime, bonuses, or commissions, lenders will generally require a two-year track record. They will average out those extra earnings over 24 months to ensure stability.

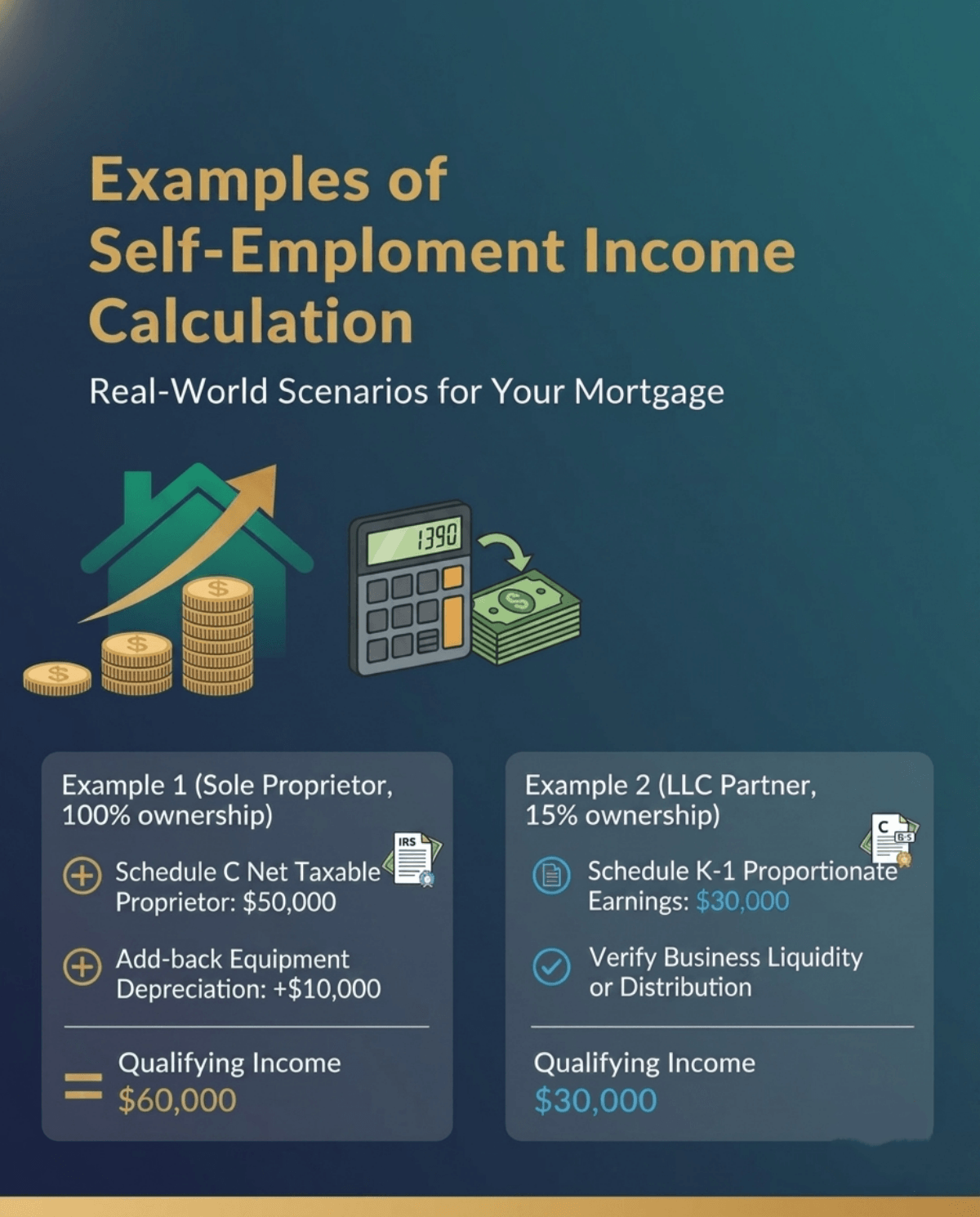

Self-Employed Individuals: This is where things flip. If you own a business, lenders actually look at your tax returns (like Schedule C) and focus on your Net Profit—your business revenue minus expenses. However, there is a silver lining. Underwriters will do "add-backs," returning non-cash deductions like depreciation to your bottom line, which artificially boosts your qualifying income.

Non-Taxable Income (Grossing Up): If you receive tax-free money, like disability benefits or Social Security, underwriters apply a neat trick called "grossing up." For certain non-taxable income types, lenders may apply a gross-up adjustment, often 25%, depending on program rules and the income source.

Debt-to-Income (DTI) Ratio: Once they finalize your gross figure, they use it to ensure your total monthly debts don't exceed that sweet spot of 36% to 43% of your income.

What are the Mortgage Income Requirements?

Income isn't just about the raw number. Stability and the type of mortgage you apply for matter just as much. Looking at the latest 2026 lending guidelines, here is what you need to know before you apply:

The 2-Year Rule: WFor variable or self-employed income, underwriters often want a 24-month history of stable earnings, while salaried W-2 income may be evaluated based on current verified employment and pay history. Job hopping within the same industry is usually fine, but sudden career changes can raise red flags.

Loan Types Matter: Your loan program dictates how strictly your income is judged. Conventional loans can allow higher DTIs in some cases, with common limits around 36% for manually underwritten loans, up to 45% for certain eligible cases, and up to 50% for DU findings. VA loans place special emphasis on residual income, while FHA loans mainly rely on DTI and other underwriting factors.

Alternative Proof of Income: If you are self-employed and your tax returns don't reflect your true cash flow, 2026 brings great news. Some Non-QM loans can use bank statements or alternative documentation instead of traditional tax-return-based income verification, depending on the product. Instead, lenders verify your income using 12 to 24 months of personal or business bank statements.

Q1. Why do lenders use gross income instead of net income?

Net income varies wildly from person to person based on tax brackets, health insurance premiums, and retirement contributions. Gross income gives lenders a universal, standardized baseline to fairly compare the financial strength and borrowing capacity of every applicant.

Q2. Is the 28% rule gross or net?

The classic 28% rule is always based on your Gross Income. This financial rule of thumb suggests that your total monthly housing expenses, including principal, interest, property taxes, and home insurance, should not exceed 28% of your pre-tax monthly earnings.

Q3. Is a mortgage 33% of gross income?

Traditionally, lenders prefer your front-end DTI (housing costs alone) to sit between 28% and 33% of your gross pay. However, some loan programs, like FHA loans, may allow your housing payment to consume up to 40% of your gross income if you have great credit.

Q4. What percentage of your income should go towards your mortgage?

While a lender might approve a mortgage taking up 28% to 30% of your gross income, personal finance experts advise a safer route. For true financial wellness, try to keep your mortgage payment under 25% to 30% of your net (take-home) pay.

Q5. Do mortgage lenders use gross or net income for self-employed?

For traditional conventional or FHA loans, lenders look at your business's Net Profit on your tax returns, plus allowable "add-backs" like depreciation. However, if you use a Non-QM bank statement loan, the lender may qualify you based on your gross business deposits.

Conclusion

Navigating the mortgage approval process can feel overwhelming, but understanding how banks view your money is half the battle. Remember the golden rule: lenders use your gross income to maximize your borrowing power, but you must use your net income to ensure you can actually afford the monthly payments. Before you start touring homes, I highly recommend getting your paperwork in order.

Gather your last two years of W-2s or tax returns, and plug your numbers into an online mortgage income calculator to estimate your DTI. Taking this step early makes qualifying for a mortgage much smoother. It helps you figure out the maximum loan you can get, and more importantly, what you can comfortably pay without losing sleep.

A loan officer's guide to calculating net income for a mortgage. Understand DTI, gross vs net pay, and how Zeitro Strata makes income verification easy.

As a loan officer for over a decade, I see homebuyers mix up take-home pay with pre-tax earnings almost every day. Understanding your true cash flow is absolutely crucial before buying a house. To figure out exact mortgage income requirements, lenders need pristine math.

That's where tools like Zeitro Strata come in handy. It allows you to upload financial documents to automatically verify and calculate earnings, keeping the entire process incredibly convenient and secure.

Key Takeaways

Gross vs. Net: Banks use your pre-tax gross earnings for loan approval, but your net pay dictates your realistic household budget.

The 25% Rule: As a personal budgeting guideline, try to keep your total housing payment at or below 25% of your take-home pay.

Smart Tech: Platforms like Zeitro Strata eliminate frustrating math errors by automating income verification.

Let's clear up a massive industry misconception right away.

Banks typically use your pre-tax gross monthly income when evaluating DTI, while your take-home pay is better used for personal budgeting and affordability planning.

As a conservative budgeting rule of thumb, many buyers try to keep housing costs near or below 25% of take-home pay, even though lender underwriting often relies on gross-income-based guidelines such as 28/36.

For variable income such as bonuses, commissions, overtime, or self-employment earnings, lenders usually require documentation that shows the income is stable and likely to continue.

So, where does your net pay actually fit into the puzzle? I always tell my clients to use their after-tax cash to determine personal affordability. It represents what you actually have in the bank for groceries and emergencies. Additionally, if you own a business, underwriters will look closely at the net profit listed on your tax returns.

Finding your true take-home pay isn't as simple as just glancing at the bottom of a pay stub, especially if you have variable paycheck deductions. Over the years, I've developed a straightforward approach to calculate employment income for personal budgeting:

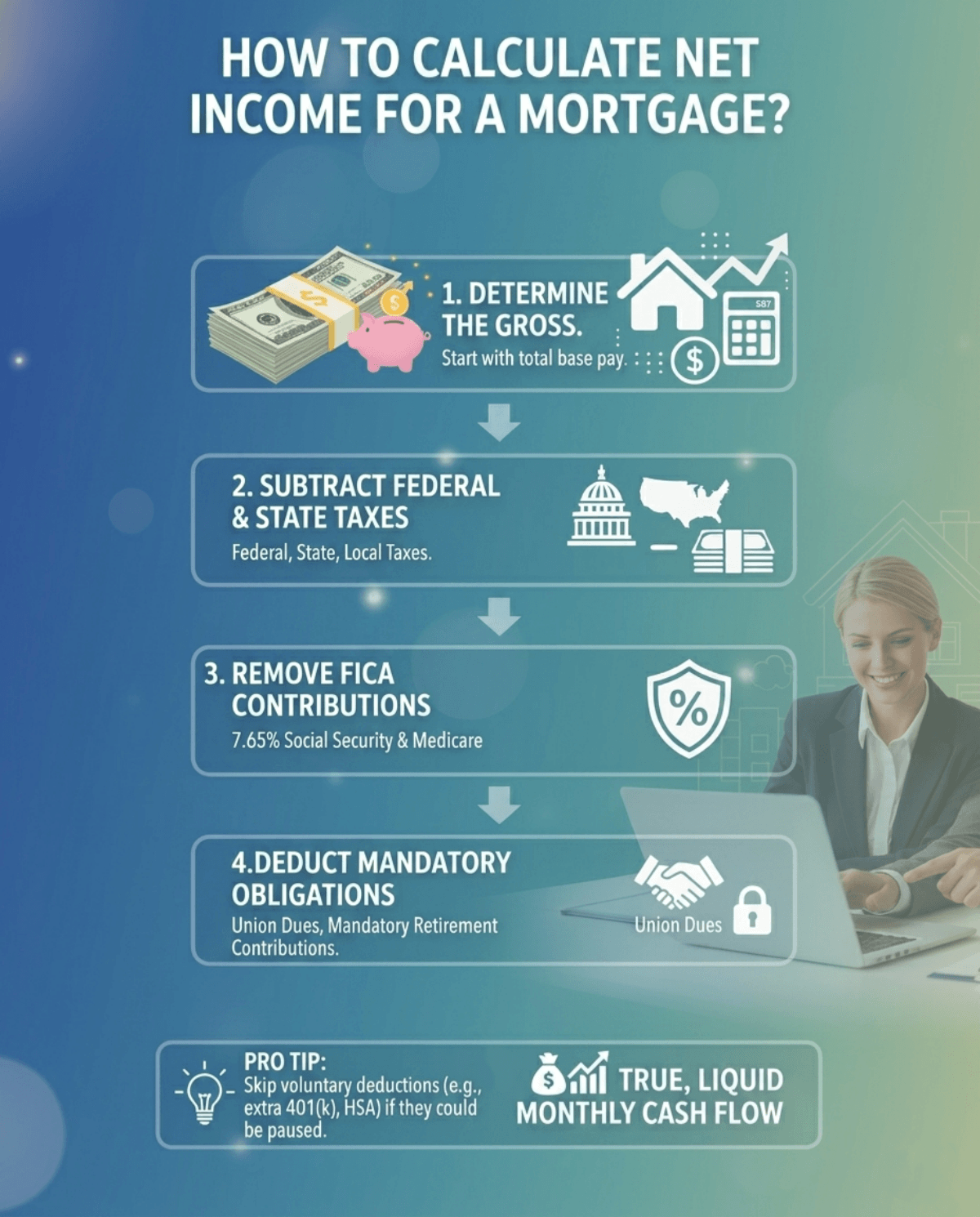

Determine the Gross: Start with your total base pay before anything is touched.

Subtract Federal and State Taxes: To estimate your personal take-home pay, subtract federal, state, and local taxes, FICA, and mandatory deductions from gross income.

Remove FICA Contributions: Subtract Social Security and Medicare, which is 7.65% combined for standard W-2 workers.

Deduct Mandatory Obligations: Take out things you can't easily cancel, like union dues or mandatory retirement contributions.

Pro tip: Skip voluntary deductions like extra 401(k) allocations or health savings accounts if you could technically pause them during a financial pinch. What's left is your true, liquid monthly cash flow.

Examples of Calculating Net Income in a Mortgage

Let's look at two real-world scenarios I see at my desk every week.

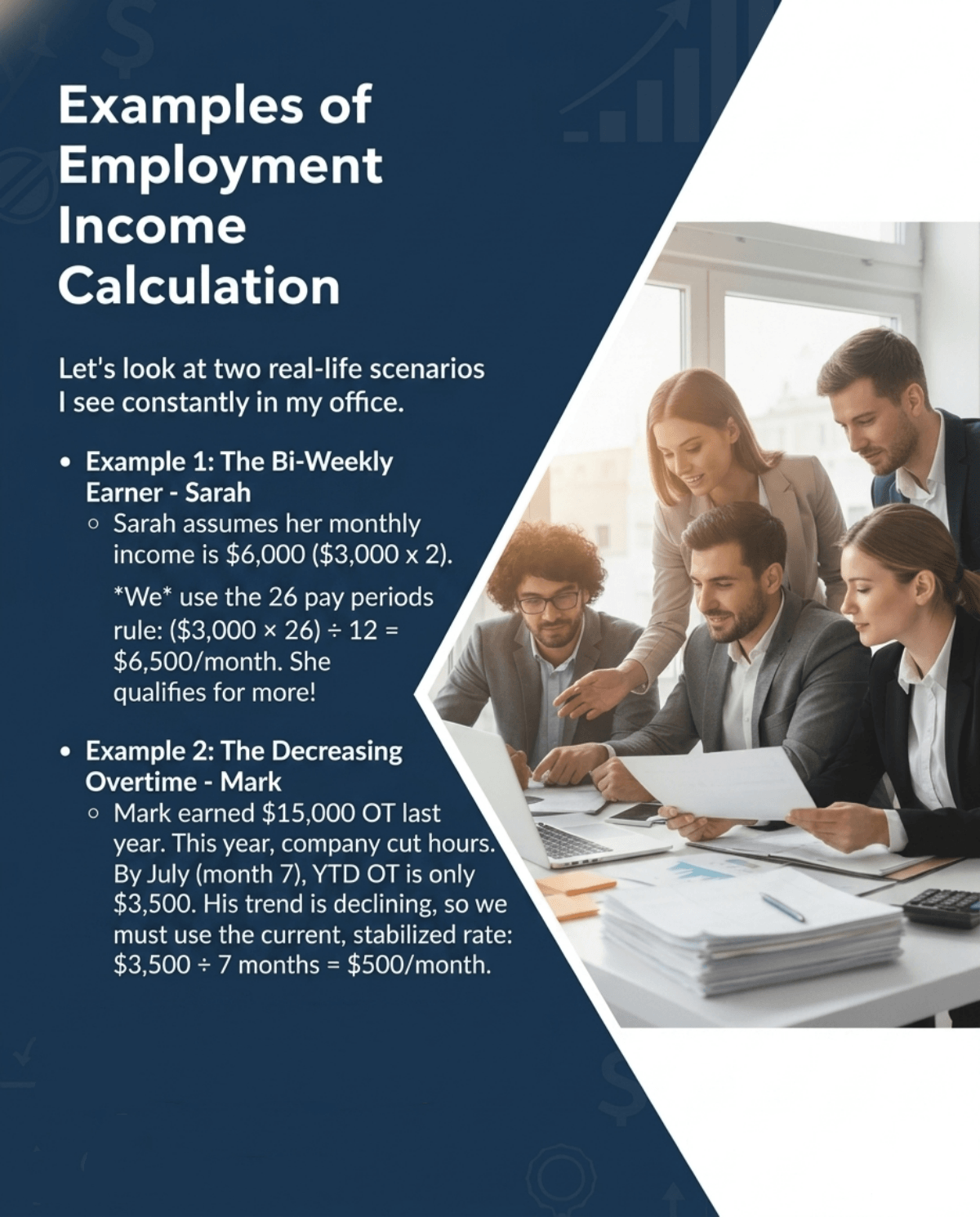

Example 1: The W-2 Salaried WorkerSarah makes $6,000 gross a month. After pulling out $900 for federal and state taxes, $459 for FICA, and $100 for mandatory union dues, her actual usable cash flow is $4,541. That's the specific number she should use to plan her house hunting budget.

Example 2: The FreelancerMark is a graphic designer. As a lender, I don't look at his gross business revenue. Instead, we pull his Schedule C. Last year, his business brought in $80,000, but he wrote off $20,000 in legitimate expenses. His taxable net profit was $60,000. We typically review the most recent two years of tax returns and often average the qualifying income, though specific rules may allow other documentation in certain cases.

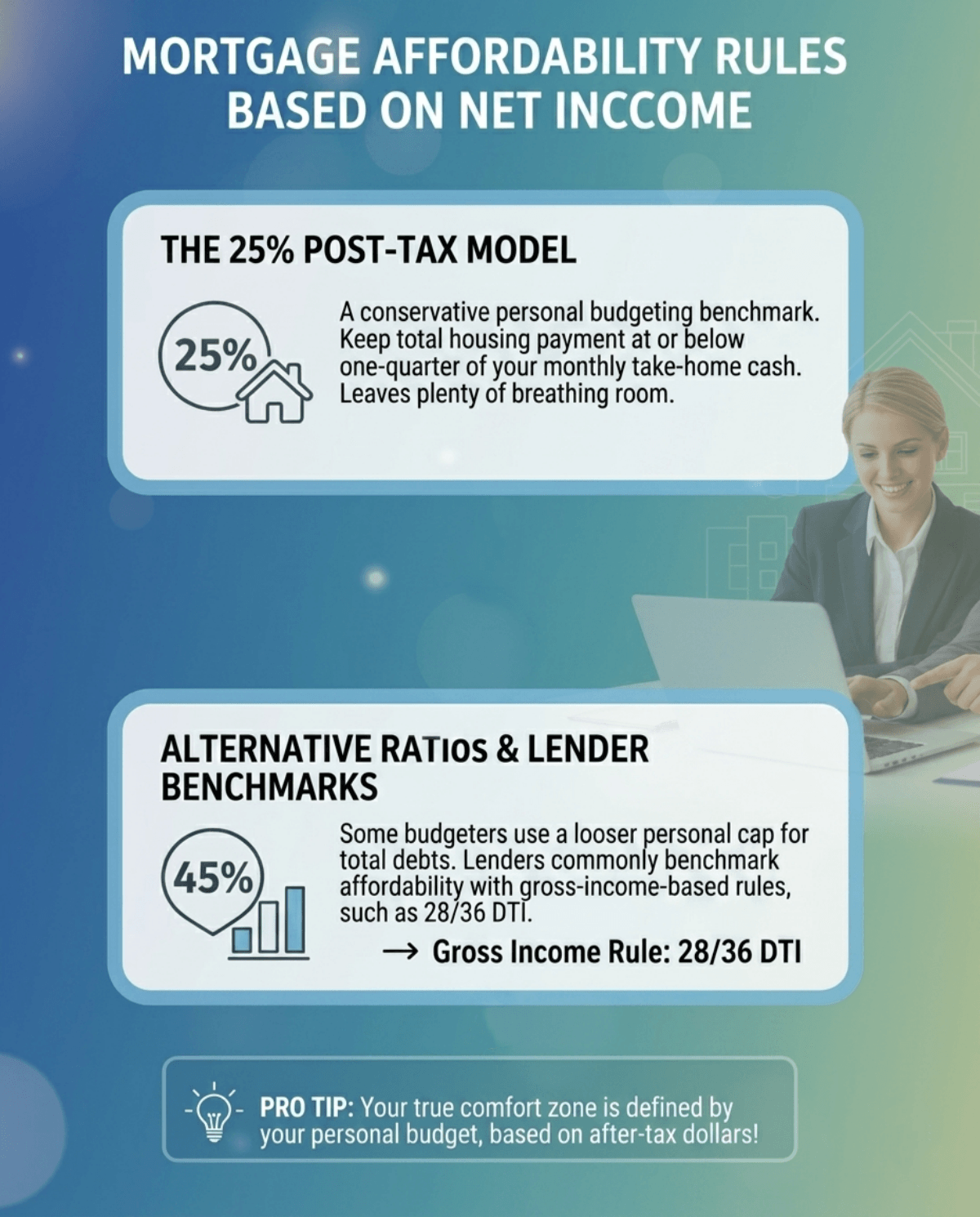

Mortgage Affordability Rules Based on Net Income

Once you know your exact take-home pay, how much house can you actually afford? While lenders focus strictly on your gross DTI, your personal comfort zone depends heavily on your after-tax dollars. I always advise borrowers to follow these practical guidelines when deciding what percentage of income should go to a mortgage:

The 25% Post-Tax Model: As a conservative personal budgeting benchmark, try to keep your total housing payment at or below one-quarter of your monthly take-home cash. This leaves plenty of breathing room for life's unexpected curveballs.

Alternative 45% Ratio: Some budgeters use a looser personal cap for total debts, but lenders commonly benchmark affordability with gross-income-based rules such as 28/36.

Tips for Specific Income Types

Not everyone gets a predictable, boring salary. If your earnings fluctuate, the math gets a bit trickier. Here are some insider tips I share with non-traditional earners:

Self-Employed Borrowers: As mentioned, underwriting relies heavily on your Schedule C net profit. We will almost always average your past two years of tax returns. If you want a deep dive into this, here's exactly how to calculate self-employed income.

Hourly Employees: Use your year-to-date pay stubs, recent payroll history, and prior income records to estimate a stable qualifying income.

Bonuses and Commissions: Don't rely on last month's big commission check. You generally need a documented history showing that the bonus, overtime, or commission income is stable and likely to continue, often supported by about two years of records.

FAQs About Calculating Net Income in a Mortgage

Q1. How much net income should go towards a mortgage?

For true peace of mind, try not to spend more than 25% of your after-tax earnings on your monthly housing payment. While banks might approve you for a higher amount based on pre-tax figures, staying near this threshold prevents you from becoming "house poor."

Q2. How do you calculate income for a mortgage?

Lenders assess your pre-tax gross pay to determine approval limits. However, for your personal budget, subtract taxes, FICA, and non-cancelable deductions from your gross earnings to find your usable take-home pay. Both numbers are essential during the homebuying journey.

Q3. How much income to qualify for a $500,000 mortgage?

It depends heavily on current interest rates, your down payment, and outstanding debts. Assuming a 20% down payment and average current rates, you'd typically need a gross annual salary of around $120,000 to $140,000 to comfortably qualify.

Q4. Does the income calculation include bonuses and overtime?

Yes, but with strict conditions. You cannot simply add a recent bonus to your base pay. Underwriters require a consistent, two-year history of receiving overtime, bonuses, or commissions before they will average that money into your qualifying application.

Q5. Why do lenders look at gross income instead of net income for DTI?

Taxes and deductions vary wildly depending on individual filing statuses, 401(k) choices, and the mortgage interest deduction you might claim later. Using gross pay provides lenders with a standardized, equitable baseline to evaluate every applicant's true earning power.

Conclusion

Nailing down your exact earnings, whether gross for the lender or net for your personal budget, is the absolute foundation of a stress-free home purchase. One tiny miscalculation can delay a closing or push you into a house you realistically can't afford. That's exactly why modern loan originators and savvy homebuyers are moving away from manual math.

I highly recommend exploring Zeitro Strata. It completely transforms the tedious underwriting process. By uploading your financial documents, Zeitro Strata can help extract information, verify details, and support income analysis more efficiently. It saves hours of frustrating paperwork and eliminates costly human errors. Let smart technology handle the complex math so you can focus entirely on finding your dream home.

Find out exactly how to calculate your gross monthly income for a mortgage. Read our expert guide covering salaried, hourly, and self-employed pay.

As loan professionals, we see homebuyers struggle with income math every day. Nailing this calculation accurately is the critical first step to getting approved.

While manual math can lead to stressful errors, we highly recommend Zeitro Strata. It safely allows you to verify income requirements and simply upload your documents to auto-calculate everything, making the entire approval process incredibly easy and secure.

Key Takeaways

Your gross earnings before taxes determine your maximum borrowing power.

Calculation methods vary depending on whether you are salaried, hourly, commission-based, or self-employed.

Many lenders average variable pay, such as bonuses and overtime over the past 24 months, although some programs may allow shorter histories if the income is stable and likely to continue.

Preparing the right tax and income documents upfront prevents frustrating underwriting delays.

How Gross Income is Used in a Mortgage?

Why do lenders care so much about your top-line number? Put simply, your gross earnings—the money you make before taxes and health insurance deductions—serve as the absolute foundation of your loan application.

We use it to evaluate your repayment ability and establish your Debt-to-Income (DTI) ratio. This ratio tells our underwriting team if you can comfortably afford a new housing payment alongside your current credit cards and car loans. Ultimately, your pre-tax pay is the primary metric for meeting specific mortgage income requirements and determining the maximum loan amount you qualify for.

Let's break down the math. Lenders do not treat all paychecks the same way. Here is how you should figure out your monthly earnings based on your specific job type:

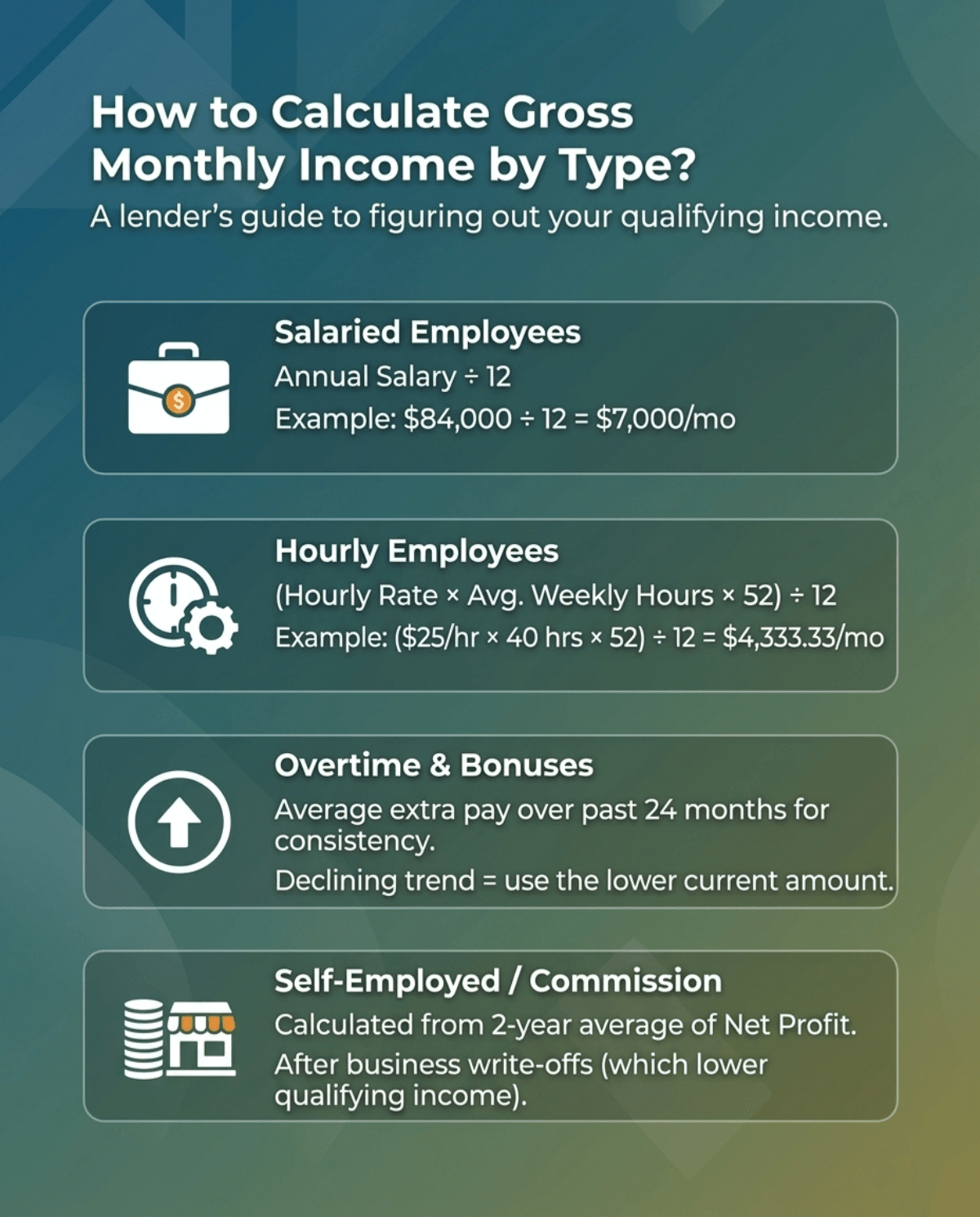

Salaried Employees: This is the easiest scenario when you need to figure out how to calculate employment income. Just take your base annual salary and divide it by 12. For example, if your salary is $84,000, your gross monthly income is $7,000($84,000 ÷ 12 = $7,000).

Hourly Employees: Don't just multiply a good week by four. Multiply your hourly rate by your average weekly hours worked, multiply that by 52 weeks, and finally divide by 12 months. For instance: $25/hour × 40 hours × 52 weeks ÷ 12 = $4,333.33 per month.

Overtime and Bonuses: We look for consistency. Lenders will generally average this extra pay over the past 24 months. However, if we notice your overtime hours are dropping recently, conservative lending guidelines require us to use the lower, current amount rather than the historical average.

Self-Employed/Commission: We do not look at your gross business revenue. Instead, we use the net profit from your tax returns (after business write-offs) averaged over the last two years. If you run a business, learning how to calculate self-employed income is vital, as heavy tax deductions will actively lower your qualifying income.

Glossary to Know Related to Gross Income

The mortgage industry has its own language. Here are a few essential terms we use daily on the processing floor:

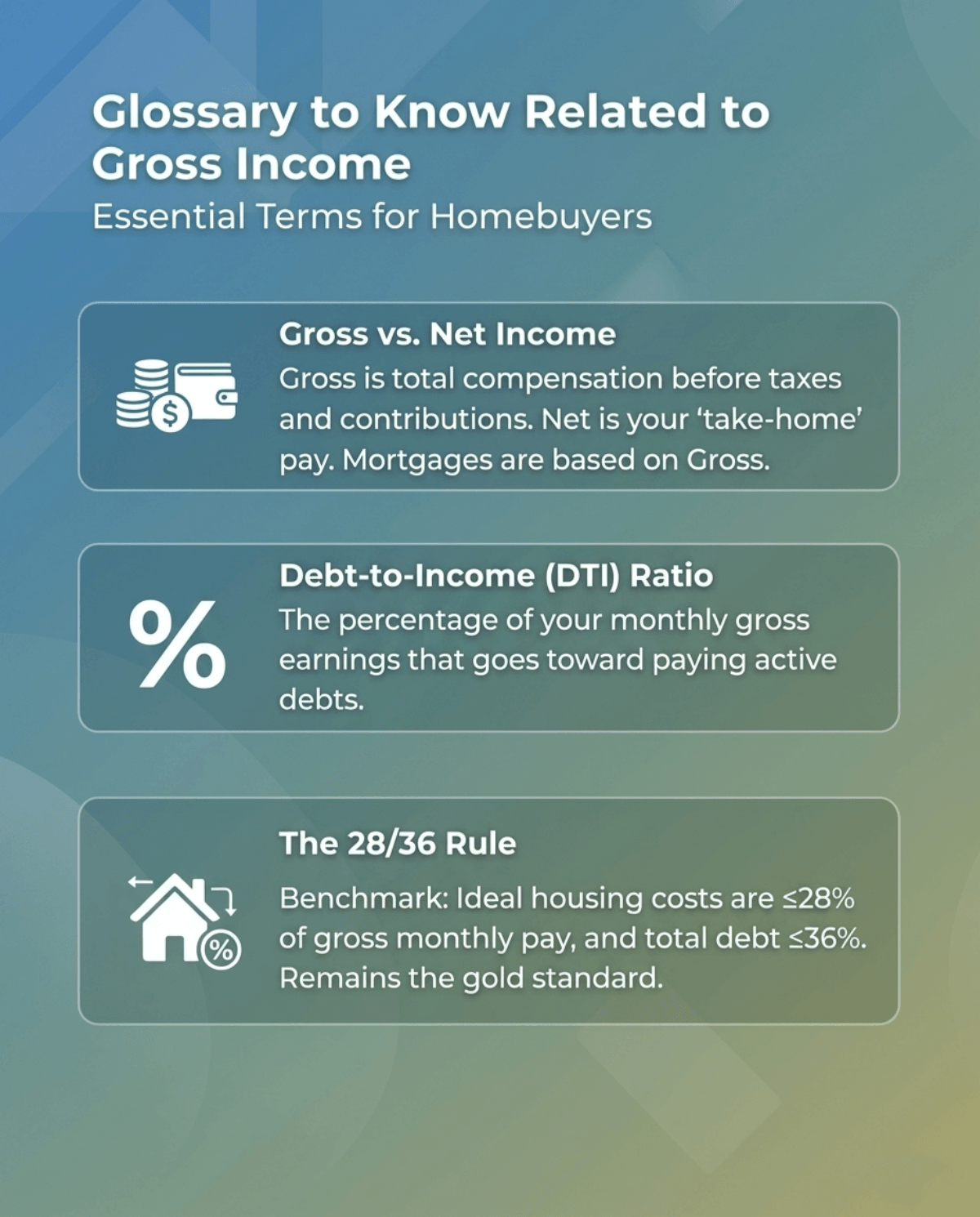

Gross vs. Net Income: Gross is your total compensation before any taxes or retirement contributions are taken out. Net is your "take-home" pay. Mortgages are almost exclusively based on your gross figure.

Debt-to-Income (DTI) Ratio: The percentage of your monthly gross earnings that goes toward paying active debts.

The 28/36 Rule: A classic underwriting benchmark. Ideally, no more than 28% of your gross monthly pay should go toward housing costs, and no more than 36% toward total debt. If you are wondering what percentage of income should go to a mortgage to keep your family's finances healthy, this rule remains the gold standard.

Documents Needed for Mortgage Verification

Whenever clients ask me how to speed up their clear-to-close, my answer is always the same: have your paperwork ready upfront. Providing clean, complete documentation prevents your file from sitting in limbo.

Here is a quick checklist of what you need to gather:

W-2 Forms: The last two years for standard employees.

1099 Forms: The last two years if you are a freelancer or contractor.

Recent Pay Stubs: Usually covering your most recent 30-day pay period.

Tax Returns (1040s): Your complete personal and business returns for the past two years (especially vital for self-employed borrowers).

Bank Statements: The last 60 days of active accounts to verify your cash reserves.

FAQs About Calculating Gross Income in Mortgage

Q1. Do mortgage lenders look at gross or net income?

We primarily use your gross earnings—the amount before taxes. The major exception is for self-employed borrowers, where we must evaluate the net profit shown on your filed federal tax returns.

Q2. Can I include overtime or bonuses in my gross income?

Yes, but it must be reliable. We require a consistent two-year history of receiving overtime or bonuses. If it is a one-time payout, we generally cannot count it toward your qualifying income.

Q3. How does rental income affect my gross monthly income?

For many loan programs, lenders count about 75% of gross rental income to account for vacancy, maintenance, and management expenses. The remaining 25% is automatically subtracted to account for potential vacancies and routine property maintenance.

Q4. At what income level do I lose the mortgage interest deduction?

Tax laws update frequently, and limitations are often tied to your total loan size. However, you can check specific IRS guidelines to see the exact income level you lose the mortgage interest deduction based on your tax filing status.

Q5. What if my income is variable or commission-based?

For variable income, underwriters often review two years of documentation, but some programs may accept shorter histories when the income is stable and expected to continue.

Conclusion

Getting your gross income right isn't just about passing the underwriter's desk. It dictates the loan amount and the interest rates you can actually secure. As mortgage professionals, we've seen too many buyers stress over scratching out math on a notepad, only to realize they miscalculated their usable earnings.

You don't have to do this the hard way. We strongly recommend Zeitro Strata. Instead of guessing, you can securely upload your pay stubs and tax forms in seconds. The platform automatically extracts the data and calculates your exact qualifying income based on current banking standards. It's fast, incredibly secure, and completely removes the guesswork from your homebuying journey.

At what income level do you lose the mortgage interest deduction? Good news: there's no direct cap! Learn how loan limits and 2026 rules impact your return.

As a loan professional, I hear the same anxious question every tax season: "Am I making too much money to deduct my mortgage interest?" Borrowers desperately want to maximize refunds, yet panic sets in when they fear a salary bump might strip away their homeowner benefits.

Let me give you some peace of mind. You don't just "lose" this valuable tax break merely by getting a raise. However, the interplay between your earnings, loan size, and the latest 2026 tax regulations can significantly alter how much you actually save. In this guide, I'll definitively answer how income limits affect your mortgage deduction and what you must know before filing.

Key Takeaway

There is no direct, absolute income limit that completely disqualifies you from claiming the mortgage interest deduction.

You must actively choose to itemize deductions rather than taking the standard route to utilize this benefit.

The actual restriction comes from loan amount limits, which are permanently capped at $750,000 for recent mortgages.

High earners in the top tax bracket face slightly reduced deduction values under the new 2026 tax laws.

At What Income Level Do You Lose Mortgage Interest Deduction?

The short answer is: you never entirely lose the mortgage interest deduction simply because your salary hits a certain threshold. The IRS doesn't enforce a direct income cap that strips away your eligibility. Instead, restrictions are heavily tied to your total loan amount.

However, high-income earners face a nuanced reduction. Under the recently passed One Big Beautiful Bill Act (OBBBA) impacting 2026 taxes, the old "Pease Limitation" was replaced. Now, if your earnings place you in the top 37% bracket (over $640,600 for single filers or $768,700 for joint filers in 2026), itemized deductions for those in the 37% bracket are reduced by 2/37 of the lesser of total itemized deductions or the amount by which income exceeds the 37% bracket threshold, effectively limiting the tax benefit to about 35 cents per dollar at the top marginal rate.

You aren't losing the write-off entirely, but its overall power is slightly watered down. Your Adjusted Gross Income (AGI) dictates the benefit's strength, not your right to claim it.

What is the Mortgage Interest Deduction?

Let's break this down into simple terms. The mortgage interest deduction is a lucrative tax incentive designed by the federal government to encourage homeownership. It allows eligible homeowners to subtract the interest they pay on their home loan directly from their taxable income, effectively lowering their annual tax bill.

To claim this write-off, the property must be your primary residence or a designated second home. You can't use it for a third house or purely investment properties. When tax season rolls around, you won't take the standard route. Instead, you must itemize your expenses using IRS Schedule A.

Your lender will send you a Form 1098, which clearly outlines exactly how much interest you paid over the prior year. By reporting this figure, you shield a portion of your hard-earned money from being taxed.

Itemized vs. Standard Deduction: How It Impacts Your Mortgage Interest

Many borrowers I work with are baffled when their accountant tells them they shouldn't write off their mortgage interest. The reason usually boils down to simple math: Itemized vs. Standard Deduction.

You can only claim housing interest if your total itemized deductions, which include mortgage interest, state and local taxes (SALT), and charitable donations, are greater than the IRS standard deduction. For the 2026 tax year, the standard deduction is $16,100 for single filers and $32,200 for married filing jointly.

If a married couple paid $20,000 in mortgage interest and has no other major deductions, their total itemized amount ($20,000) falls well short of the $32,200 standard threshold.

In this scenario, they will rationally choose the standard deduction to save more money. They didn't lose the benefit due to income. They voluntarily bypassed it because the standard deduction offered a better deal.

Factors that Affect the Mortgage Interest Deduction

While your salary doesn't directly disqualify you, several other critical elements absolutely dictate how much interest you can write off. Here are the true limiting factors:

Loan Amount Limits: For mortgages originated after December 15, 2017, you can only deduct interest on the first $750,000 of your mortgage debt ($375,000 if married filing separately). The OBBBA made this $750k cap permanent.

Loan Purpose: The IRS strictly mandates that the borrowed funds must be used to buy, build, or substantially improve the property securing the loan. If you do a cash-out refinance to pay off high-interest credit cards or buy a boat, that specific portion of the interest is not deductible.

Filing Status: Whether you file as single, married filing jointly, or head of household changes your standard deduction baseline, which directly influences whether itemizing your mortgage interest is financially beneficial.

FAQs About Income Level Losing Mortgage Interest Deduction

Q1. Is there an income limit for deducting mortgage interest?

No, there is no hard income limit that entirely strips away your eligibility to deduct mortgage interest. However, if your income places you in the highest 37% tax bracket (over $640,600 for singles in 2026), new tax rules slightly reduce the value of your overall itemized deductions to 35 cents per dollar. You keep the deduction, but the relative tax-saving power is modestly restricted.

Q2. Why can't I claim my mortgage interest on my taxes?

The two most common reasons you can't claim it are math and loan purpose.

First, if your total itemized expenses don't exceed the generous standard deduction, it makes no financial sense to claim it.

Second, if you utilized a cash-out refinance for personal expenses like a vacation or a vehicle, rather than improving your home, that interest becomes completely ineligible for IRS tax benefits.

Q3. Can I write off 100% of my mortgage interest?

Yes, provided your situation fits within IRS guidelines. You can write off 100% of the interest paid if your total mortgage debt is under the permanent $750,000 cap, the loan was used strictly for purchasing or improving your primary or secondary home, and your total itemized deductions exceed your standard deduction. Any debt exceeding that $750,000 threshold will only yield a prorated deduction.

Q4. Is it worth it to deduct mortgage interest on taxes?

It strictly depends on your personal financial footprint. If your combined deductible expenses, like housing interest, substantial charitable contributions, and eligible state and local taxes, surpass the standard deduction ($32,200 for joint filers in 2026), it is absolutely worth the effort to itemize. Otherwise, taking the standard route is much faster, less complicated, and yields a larger tax return.

Q5. How much mortgage interest can I deduct on my taxes?

You can deduct the exact amount of interest paid on up to $750,000 of qualified principal debt for your home. You don't need to guess this number. Your loan servicer will mail you a Form 1098 early in the year detailing the precise interest paid. For 2026 returns, qualifying private mortgage insurance (PMI) premiums paid after December 31, 2025, are treated as deductible home mortgage interest.

Conclusion

Ultimately, your income level won't outright disqualify you from the mortgage interest deduction. The true deciding factors are the size of your loan, how you utilized the funds, and whether your total itemizable expenses surpass the standard deduction threshold. As tax codes continually evolve, navigating these rules can feel incredibly overwhelming for any homeowner.

If you are unsure how these complex IRS changes impact your household budget, I strongly recommend consulting a licensed CPA for personalized tax strategy. Additionally, I encourage you to reach out for a free consultation with a local loan officer. We can help you structure future home purchases or refinancing strategies to maximize your financial leverage and keep more money in your pocket.

Master mortgage income requirements with our expert guide. We break down DTI, income rules, Non-QM loans, and the exact numbers needed for approval.

Facing today's elevated home prices and 2026 mortgage rates sitting near 6.5%, I hear the same anxiety from homebuyers every day: "Do I actually make enough to get approved?"

As a loan professional, I always tell my clients that understanding the exact mortgage income requirements and lender guidelines before applying is your strongest weapon. Let me take you behind the underwriter's desk to reveal exactly how we evaluate your earnings.

Key Takeaways

Loan types matter: Conventional, FHA, and Non-QM loans each weigh your earnings differently. What gets denied by one program might easily be approved by another.

It's not just what you make: Underwriters scrutinize your Debt-to-Income (DTI) ratio and residual income just as closely as the gross pay on your check.

Calculations are complex: The 2026 guidelines around self-employment and variable pay are incredibly strict. I highly recommend using specialized tools like Zeitro Strata or Zeitro Mortgage Income Calculator to verify your actual qualifying numbers rather than just guessing.

Mortgage Income Requirements By Loan Types

When I sit down with a new client, the first thing we look at isn't just their salary—it's matching that income profile to the right loan program.

Conventional Loans: Backed by Fannie Mae and Freddie Mac, these are the industry gold standard. They generally demand a tighter back-end DTI (usually capped around 45% to 50%) and a front-end DTI of no more than 28%, and rely heavily on consistent, traditional W-2 income.

FHA & VA Loans: If your debt is a bit higher, government-backed loans are much more forgiving. FHA loans are fantastic for moderate earners with higher debt loads, while VA loans uniquely focus on "residual income", ensuring veterans actually have enough cash left over after paying the bills.

Non-QM Loans: This is where the mortgage industry is seeing a massive shift in 2026. For freelancers, gig workers, and real estate investors, standard W-2s just don't tell the whole story. Non-QM loans allow us to use 12 to 24 months of Bank Statements or 1099 forms to prove actual cash flow instead of traditional tax returns.

💡 Pro Tip: Since mortgage guidelines are constantly changing and extremely complex in 2026, using automated verification tools like Zeitro Strata can help both borrowers and loan officers verify income accurately and instantly, saving weeks of back-and-forth.

Key Income Metrics to Learn

Underwriters don't look at your bank account the same way you do. We rely on very specific mathematical metrics to decide your fate.

Gross Monthly Income: This is the big one. We base your loan qualifications on your pre-tax income, not the net amount deposited into your checking account after taxes and health insurance are stripped out.

Debt-to-Income (DTI) Ratio: I evaluate two numbers here. The "front-end" DTI is simply your proposed housing expense divided by your gross income. The "back-end" DTI includes all other monthly obligations like car loans, credit cards, and student debt.

Residual Income: Think of this as your real-world survival money. Especially critical for VA loans, this metric calculates the actual dollar amount remaining in your pocket each month after all debts and living expenses are covered.

Key Income Rules to Learn

Beyond the raw numbers, the quality of your earnings is everything. In my experience, this is exactly where most pre-approvals fall apart if you aren't prepared.

The 2-Year Rule: We generally need to see a stable, two-year history in the same line of work. Job hopping isn't a dealbreaker if it's within the same industry, but a sudden career pivot right before applying will raise red flags.

Income Stability & Continuity: Relying on bonuses, commissions, or overtime to boost your budget? You must prove you've received this extra money consistently over the last 24 months, and your employer needs to confirm it's likely to continue.

Self-Employed Hurdles: If you own a business, we look at your net income after all those clever tax write-offs. Many entrepreneurs aggressively write down their business income to save on taxes, only to discover it accidentally disqualifies them for a traditional mortgage.

How to Calculate Your Income Required for a Mortgage?

I rarely encourage buyers to do these calculations entirely by hand. Figuring out exact DTI ratios while factoring in projected property taxes, homeowner's association (HOA) fees, and private mortgage insurance (PMI) gets messy fast.

Instead, I suggest running your numbers through trusted online calculators first to get a solid baseline:

Mortgage Affordability Calculator: This is my go-to recommendation for clients who want to run highly detailed scenarios with various tax and insurance inputs.

NerdWallet Calculator: If you just want a quick, clean, and incredibly user-friendly interface to evaluate your buying power, start here.

Keep in mind, these estimates are just a starting point. Your final approved amount will shift based on your personal credit score and the exact interest rate we lock in.

Examples of Income Required for a Mortgage

To give you a realistic picture, I've mapped out some common loan amounts.

Disclaimer: These estimates assume a 2026 average interest rate of 6.5%, a 20% down payment on a 30-year fixed loan, and a target front-end DTI of 28%. Property taxes and insurance are estimated national averages.

Seeing the numbers laid out like this usually helps my clients realize exactly how their target home price aligns with their current salary.

Mortgage Income Documents Required

The underwriting phase is essentially a massive audit of your financial life. Having your paperwork perfectly organized prevents frustrating closing delays. Here is exactly what I ask my clients to pull together:

For W-2 Employees: I need your most recent 30 days of pay stubs, plus your W-2 forms and full federal tax returns from the past two years.

For Self-Employed/Non-QM: If we are skipping tax returns, I'll need your 1099 forms, 12 to 24 months of complete business or personal bank statements, and a recent Profit & Loss (P&L) statement prepared by your accountant.

General Assets: Regardless of your job type, expect to provide the last two months of bank statements to prove you have the required funds for closing.

Always ensure every document is fully up-to-date and completely unaltered. Missing pages are the number one cause of delays.

FAQs About Mortgage Income Requirements

Q1. How much loan can I qualify for based on income?

Your exact loan limit depends heavily on your Debt-to-Income (DTI) ratio. Most lenders allow a maximum DTI of 43% to 50%, meaning your total monthly debts plus your new mortgage payment cannot exceed half of your gross income.

Q2. What is the minimum income to get a mortgage?

There is actually no legally mandated minimum income required to buy a house. As long as your earnings comfortably cover the monthly payment while keeping your DTI within guidelines, you can qualify. Lower-income buyers often succeed using FHA or USDA loans.

Q3. Can I use bonus, overtime, or commission to qualify?

Yes, but you have to prove a two-year track record of receiving it. We average that extra income over the last 24 months, and your employer must officially indicate that this variable pay is highly likely to continue.

Q4. How do self-employed borrowers prove income?

Traditionally, we analyze your last two years of Tax Returns to find your net qualifying income. However, by utilizing a Non-QM loan, you can bypass tax returns entirely and use 12 to 24 months of business bank statements to prove your real cash flow.

Q5. Can I use rental income or a co-borrower to boost my qualifications?

Absolutely. Adding a co-borrower combines your incomes, which significantly lowers your DTI. Similarly, documented rental income from an investment property or a compliant ADU can be legally added to your gross income to boost your borrowing power.

Final Word

Proving your income is arguably the most critical, and stressful, part of the entire home-buying journey. One simple miscalculation on variable pay or self-employed deductions can easily derail a purchase. Whether you are a homebuyer trying to figure out your realistic budget, or a loan officer wrestling with complex 2026 guidelines, getting the math right on day one saves everyone a massive amount of heartache.

Ready to streamline your mortgage process? Say goodbye to manual calculations and complex guideline checks. Visit Zeitro Strata to verify income securely, accurately, and instantly.

How much of your salary should go to housing? Discover the best percentage of income for a mortgage, compare expert rules, and find your ideal monthly budget.

I recently stumbled down a Reddit rabbit hole on r/RealEstate where a user asked a question keeping millions awake at night: "What percentage of my monthly income should actually go toward my mortgage?" The thread exploded. While internet strangers threw around wild guesses and personal anecdotes, financial experts rely on battle-tested golden rules. Let's break down the exact math so you don't end up house poor.

Key Takeaways

The 28/36 rule is the most universally accepted standard by lenders.

High Cost of Living (HCOL) areas often force buyers to stretch these limits, though it might impact your other investments.

Never calculate based purely on principal and interest. You must factor in hidden expenses like property taxes, homeowner's insurance, and HOA fees to see your true monthly burden.

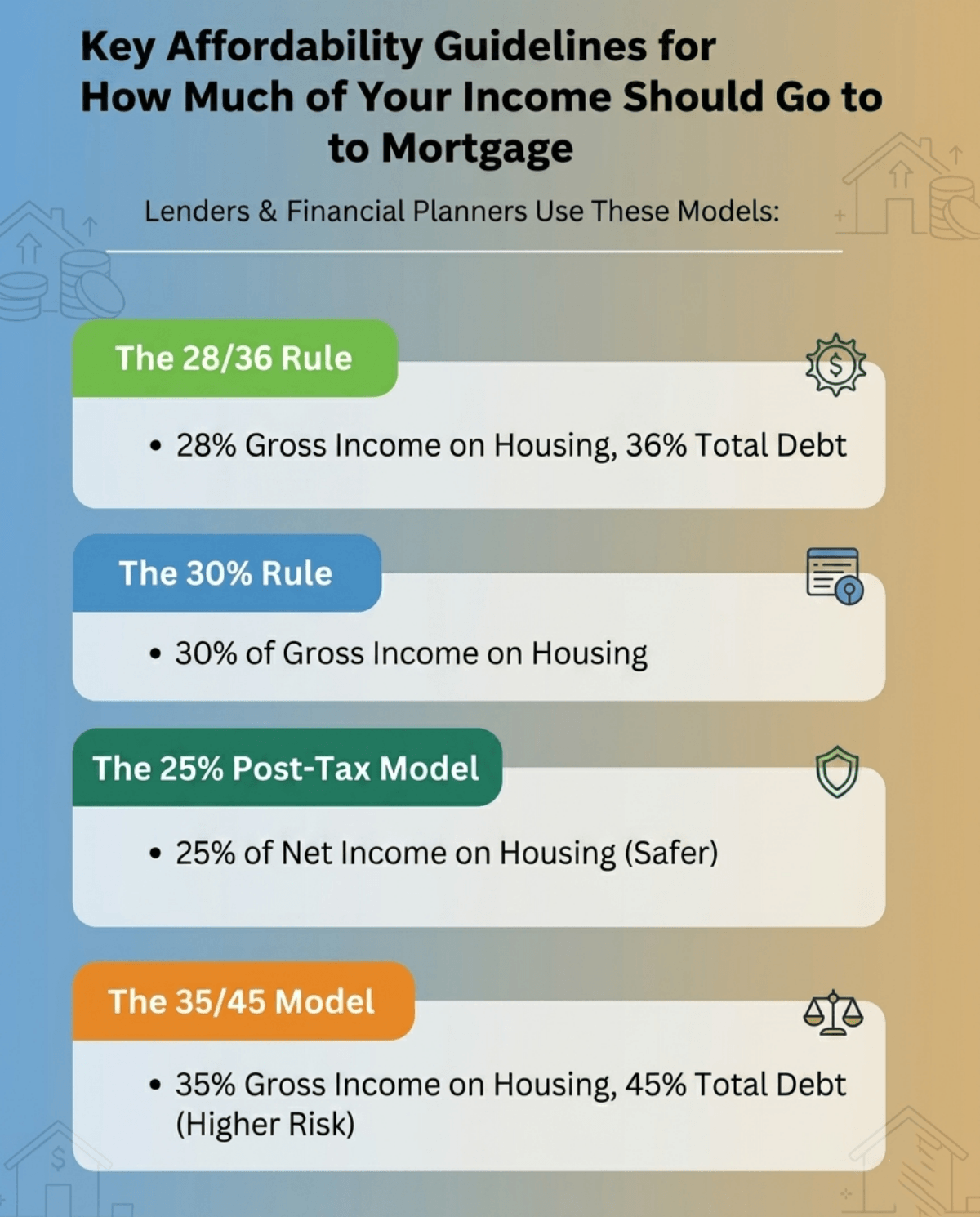

Key Affordability Guidelines for How Much of Your Income Should Go to Mortgage

When I bought my first home, I quickly learned that lenders and financial planners use specific models to determine affordability. Here are the four primary guidelines you should know:

The 28/36 Rule: This is the gold standard in banking. It suggests spending no more than 28% of your gross (pre-tax) income on housing costs, and capping your total debt, including car loans and credit cards, at 36%.

The 30% Rule: A classic rule of thumb stating your housing expenses shouldn't exceed 30% of your gross income. It's simple, but sometimes a bit too broad for modern markets.

The 25% Post-Tax Model: This is my personal favorite and highly recommended by conservative financial gurus. It dictates spending no more than 25% of your net (take-home) pay. It's much safer and leaves plenty of room to build wealth or invest.

The 35/45 Model: Often used by those with high incomes or unique debt structures. It allows up to 35% of pre-tax income for housing and 45% for overall debt. It's lenient, but carries more risk if your financial situation suddenly changes.

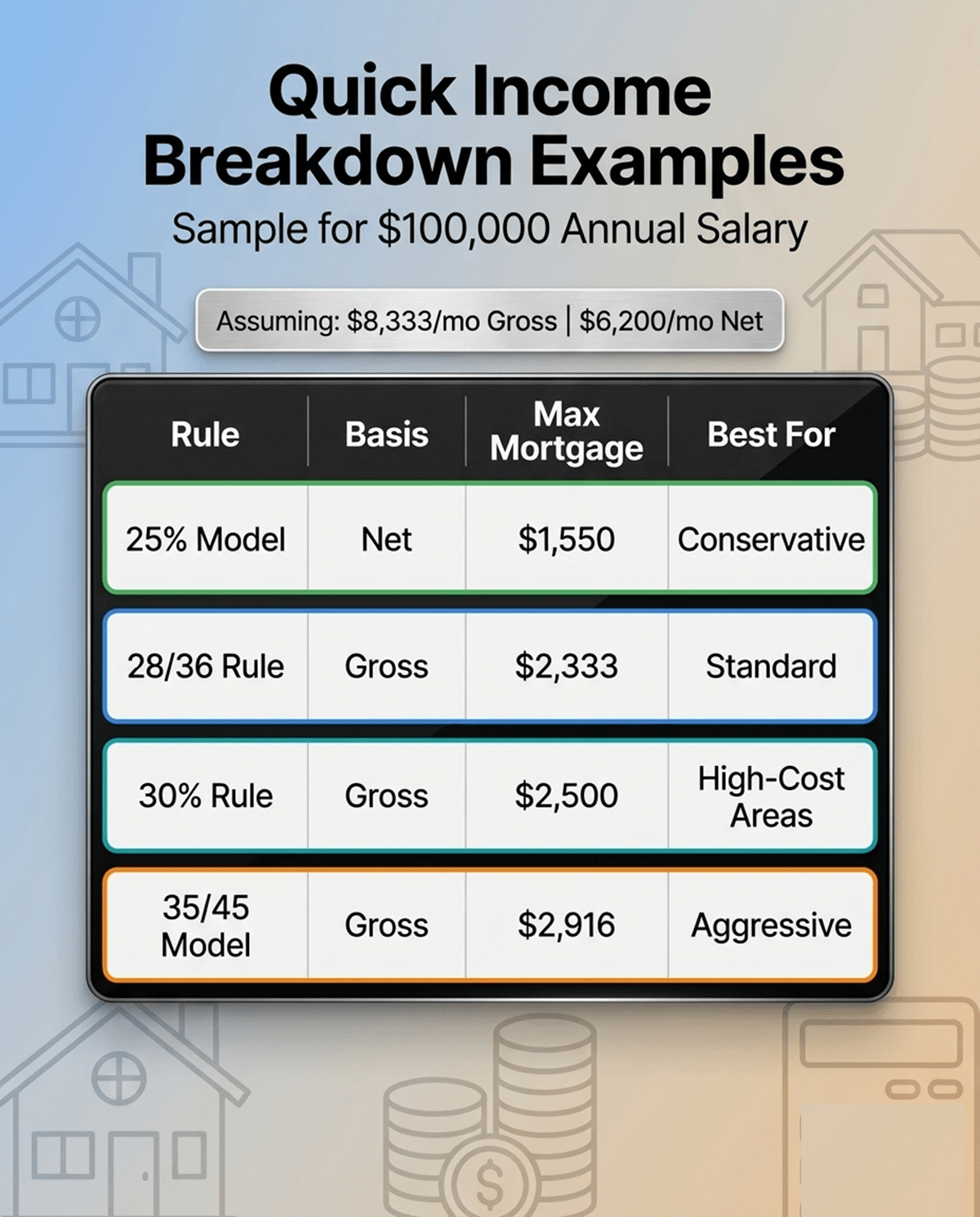

Quick Income Breakdown Examples

To make this crystal clear, let's assume a baseline scenario. Imagine a homebuyer with an annual salary of $100,000. That breaks down to roughly $8,333 in monthly gross income, or about $6,200 in monthly net take-home pay after taxes and basic deductions.

Here is how the maximum monthly mortgage payment shakes out depending on the financial framework you choose:

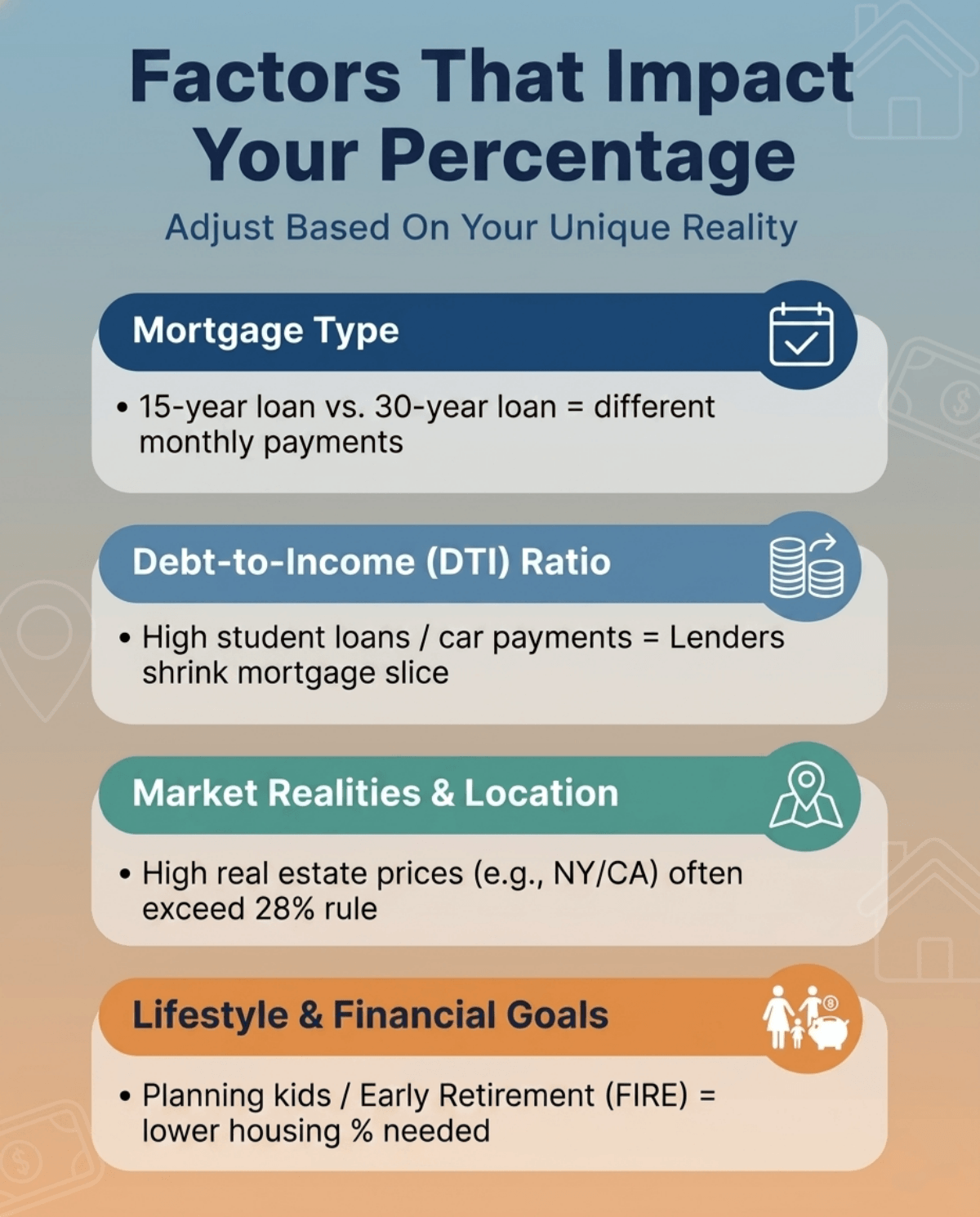

Sticking rigidly to these rules isn't always realistic. You need to adjust based on your unique reality:

Mortgage Type: A 15-year fixed loan will hike up your monthly payment compared to a 30-year fixed, drastically shifting your percentage.

Debt-to-Income (DTI) Ratio: If you're carrying massive student loans or hefty car payments, lenders will drastically shrink the slice of the pie available for your mortgage.

Market Realities & Location: If you live in New York or California, sky-high real estate prices often force buyers to break the 28% rule just to get a foot in the door.