When I first considered transitioning into the mortgage industry, my biggest question was simple: how do loan officers actually get paid, and is the income as high as everyone says? If you are looking to change careers or become a licensed loan officer, understanding the commission structure is crucial. Let's dive straight into how much you can realistically earn and how those paychecks land.

Key Takeaways

Commission Structure: Most loan officers earn a percentage of closed loans, typically ranging from 0.5% to 2.5%.

Diverse Pay Models: Compensation ranges from pure commission to salary-plus-commission.

Regulatory Limits: Federal laws prevent pay variations based on loan interest rates.

Realistic Income: Average annual earnings span from $74,000 to over $180,000 based on loan volume.

Do Loan Officers Get Commission?

Yes, the vast majority of mortgage loan officers are compensated primarily through commissions. In my experience, this commission-driven model is what attracts top-tier talent, as it directly ties your hard work to your earning potential. Depending on the company you work for, you will typically encounter one of three main compensation structures:

Commission-Only: Common at independent brokerages. You receive no base salary, but you earn the highest possible percentage of the loan amount.

Salary Plus Commission: Salary, salary-plus-bonus, fixed-per-loan pay, and commission-based models may all be used at banks and credit unions.

Flat Fee: Some lenders use a fixed amount per loan, and whether that model applies to junior originators depends on the employer.

How Much Commission Does a Loan Officer Make?

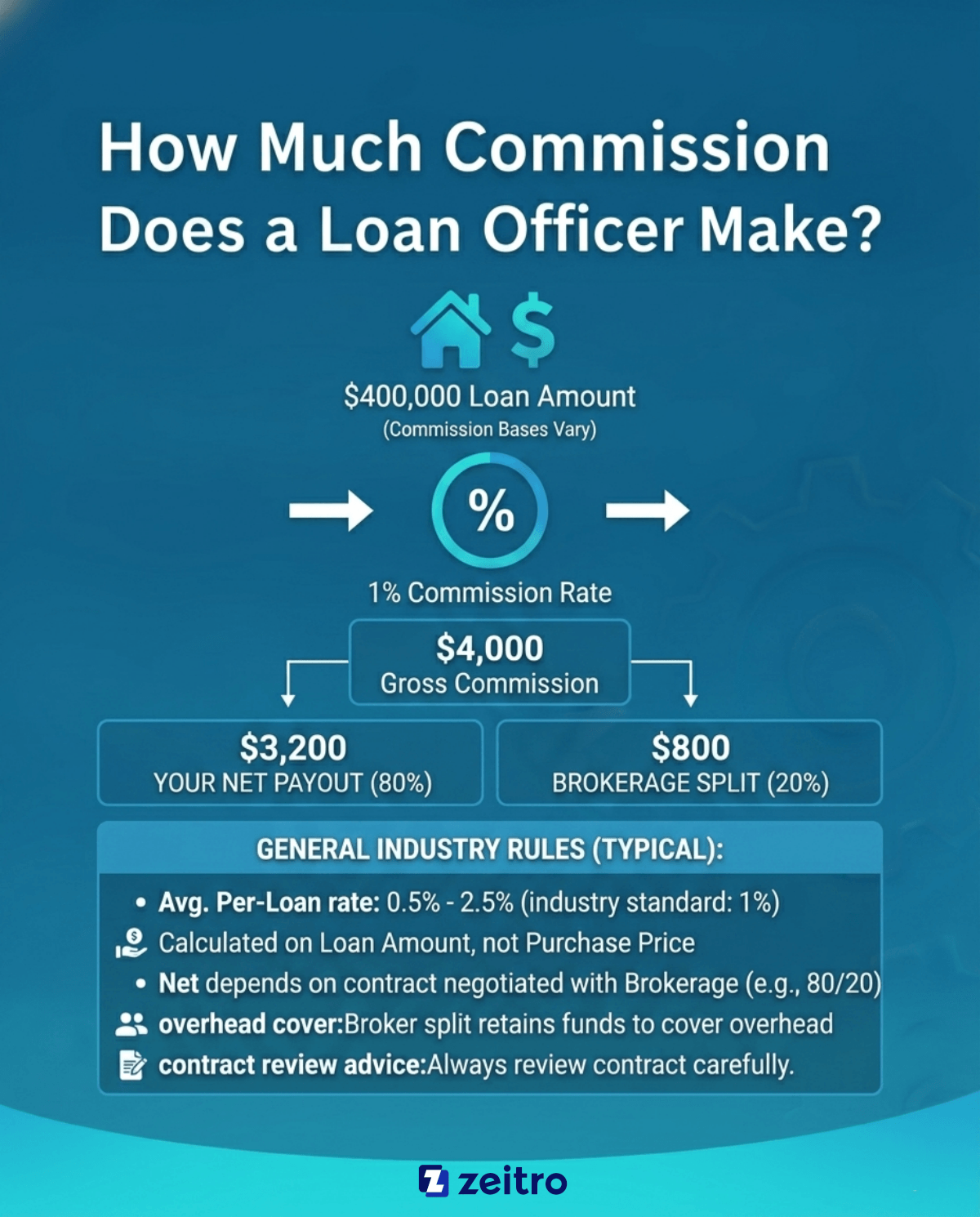

On average, a loan officer earns between 0.5% and 2.5% in commission per closed loan, with 1% being the typical industry standard. In many cases, commission is calculated based on the loan amount rather than the purchase price, though pay structures vary by lender.

To see how the math works, imagine you close a $400,000 mortgage. At a 1% commission rate, the gross commission paid to your brokerage is $4,000. However, you don't pocket all of it. Your net payout depends on your negotiated commission split. If you have an 80/20 split with your broker, you will take home $3,200, while the brokerage retains $800 to cover overhead. In my early days, negotiating a fair split was just as important as generating the leads themselves, so always review your brokerage contract carefully.

Average Salary of Loan Officers

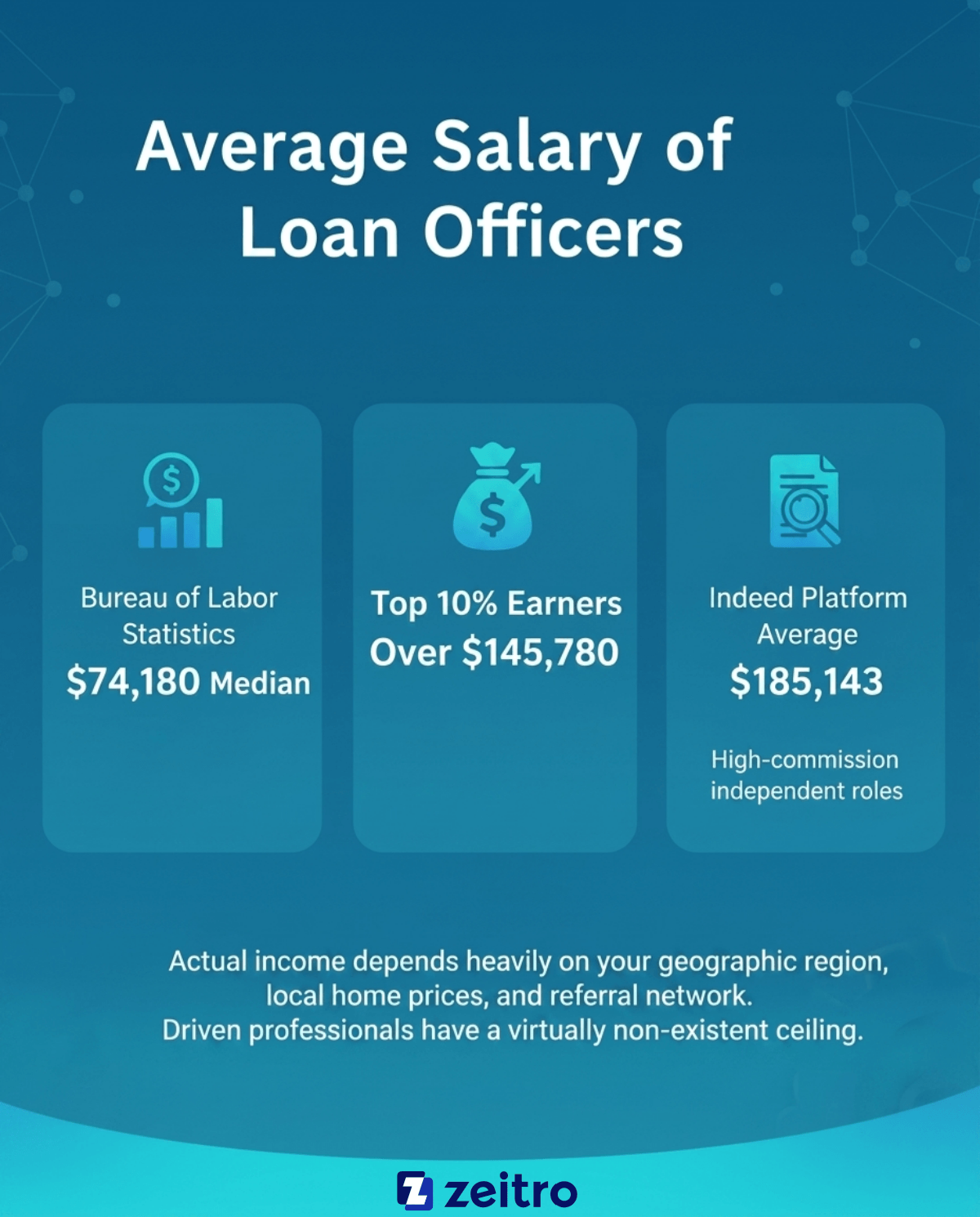

Because commissions fluctuate with the housing market, annual earnings vary widely. According to the U.S. Bureau of Labor Statistics, the median annual wage for loan officers is $74,180, with the top 10% of earners clearing more than $145,780. Meanwhile, job platforms like Indeed report average annual salaries exceeding $185,000, heavily driven by high-volume, commission-only originators.

From what I've seen in the field, your actual income depends heavily on your geographic region, local home prices, and your referral network.

This wide spectrum proves that while the floor is low for those who struggle to find clients, the ceiling is virtually non-existent for driven professionals.

In many commission-based roles, pay is triggered when the loan closes and funds, but some lenders use salary or hybrid compensation structures. Once the loan is funded, the closing agent distributes the gross commission to your brokerage, which then processes your split.

Many brokerages utilize a "draw against commission" system. This means they provide you with a regular advance payment to cover living expenses, which is later deducted from your earned commissions. Federal rules prohibit mortgage loan originator compensation from varying based on loan terms or conditions, including interest rate, fees, or other covered terms.

FAQs About Loan Officer Commission

Q1. How much commission do loan officers make on a $500,000 loan?

On a $500,000 loan, a standard 1% commission generates $5,000 gross. If your contract dictates an 80/20 split, you will personally earn $4,000. Under a bank's salary-plus-commission model, you might earn a much lower flat bonus, such as $500 to $1,000, but with a guaranteed base.

Q2. Will MLO be replaced by AI?

No, AI will not replace mortgage loan officers. While automated systems are excellent for processing paperwork, uploading documents, and verifying credit scores, borrowers still demand human guidance. Navigating a mortgage is highly emotional and legally complex. Real estate agents and buyers want a trusted human professional to solve sudden underwriting issues, offer empathy, and negotiate complex financial scenarios.

Q3. Do loan officers get commission in California?

Yes, but California enforces strict labor laws. All California loan officers must receive at least the state's minimum wage of $16.90 per hour for all hours worked, regardless of closed deals. If an MLO is classified as non-exempt, employers must also pay overtime. Thus, pure commission plans in California are highly regulated to protect employee wages.

Q4. How much does a loan officer make per loan?

Typically, a loan officer nets between $2,000 and $5,000 per closed loan. This estimate assumes a standard loan size of $300,000 to $500,000 and a typical commission split, though high-end luxury loans can yield significantly higher single-payday results.

Q5. Do loan officers pay for their own marketing and leads?

It depends on your business model. In my experience, commission-only independent brokers must fund their own marketing, CRMs, and lead generation, which eats into their profits but offers higher commission splits. Conversely, retail bank loan officers receive company-provided leads and marketing support, but accept a much lower commission percentage in return.

Conclusion

Navigating the world of loan officer commission can seem complex at first, but it ultimately offers one of the most rewarding financial paths in the real estate sector. Whether you choose the stability of a retail bank or the unlimited earning potential of an independent brokerage, your success will depend entirely on your work ethic and ability to build strong referral relationships.

If you are ready to take control of your financial future, your next step is to research your state's licensing requirements and prepare for the National Mortgage Licensing System exam. The effort is significant, but the payoff is entirely in your hands.

What is a mortgage loan origination fee? Learn why lenders charge it, see a real cost breakdown (usually 0.5%-1%), and find out how to negotiate it down.

I recently saw a Reddit post from a first-time homebuyer experiencing severe sticker shock. They were borrowing $285,000 but faced a 1.36% origination fee (about $3,835) plus a $1,795 admin fee. That's over $5,600 just to get the loan started!

They panicked, asking if this was normal. If you've just received your Loan Estimate and are staring at similar numbers, don't worry. Let's break down exactly what this fee means and how you can save.

Key Takeaways

Origination fees often fall around 0.5% to 1% of the loan amount, though some lenders charge flat fees or structure costs differently.

This charge covers the lender's administrative work, including underwriting, processing, and document preparation.

You'll pay this fee at closing, but you can sometimes roll it into your loan balance.

Origination costs are highly negotiable. Shopping around and comparing Loan Estimates is the best way to lower them.

What is the Loan Origination Fee on a Mortgage?

Whenever clients ask me about the mortgage loan origination fee, I tell them to think of it like the service charge at a fancy restaurant. Essentially, it is the upfront price you pay a lender or broker for doing the heavy lifting to create, evaluate, and fund your mortgage.

Creating a home loan isn't automated magic. It takes human effort and technology. Lenders have to pull your credit, verify your income, assess the property's risk, and ensure everything complies with federal regulations. The origination fee compensates them for this labor.

Instead of hiding these operational costs entirely within your interest rate, lenders list them out so you know exactly what you're paying for the service itself. While seeing a massive charge on your paperwork is frustrating, understanding that you're paying for a specialized financial service makes it a bit easier to swallow.

Is Mortgage Loan Origination Fee Necessary?

Yes, it typically is necessary. Lenders are running a business, and this fee is one of the ways lenders recover the operational costs of processing your loan, alongside interest income and secondary market revenue.

However, while the cost exists, you don't always have to pay it out of pocket. As I'll explain later, savvy borrowers can use strategic negotiations or lender credits to effectively reduce their upfront cash requirement to zero.

What Does a Loan Origination Fee Cover?

The term 'origination fee' isn't just one single charge. In my experience reviewing closing disclosures, it actually acts as an umbrella term bundling several administrative costs together. Depending on how your lender itemizes things, this fee usually covers:

Application fee: The cost to initiate your file.

Underwriting fees: The heavy analysis of your financial risk and creditworthiness.

Processing fees: Gathering and verifying your documents.

Document preparation fee: Drafting the massive stack of legal paperwork.

Tax service processing fee: Ensuring property taxes are tracked accurately.

Courier and Wire transfer fees: Moving physical documents and funding the loan.

While some lenders bundle multiple administrative costs together, not all of the following are technically part of "origination charges" under CFPB definitions. Items like tax service fees, courier fees, and wire transfer fees are often listed separately under other closing cost sections.

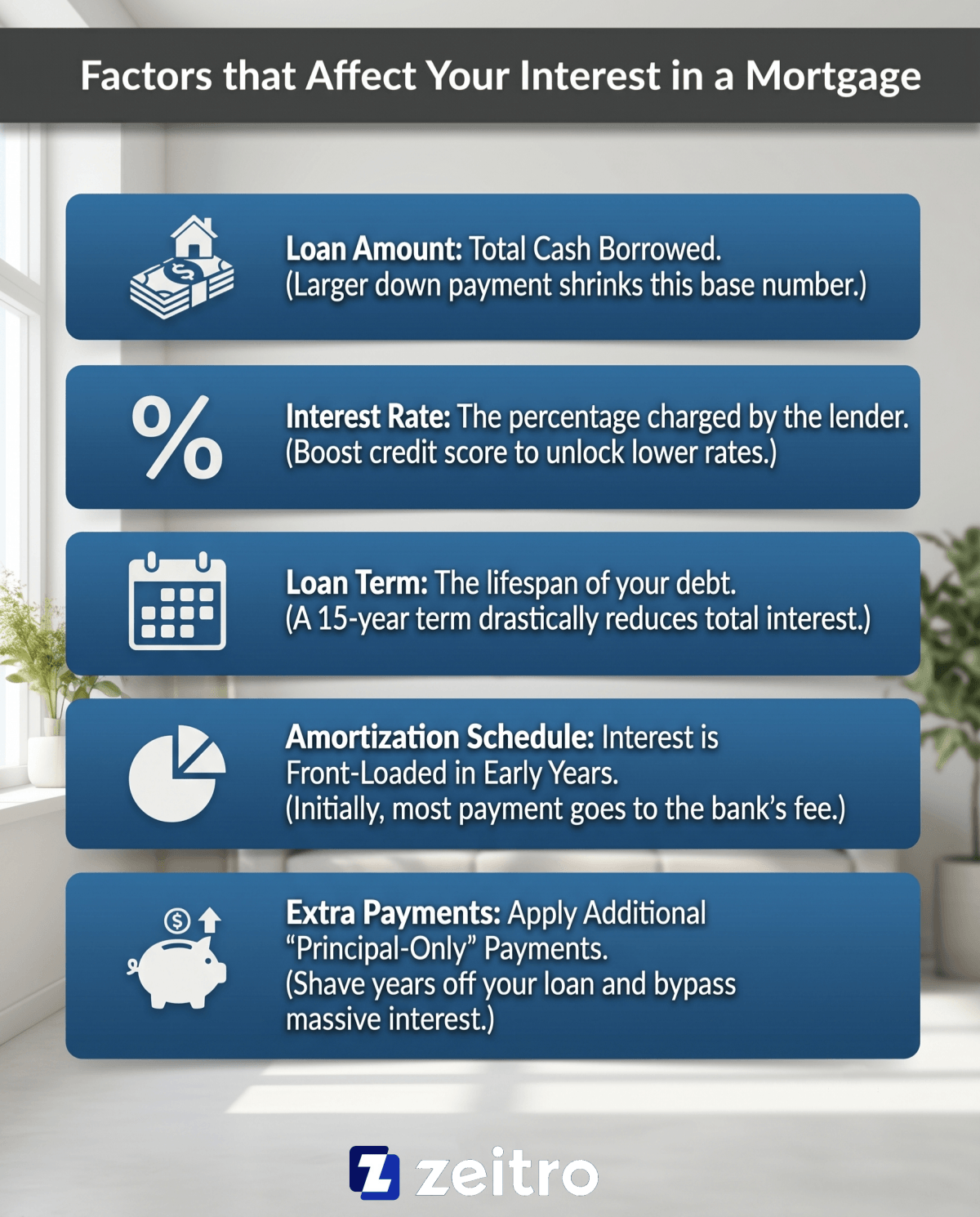

How Much is a Loan Origination Fee?

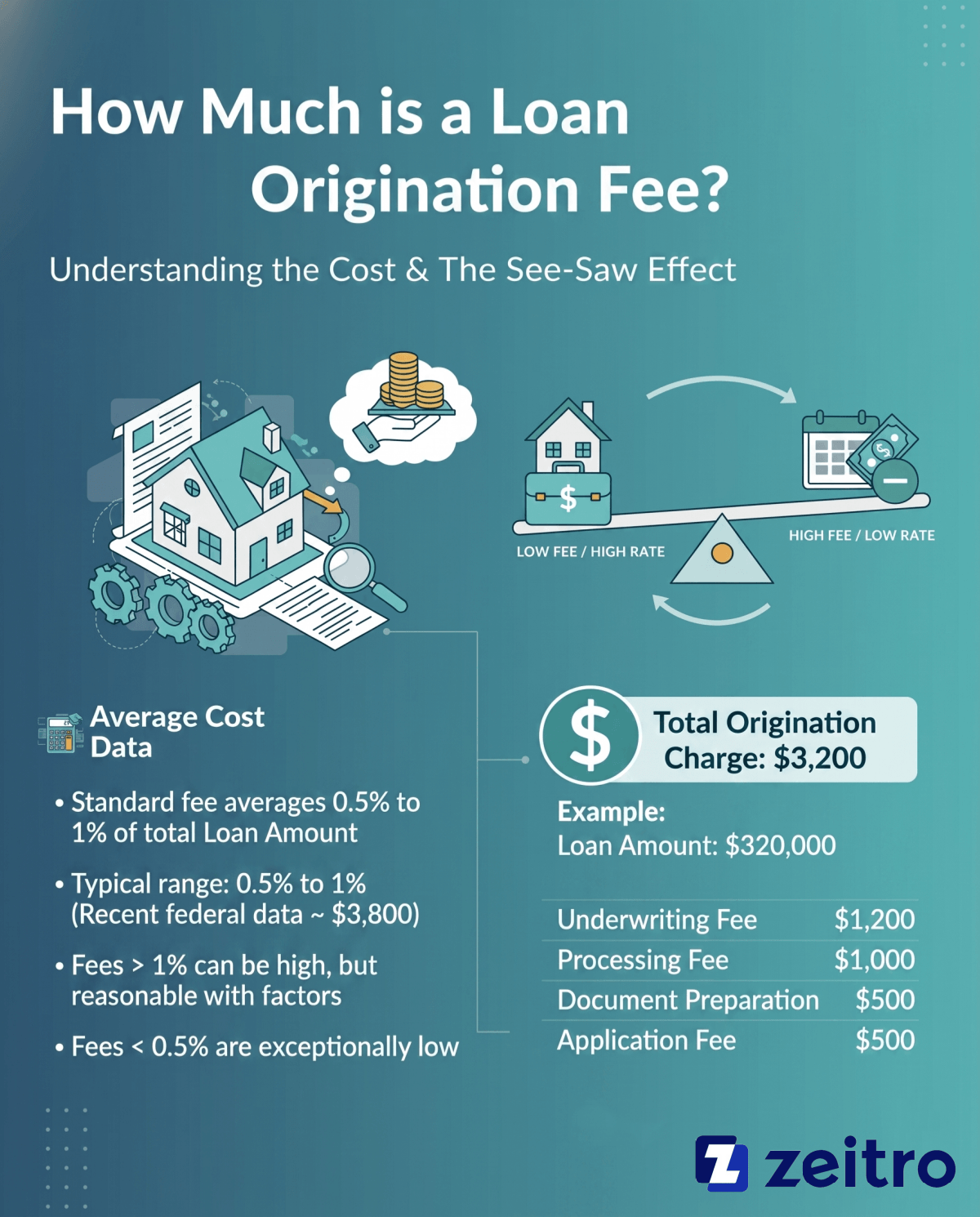

In the U.S. market, a standard loan origination fee averages between 0.5% and 1% of your total loan amount. For context, recent federal housing data shows average origination costs hovering around $3,800.

So, how do you know if you're getting ripped off? If we look back at that Reddit user facing a 1.36% charge plus nearly $1,800 in extra admin fees, that is undoubtedly on the high end. Fees above 1% are on the higher side, but they can be reasonable depending on factors like loan size, credit profile, or whether you're working with a broker. Conversely, anything below 0.5% is considered exceptionally low.

But here is the catch: mortgage pricing is a see-saw. A lender offering a 'low' or 'zero' origination fee isn't doing it out of charity. They are almost certainly charging you a higher interest rate to make their money on the back end. On the flip side, paying a standard 1% fee might secure you a much lower monthly payment. As a borrower, you have to decide if you'd rather pay cash upfront or interest over the next 30 years.

Let's look at a realistic scenario so you can see the math in action. Imagine you are buying a $400,000 house and putting down 20% ($80,000). That leaves you with a mortgage loan amount of $320,000.

If your lender charges a typical 1% origination fee, you will owe $3,200. On your official paperwork, instead of one lump sum, you might see this broken down into a few line items like this:

Underwriting Fee: $1,200

Processing Fee: $1,000

Document Preparation: $500

Application Fee: $500

Total Origination Charge: $3,200

Keep in mind, the fee percentage is always calculated based on the loan amount, never the total purchase price of the home.

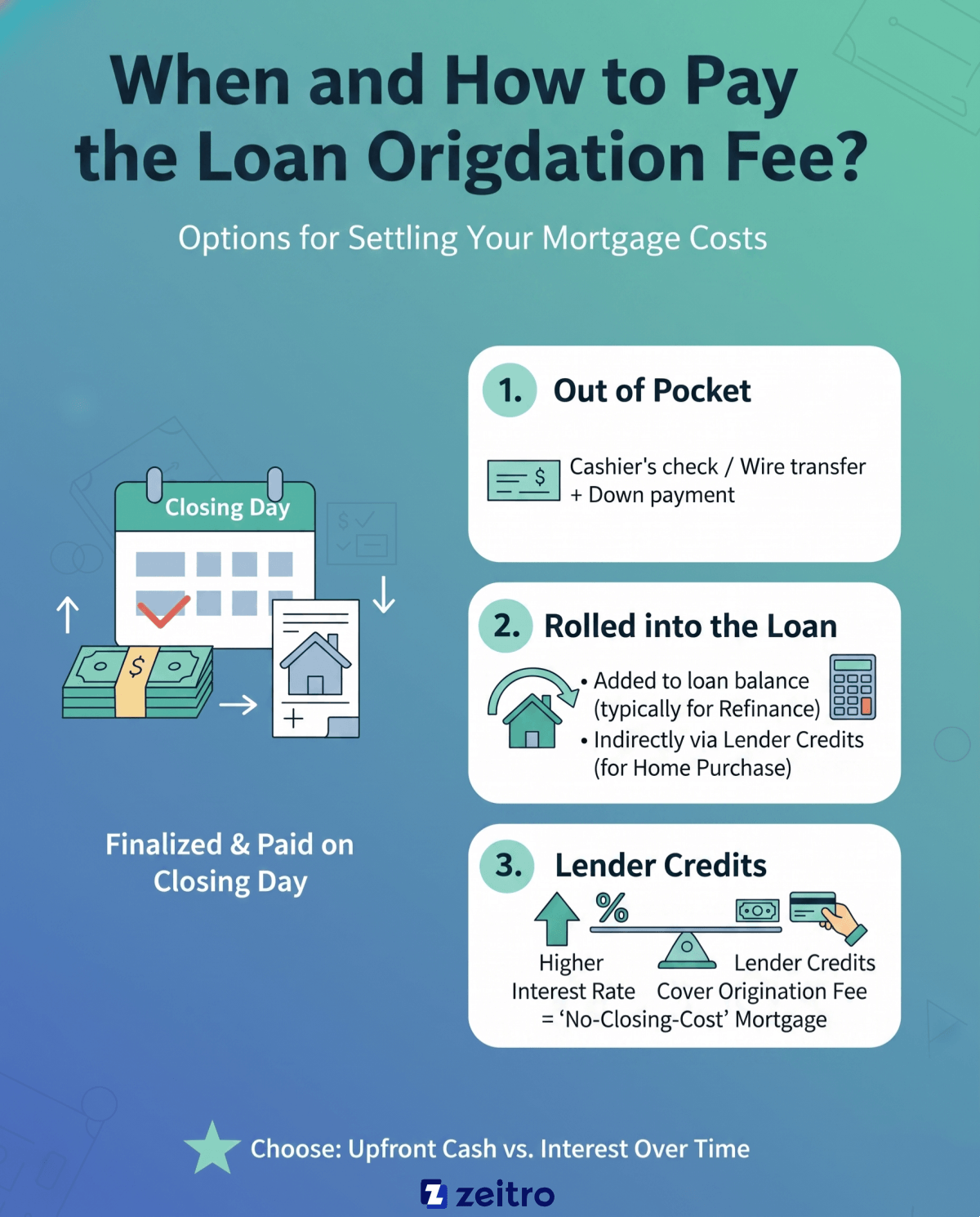

When and How to Pay the Loan Origination Fee?

You won't have to hand over a credit card when you first apply. The origination fee is finalized and paid on your Closing Day as part of your overall closing costs.

When it comes time to settle up, you generally have three options:

Out of pocket: You pay it directly using a cashier's check or wire transfer along with your down payment.

Rolled into the loan: In some cases—more commonly with refinances, or if your loan-to-value ratio allows—you may be able to roll certain costs into the loan balance. For home purchases, this is often achieved indirectly through lender credits tied to a higher interest rate.

Lender Credits: You can accept a slightly higher interest rate. In exchange, the lender gives you credits to cover the origination costs entirely, effectively making it a 'no-closing-cost' mortgage.

Crucial Things to Know About Mortgage Origination Fees

Before you sign anything, there are a few critical nuances I always urge homebuyers to understand to protect their wallets.

First, know exactly where to spot these charges. Lenders are legally required by the Consumer Financial Protection Bureau (CFPB) to clearly itemize this under Section A ("Origination Charges") on Page 2 of your Loan Estimate and Closing Disclosure.

Second, don't confuse origination points with discount points. This is a common trap. Origination points are the lender's mandatory service fees. Discount points, however, are completely optional prepaid interest. You can choose to buy discount points to permanently lower your interest rate, but they shouldn't be hidden as a mandatory origination fee.

Finally, remember the power of negotiation. These fees are not set in stone! The absolute best strategy is to get Loan Estimates from at least three different lenders. If Lender A has great service but high fees, show them Lender B's cheaper paperwork and ask for a price match. Often, they'll drop their origination fee to win your business.

FAQs About Mortgage Loan Origination

Q1. Are loan origination fees tax deductible?

Generally, no. The IRS doesn't allow you to deduct standard service fees like underwriting or processing. However, if your 'origination charges' actually include discount points paid to secure a lower interest rate, those might be deductible as prepaid mortgage interest. Always consult your CPA for specifics.

Q2. Do you get your origination fee back?

No, you don't. Once your loan closes, this fee is non-refundable because the lender has already performed the work. Even if you refinance the house or pay off your mortgage entirely just six months later, that initial service charge will not be returned to you.

Q3. Can a loan origination fee be waived?

Yes, practically speaking. You can negotiate a 'no-closing-cost' mortgage where the lender waives or covers the origination fee. However, they aren't working for free. To compensate for dropping the upfront fee, the lender will simply charge you a higher monthly interest rate.

Q4. Why is my origination fee so high?

It could be high for a few reasons. If you have a small loan balance, lenders often charge a flat minimum fee. Alternatively, a low credit score might increase underwriting complexity, or your lender may have bundled optional discount points into the total origination charge.

Q5. How to negotiate the origination fee?

The secret is to shop around. Get official Loan Estimates from at least three different banks, credit unions, or brokers. Take the estimate with the lowest origination fee and present it to your preferred lender, asking them to match or beat their competitor's pricing.

Q6. How to finance a loan origination fee?

You can roll the fee into your loan balance so you don't pay cash upfront. However, this only works if your home's loan-to-value (LTV) ratio allows for the slightly larger loan size. Keep in mind, financing the fee means you'll pay interest on it for years.

Final Thoughts

Getting fixated on finding the lowest possible origination fee is a common rookie mistake. While saving money upfront feels great, a lender offering zero fees might be masking a terrible interest rate.

When comparing your mortgage options, my best advice is to focus heavily on the APR (Annual Percentage Rate). The APR gives you the honest, big-picture cost of borrowing because it blends both your interest rate and those upfront origination costs into one single number. Do your homework, gather multiple quotes, and don't be afraid to negotiate. You have more power in this transaction than you think.

Find the best mortgage loan processor training for beginners in 2026. Compare top free and paid courses, master core skills, and launch your career today.

When I first transitioned into mortgage processing, the avalanche of industry acronyms, federal regulations, and complex tax return calculations completely overwhelmed me. I remember scouring Reddit threads where absolute newbies shared my exact anxiety. Shadowing senior staff who effortlessly handled credit lines was helpful, but watching someone else work rarely translates into muscle memory.

To truly bridge the gap between theoretical knowledge and real-world loan files, you need structured training. A systematic approach will help you overcome the steep learning curve and rapidly sharpen your professional skills so you can confidently clear conditions.

Key Takeaways

Master the Core Fundamentals: Your daily grind requires expertise in auditing URLA 1003s, crunching income data, and satisfying TRID compliance.

Choose the Right Educational Path: Pathways range from budget-friendly YouTube crash courses to prestigious, paid certifications from the MBA or NAMP.

Embrace Mortgage Tech: Modern processors rely heavily on AI tools like Zeitro to automate guideline searches and streamline workflows, saving countless hours on file stacking.

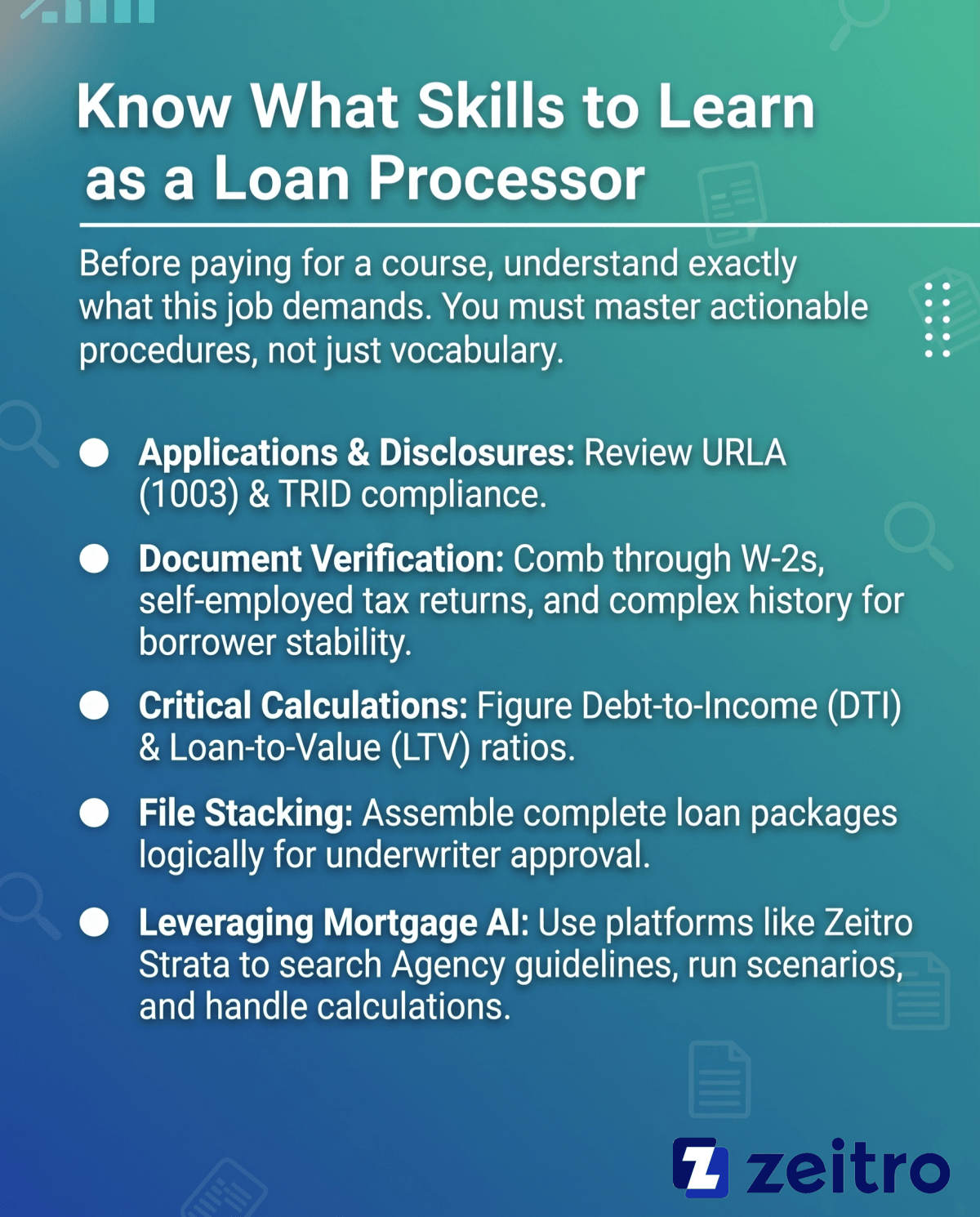

Know What Skills to Learn as a Loan Processor

Before paying for a course, understand exactly what this job demands. You must master actionable procedures, not just vocabulary.

Applications & Disclosures: You will meticulously review the initial URLA (1003) and guarantee strict alignment with federal mandates like TRID.

Document Verification: Expect to comb through W-2s, self-employed tax returns, and complex employment histories to prove borrower stability.

File Stacking: Assemble the complete loan package logically so the underwriter can approve it without kicking it back.

Leveraging Mortgage AI: I highly recommend using platforms like Zeitro Strata. It instantly searches all Agency guidelines (Fannie Mae, FHA, VA), runs loan scenarios, and handles income calculations, keeping newbies from drowning in massive PDF manuals.

The market offers a massive variety of educational resources. Which route you take ultimately depends on your current budget, existing industry experience, and whether you need an employer-recognized certificate to land your very first job. Let's break down the top options.

YouTube (Free)

If you are an absolute beginner with zero budget, this should be your very first stop. When I initially dipped my toes into the industry, YouTube was my saving grace for deciphering the endless sea of mortgage lingo. I suggest typing highly specific phrases into the search bar, such as "how to complete a 1003" or "mortgage processing 101." Many veteran originators and brokers post incredible, screen-share walkthroughs of their daily pipeline management.

However, you must stay vigilant regarding upload dates. Mortgage regulations, agency guidelines, and standardized forms evolve constantly. A video published back in 2019 might feature outdated TRID disclosure timelines or obsolete versions of the URLA. Always filter your search results for content posted within the last twelve to eighteen months to guarantee you are studying the most current lending environment.

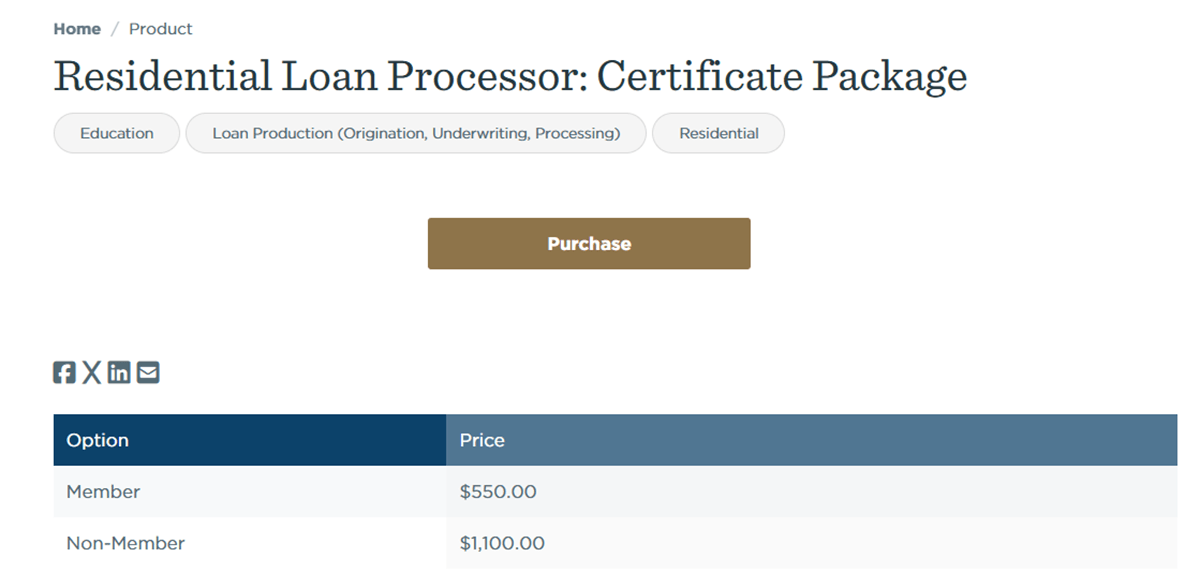

Mortgage Bankers Association (MBA)

When you are ready to invest in a gold-standard credential, the MBA's "Residential Loan Processor Certificate Package" is widely recognized in the industry, particularly among larger lenders and banking institutions. Pricing is typically around $550 for MBA members and about $1,100 for non-members, though this may change over time.

The program generally includes multiple self-paced modules totaling around 30 hours of study. You will dive deep into foundational origination procedures, property appraisal evaluations, fraud detection techniques, and heavy regulatory compliance. I particularly like how this curriculum bridges the gap between basic data entry and actual risk mitigation. If you are aiming for a corporate role at a major retail lender or traditional bank where formal educational backing dictates your starting salary, securing this specific certificate will give you a massive competitive advantage.

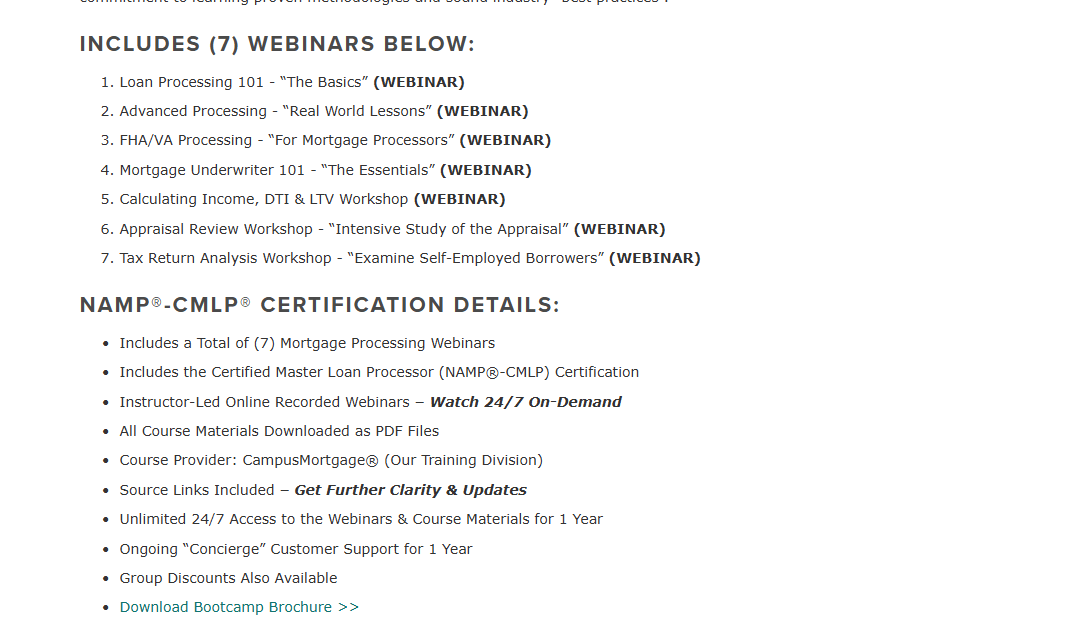

National Association of Mortgage Processors® (NAMP®)

For those who want training hyper-focused solely on the processing niche, NAMP is a well-recognized organization within the mortgage processing niche. Their flagship offering, "The Official NAMP® Processor Boot Camp™," typically runs about $995.

What makes NAMP stand out is their intensely practical, 100% online curriculum. You are not just reading dry compliance text. You learn actionable strategies for FHA/VA file handling and complex tax return analysis. Completing their programs can help you work toward earning the NAMP-CMLP designation, which may require additional experience or qualifications.

I always recommend this specific pathway to anyone looking to make processing a long-term, lucrative career rather than just a stepping stone to underwriting. It proves to prospective wholesale lenders and brokerages that you possess serious, specialized expertise in moving complex borrower files straight to the closing table.

ICE Mortgage Technology (formerly Ellie Mae)

Since Encompass is one of the most widely used loan origination systems in the lending market, learning its specific ecosystem is incredibly strategic. ICE Mortgage Technology offers a phenomenal, quick-hit course typically priced around $63 in 45 minutes.

Usually takeing under an hour to complete, this self-study module won't make you an expert overnight, but it flawlessly illustrates how the processing role physically functions within their proprietary software. The curriculum heavily emphasizes utilizing the Uniform Residential Loan Application (URLA) directly within the LOS. If you recently landed a job at a company running on Encompass, or you know your target employers utilize it, taking this specific training is a no-brainer. It allows you to skip the clumsy software-fumbling phase and immediately start navigating digital files, ordering third-party services, and communicating with underwriters efficiently.

Bank Training Center

If you plan to work inside a traditional depository bank rather than an independent broker shop, the Bank Training Center (partnered with CampusMortgage) is your best bet. Their foundational module, "Loan Processing 101 - The Basics," costs $395, while their comprehensive Boot Camp sits at $995.

I appreciate this platform because it heavily targets the strict banker environment. Beyond teaching you standard DTI and LTV calculations, their curriculum dives deep into the rigid compliance standards unique to banking institutions, such as TRID, HMDA, BSA/AML, and UDAAP regulations. The instructors focus on fixing bad habits and teaching proper file structuring from day one. If your career goal involves handling portfolios for a credit union or a large retail banking entity, this training directly aligns with the rigorous internal audit standards you will face daily.

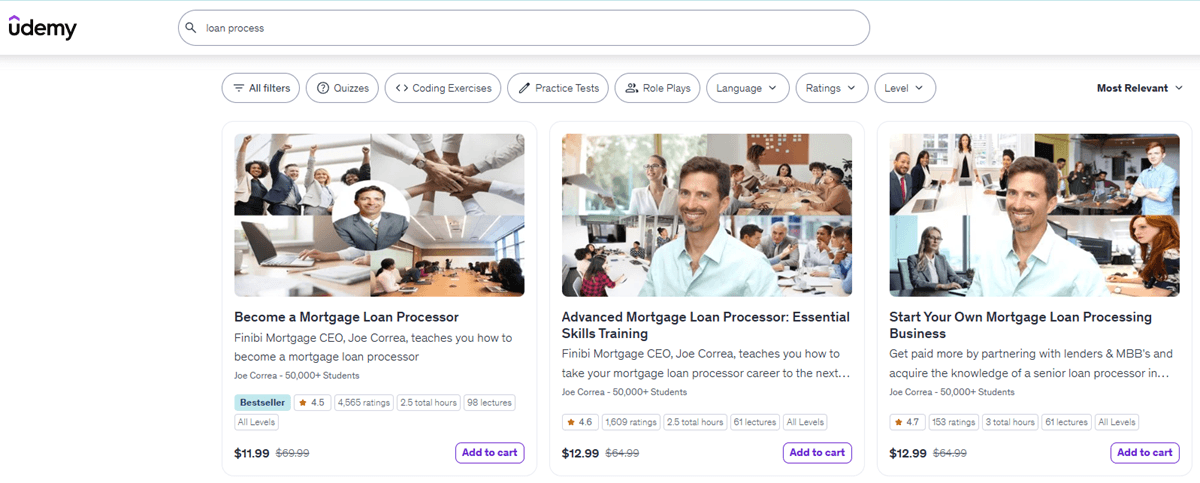

Udemy

When you want structured video learning without spending a fortune, Udemy serves as a fantastic, budget-friendly alternative. Depending on their frequent seasonal sales, you can typically grab comprehensive courses covering mortgage terminology or basic underwriting tasks for anywhere between $15 and $150.

Because anyone can upload a course, the quality varies wildly. You might find a hidden gem taught by a 20-year industry veteran, or a poorly recorded slideshow that barely scratches the surface. Before hitting the purchase button, I highly advise aggressively scrutinizing the student reviews. More importantly, check the "Last updated" date stamped on the course page. If the material hasn't been refreshed since 2025, walk away. The lending landscape shifts too rapidly to risk memorizing outdated loan limits, automated underwriting system (AUS) rules, or legacy disclosure timelines.

Considerations Before Starting Mortgage Loan Processor Training

Before committing to a specific program, weigh these crucial factors so you don't waste time or money:

Your Budget: Determine if you should exploit free introductory content first or if you are financially ready to drop $1,000+ on a prestigious industry designation.

Target Career Path: Are you aiming for a retail bank, a wholesale lender, or working as a 1099 independent contractor? Depository banks require vastly different compliance knowledge compared to nimble brokerages.

Company Tech Stack: Find out what software your future employer uses. If they are locked into Encompass, prioritize ICE's official platform training over generic alternatives.

Licensing Requirements: Depending on your state and employment type, you might need an active NMLS license. W-2 employees at direct lenders usually don't need one, while independent contract processors typically do.

FAQs About Mortgage Loan Processor Training

Q1. Do I need a license to be a mortgage loan processor?

Generally, if you work as a W-2 employee directly for a bank or direct lender, you do not need an individual license. However, requirements vary by state. In some cases, independent contract processors may need an NMLS license, especially if they perform loan originator activities

Q2. How long does it take to complete loan processor training?

It entirely depends on the platform's depth. Short software introductions, like those from ICE, take roughly 45 minutes. Conversely, comprehensive certification tracks from the MBA or NAMP demand around 30 hours of rigorous study, which might take several weeks to fully absorb.

Q3. Are paid mortgage loan processor courses worth it?

Yes, absolutely—especially if you leverage MBA or NAMP credentials to negotiate a higher starting salary or secure a promotion. However, if you are a total novice who cannot yet define basic industry acronyms, stick to free resources until you are certain this career fits you.

Q4. What is the best loan origination software (LOS) to learn?

Encompass, developed by ICE Mortgage Technology, remains the undisputed industry heavyweight and is used by many large lenders and financial institutions. Understanding its interface gives you a massive hiring advantage. Other prominent systems worth exploring include Calyx Point and Arive, which are incredibly popular among independent mortgage brokers.

Q5. Is loan processing hard for a beginner?

The initial learning curve is notoriously steep due to the aggressive compliance rules, complex tax return math, and endless acronyms. Yet, by completing structured training and utilizing modern AI tools to interpret guidelines, many people can become comfortable in the role within a few months, though mastery often takes significantly longer depending on deal complexity.

Conclusion

Stepping into the mortgage industry doesn't require emptying your wallet on day one. I always advise newcomers to hold off on spending cash immediately. Start by searching YouTube for walkthroughs on completing the 1003 and basic lingo tutorials. Once you feel confident you actually enjoy the workflow, invest in authoritative credentials from NAMP or the MBA to boost your resume.

Most importantly, succeeding in 2026 means embracing technology. Knowing how to calculate income manually is great, but leveraging AI platforms like Zeitro Strata to cross-reference agency guidelines instantly will separate you from the pack. Master the fundamentals, lean heavily on modern tech tools, and you will quickly transform from a nervous newbie into a top-tier loan processor.

What is mortgage loan origination? Discover how the process works, typical costs (0.5%-1%), and expert tips to negotiate fees and speed up your closing.

We all love the idea of getting the keys to a new place, but dealing with mortgage paperwork? That's a different story. As a homebuyer, mortgage loan origination is one of the earliest and most important steps you'll face. Figuring out how this phase works isn't just about learning bank jargon. It's your secret weapon for avoiding stressful delays and actually saving money on closing costs. Let's break down exactly what you need to know.

Key Takeaways

The bottom line: Mortgage loan origination covers the entire journey your lender takes to create, process, and ultimately fund your home loan.

What you'll pay: Expect to see an origination fee that often runs about 0.5% to 1% of the loan amount, though it can vary depending on the lender and loan structure.

The big difference: Origination is all about gathering and organizing your file, while underwriting is the final "yes or no" decision on your money.

What is Loan Origination for a Mortgage?

I've noticed a lot of first-time buyers think getting a mortgage happens in one shot. You ask for money, and the bank eventually says yes. Actually, it's a much more involved administrative process called loan origination.

Think of it as the timeline starting from the minute you hand in your initial application right up to the day the lender gets your funds ready for closing. Why do lenders put you through the wringer? Mostly, it's about risk. They can't just wire hundreds of thousands of dollars based on a handshake. They use this phase to double-check your identity, dig into your financial health, and make sure that property is actually worth the asking price.

In my experience, if you view origination as building a solid financial relationship with your lender rather than just "filling out forms," the strict rules start to make a lot more sense. It's the foundation of your entire home purchase.

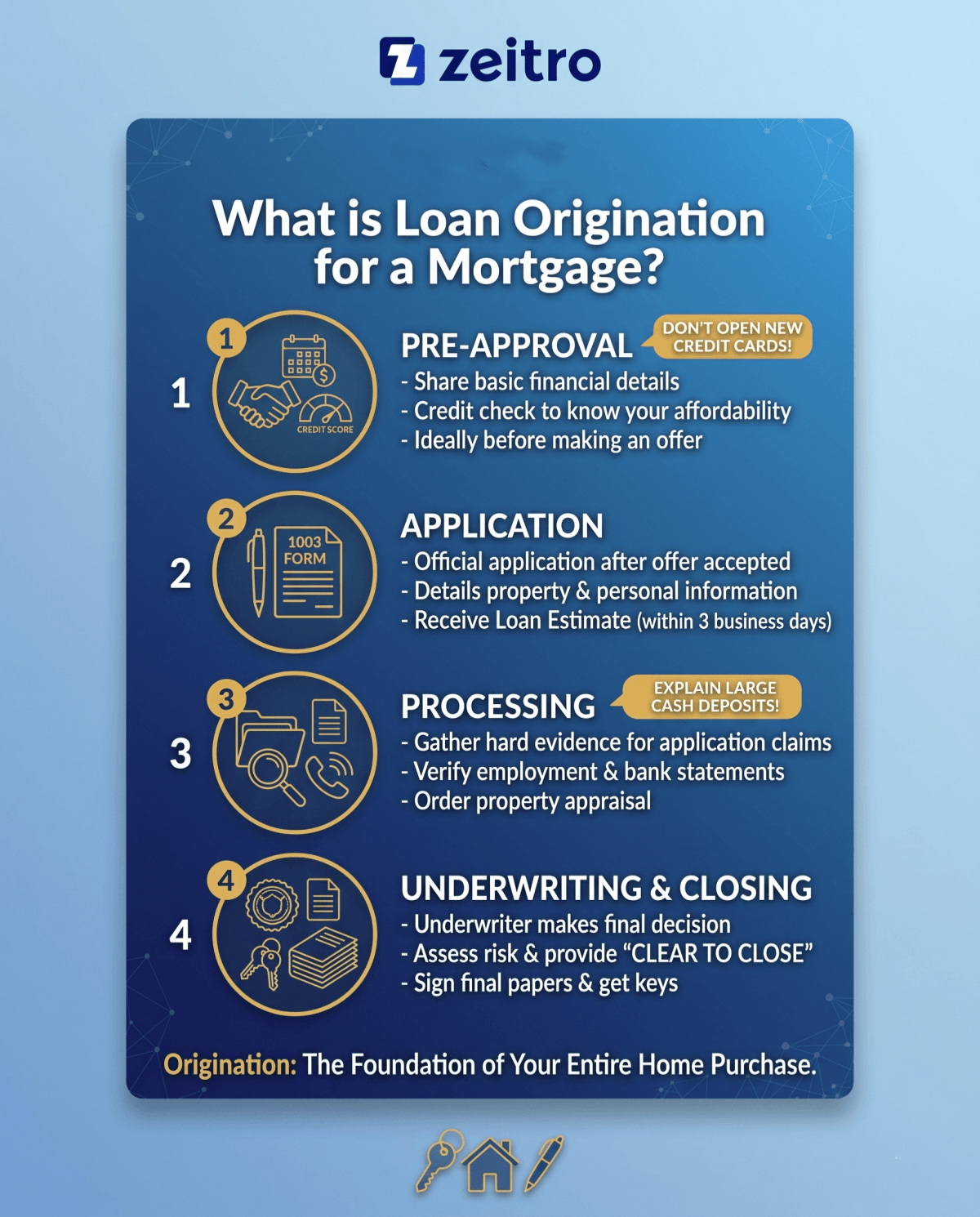

4 Stages of the Loan Origination Process

The whole timeline feels way less intimidating once you chop it into bite-sized pieces. If you know what's coming, you can actually help speed things up.

1. Pre-approval and Pre-qualification

Ideally, you should complete this step before seriously shopping for a home or making an offer. You'll share basic financial details, allowing the lender to run a credit check and tell you how much house you can afford.Please don't open new credit cards or buy a car right now. A sudden credit ding can kill your pre-approval fast.

Found the house and got your offer accepted? Great. Now you officially apply by filling out the Uniform Residential Loan Application (often called the 1003 form).Fill this out honestly, detailing the property and your personal info. In return, the lender is generally required to provide a Loan Estimate within three business days after receiving a complete application, breaking down your expected rate and closing costs.

3. Processing and Verification

This is the grunt-work phase. A loan processor steps in to make sure every claim on your application is backed by hard evidence. They'll order the property appraisal, call your boss to verify employment, and scrutinize your bank statements.Processors hate mystery money. If you have large, unexplained cash deposits in your checking account, prepare to write letters explaining exactly where they came from.

Finally, your thick file lands on the underwriter's desk. They are the ultimate decision-makers. They assess the risk and decide if you're good for the money. If you pass, you get a "Clear to Close," meaning you're ready to sign the final papers and get your keys.

Requirements of Loan Origination

Want a secret to a stress-free mortgage? Have your documents ready before the loan officer even asks. Doing this upfront easily shaves days off your timeline. Here's the standard checklist you'll need to pull together:

Government ID: A current driver's license or US passport.

Proof of Income: Your two most recent W-2s and about a month's worth of recent pay stubs.

Tax Returns: The last two years of your 1040s (super important if you're a freelancer or business owner).

Asset Proof: The past 60 days of bank statements across checking, savings, and retirement accounts. They need to see you actually have the cash for the down payment.

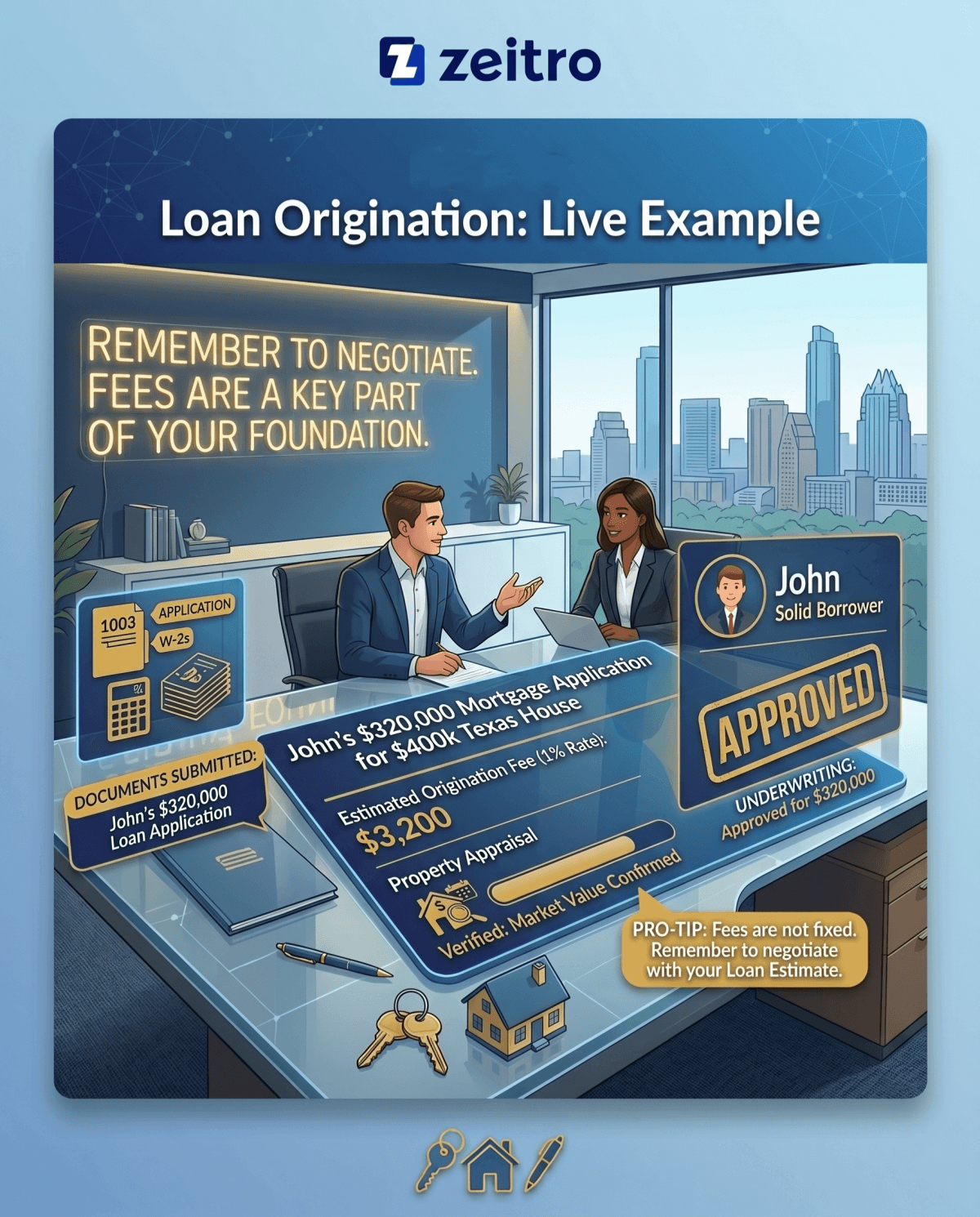

Let's look at how this plays out in real life. Imagine John is buying his first place in Texas for $400,000. He is putting down 20% ($80,000), meaning he needs to borrow $320,000.

John heads to a local lender to kick off the origination process. He hands over his 1003 application, his W-2s, and bank statements. The bank charges him a 1% origination fee on his $320,000 loan amount.

Over the next month, the bank's processor orders an appraisal to verify the house is truly worth that 400k price tag. Once John's financial puzzle is fully assembled, the file goes to the underwriter. They review the risk, confirm John is a solid borrower, and officially approve the $320,000.

How Much Does Loan Origination Cost?

So, what's the damage? In the U.S., a typical loan origination fee usually lands between 0.5% and 1% of your total borrowed amount. Using John's $320,000 mortgage as an example, his fee would run anywhere from $1,600 to $3,200.

You don't have to write a check for this on day one, though. It is typically included as part of your total closing costs, which you may pay upfront or, in some cases, roll into the loan depending on the structure.

These fees aren't always set in stone. I strongly recommend trying to negotiate. Ask your lender to lower the fee, or bring in a competitor's Loan Estimate and ask them to match it.

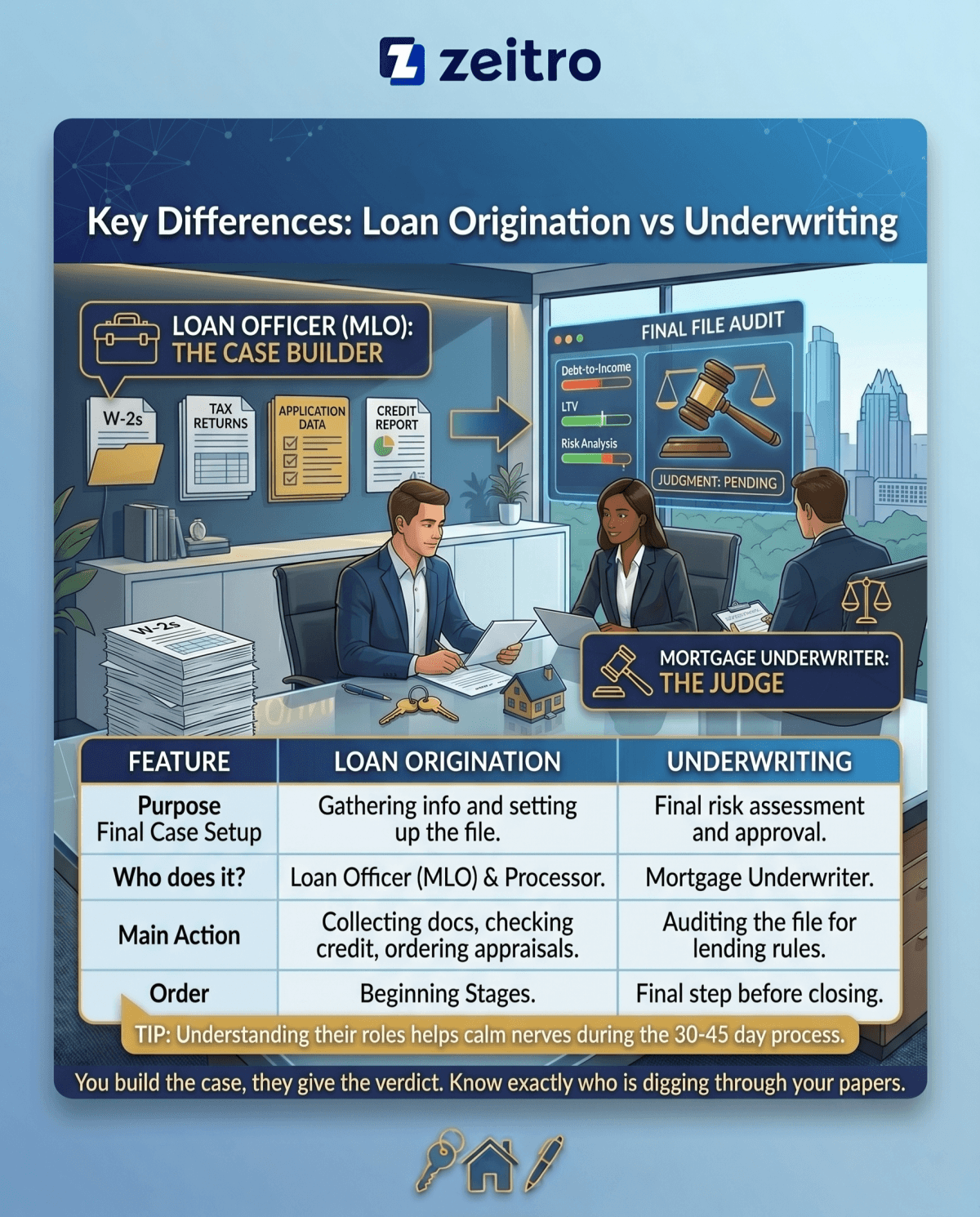

Key Differences: Loan Origination vs Underwriting

People mix these two up all the time since they happen right next to each other. To put it simply: the loan officer helps you build your case, while the underwriter is the judge who hands down the verdict.

Knowing who does what really helps calm the nerves during those 30 to 45 days of waiting. You'll know exactly who is digging through your paperwork.

A mortgage loan originator (MLO) is the professional or company helping you apply for your home loan. Think of them as your main point of contact. They take your application, explain your interest rates, and guide your file through the messy early stages.

Q2. What is a loan origination system?

A loan origination system (LOS) is the backend software banks use to manage your file. This digital platform handles the heavy lifting, from spitting out initial disclosures to securely holding your tax returns and running automated compliance checks.

Q3. Is a loan originator the same as a broker?

No, they aren't the same. A loan originator typically works for a specific lender and offers that lender's products, though some may have access to a wider range of loan options depending on their organization. A mortgage broker, on the other hand, is a middleman who shops your application around to dozens of wholesale lenders to find the best rate.

Q4. Can you negotiate loan origination fees?

Yes, you absolutely can. When you get your Loan Estimate, look closely at the "Origination Charges." You can push back and ask the lender to lower that number, or better yet, use a competing offer from a different bank to force a price match.

Q5. How long does the loan origination process take?

From application to closing table, the whole origination process usually takes often takes around 30 to 45 days, though timelines can vary widely depending on market conditions and borrower responsiveness. Keep in mind, this timeline heavily relies on you. The faster you hand over requested documents, and the smoother the appraisal goes, the quicker you'll get to closing.

Final Word

Getting a mortgage can easily feel like drowning in paperwork, but the origination process is really just the foundational first step of buying a house. Once you understand the mechanics behind the scenes, from that first 1003 application to the underwriter's final stamp of approval, you take back control. Having your files organized early on and pushing back on fees can save you a ton of stress and cash.

Stop losing prospects. Compare the 8 best mortgage lead management software of 2026. Find the top CRMs and AI agents to help loan officers boost conversions.

I've spent years in the mortgage industry, and if there's one thing I've learned, it's that a leaky pipeline kills business. With guidelines shifting and margins tightening in 2026, letting prospects slip through the cracks is not an option.

You need a system that captures, nurtures, and converts efficiently. To help you boost your conversion rates, I've tested and compared the best mortgage lead management software on the market. Let's dive into the top contenders.

Key Takeaways

Automation is non-negotiable: Modern platforms must automate follow-ups to maintain a high speed-to-lead and prevent burnout.

AI integration drives conversion rates: AI-driven tools drastically reduce manual underwriting tasks and expedite pre-qualifications.

LOS compatibility is crucial: Your chosen lead management tool must sync perfectly with your Loan Origination System (LOS) to avoid double data entry.

How We Evaluated the Best Mortgage Lead Management Software

To give you the most accurate recommendations, I evaluated these platforms based on real-world loan officer feedback, LOS integration capabilities, automated follow-up efficiency, and data security. I also looked closely at how effectively each tool leverages new technology to solve actual origination bottlenecks.

Take a Quick Comparison Here

Deciding on the right platform can feel overwhelming, so I always recommend starting with a high-level view before getting lost in the technical weeds. The table below compares the 8 leading tools side-by-side, summarizing their core strengths, potential drawbacks, and baseline costs.

I've structured this comparison specifically to help loan officers, account executives, and wholesale brokers make a rapid preliminary decision within minutes rather than hours. Keep in mind that the "Starting Price" reflects base-level tiers or publicly available data. For many of these systems, custom enterprise rollouts or adding advanced features, like predictive dialers or deep AI modules, will affect your final quote. Let's see how they stack up.

8 Best Mortgage Lead Management Systems in 2026

Now, let's break down exactly what makes each of these systems stand out. From robust enterprise CRMs to specialized AI agents, here is my detailed breakdown of the tools that will redefine your workflow this year.

#1 Surefire CRM - Best for Overall Mortgage Marketing Automation

Verdict: The most comprehensive marketing automation CRM for loan officers who want extensive content ready to go.

Pricing: Custom pricing

Built specifically for the mortgage industry, Surefire CRM by ICE Mortgage Technology remains an absolute powerhouse in 2026. If you dread drafting emails or creating flyers, this is your holy grail. It shines in lead management by offering an unparalleled content library that automatically nurtures borrowers long after closing.

Unlike generic CRMs, its deep industry focus means it seamlessly connects with major LOS platforms like Encompass, ensuring your pipeline data flows flawlessly without repetitive manual entry.

Features:

Client for Life Workflows: Automated multi-year drip campaigns to guarantee repeat business.

Deep LOS Integration: Real-time, two-way sync with top origination systems.

Dynamic Video Integration: Send personalized video messages natively to build instant trust.

Automated Rate Alerts: Triggers communications when prospects are financially ready to act.

#2 Zeitro - Best for AI-Driven Lead Qualification & Non-QM Efficiency

Verdict: A game-changing AI agent that drastically accelerates pre-qualifications and instantly decodes complex Non-QM guidelines.

Pricing: Custom pricing

Zeitro isn't just a CRM. It's a purpose-built AI Agent for mortgage professionals. I was blown away by how it tackles lead management. Instead of just organizing contacts, it acts as a lead-generating and conversion machine.

Through its GrowthHub, loan officers launch branded microsites featuring live rates, which powerfully boosts local SEO to attract inbound leads. Once captured, the Digital 1003 (POS) takes over, allowing borrowers to pre-qualify in just 5 minutes while the AI instantly computes accurate DTI ratios. It actively saves Account Executives over 18 hours monthly.

Features:

GrowthHub Personal Sites: Attract organic traffic via personalized, branded rate quote pages.

Digital 1003 POS: Automated borrower application system exporting to MISMO 3.4–compatible formats used by Fannie Mae and other industry systems

Live Pricing Engine: Generate highly competitive conventional and Non-QM quotes instantly.

High Conversion Rates: Increases closing rates by 30% and closes loans 20% faster.

#3 Jungo - Best for Salesforce-Based Mortgage Operations

Verdict: The ultimate mortgage ecosystem for teams that want the immense customizability and power of Salesforce.

Pricing: Starting at $96/user/month (annual contract)

For teams already comfortable with the Salesforce ecosystem, Jungo is a no-brainer. It takes the world's leading CRM infrastructure and tailors it specifically for mortgage professionals. In my experience, its true advantage in lead management lies in its seamless LOS sync capabilities.

As loans progress through various stages in your LOS, Jungo automatically updates lead statuses and triggers appropriate milestone emails to borrowers and realtors. It bridges the gap between sales and operations beautifully.

Features:

Salesforce Infrastructure: Enterprise-level security and endless third-party integration possibilities.

Automated Milestone Alerts: Keeps all parties updated seamlessly during the origination process.

Reffinity Partner Tracking: Specialized tools to manage and grade realtor referral relationships.

Co-Branded Marketing: Easily generate flyers and emails alongside your referral partners.

Centralized Lead Routing: Pulls leads automatically from Zillow, LendingTree, and other sources.

#4 Shape - Best for Built-in Communication & Auto-Dialer

Verdict: A communication-heavy platform perfect for teams relying on aggressive outbound calling and immediate text responses.

Pricing: Custom pricing

If your strategy revolves around speed-to-lead, Shape is a fantastic option. Rather than piecing together a CRM, a dialer, and a texting platform, Shape gives you everything under one roof. I love how it handles initial lead capture.

The moment an inquiry comes in, the system's automated workflows can text, email, and queue a call simultaneously. It is explicitly built for high-volume outreach, making it a great fit for loan officers who spend their days actively prospecting.

Features:

Integrated Cloud Dialer: Built-in calling capabilities without needing a third-party add-on.

Omnichannel Workflows: Trigger emails, SMS, and ringless voicemails automatically.

Custom Lead Prioritization: Smart views ensure you always call your hottest prospects first.

Partner Integrations: Connects easily with thousands of apps via webhooks and Zapier.

#5 Follow Up Boss - Best for Real Estate & Mortgage Team Alignment

Verdict: The gold standard for lightning-fast lead routing, keeping real estate agents and LOs perfectly aligned.

Pricing: Starting at $58/user/month

While often associated heavily with real estate agents, Follow Up Boss is incredibly popular in the mortgage sector, especially for LOs who work tight pipelines alongside Realtor partners. Its philosophy is simple: zero leads left behind. I've found its lead routing to be incredibly fast.

A new prospect can be distributed to an available team member instantly based on custom rules. If you run a joint marketing venture with real estate teams, this platform ensures absolutely frictionless handoffs.

Features:

Instant Lead Routing: Distribute prospects based on zip code, price point, or round-robin rules.

Smart Lists: Automatically surface the specific contacts you need to call today.

Action Plans: Pre-built, customizable follow-up sequences to nurture cold leads.

Two-Way Email & Texting: Centralized communication inbox visible to the whole team.

Deep Realtor Synergy: Easily share notes and lead statuses with referring partner agents.

#6 HubSpot CRM - Best for Scalability & Inbound Lead Generation

Verdict: A highly adaptable powerhouse for large brokerages focused heavily on content marketing and inbound lead capture.

Pricing: Free base version, paid plans start from $7/month

HubSpot isn't natively a mortgage software, but its sheer power makes it impossible to ignore. I recommend it for larger organizations that generate their own leads through blogs, social media, and landing pages. Its inbound marketing tools are practically unmatched.

While you will need to spend time customizing pipelines to match mortgage stages, the scalability is fantastic. You can capture a lead via a website form, automatically score their engagement, and route them to an LO without lifting a finger.

Features:

Advanced Lead Scoring: Prioritize prospects based on their direct interactions with your website.

Powerful Form Builder: Capture borrower information effortlessly across digital channels.

Visual Sales Pipeline: Drag-and-drop interfaces to track where every single loan sits.

Extensive App Marketplace: Integrates with practically any other tool in your tech stack.

Unmatched Analytics: Deep insights into which marketing channels actually produce closed loans.

#7 RevSystems - Best for Enterprise-Level Custom Workflows

Verdict: A sophisticated engine for massive lending institutions requiring highly complex, automated approval sequences.

Pricing: Custom pricing

When standard out-of-the-box CRMs simply aren't enough for a large lending institution, RevSystems steps up. From my perspective, this platform excels at complex workflow orchestration. Large organizations often have intricate lead distribution rules, compliance checkpoints, and specialized underwriting handoffs.

RevSystems allows enterprise IT teams to build highly customized automated approval paths and sophisticated lead scoring models. It handles high-volume lead traffic effortlessly, ensuring that massive teams maintain a standardized, compliant process across every single branch.

Features:

Enterprise Automation: Build complex, multi-branch workflow rules from the ground up.

Dynamic Lead Scoring: Evaluate prospect viability using entirely customizable data points.

Robust Compliance Framework: Designed to meet strict mortgage industry security standards.

Advanced Data Aggregation: Pull leads securely from multiple massive aggregators simultaneously.

Custom Reporting: Deep granular visibility into your institutional lending metrics.

#8 Rise CRM - Best for Boutique Mortgage Brokerages

Verdict: A lightweight, highly intuitive option perfect for smaller teams prioritizing ease of use and value.

Pricing: Custom pricing

Not every team needs a bloated enterprise system, and that is exactly where Rise CRM fits into the picture. If you operate a boutique brokerage and just want a clean, simple interface to stop leads from falling through the cracks, this is a solid choice.

I appreciate how quickly a new loan officer can learn this system. It focuses purely on the essentials: organizing contacts, setting up basic follow-ups, and managing tasks, offering high performance without the steep learning curve.

Contact Segmentation: Easily group leads by loan type, timeline, or referral source.

Email Integration: Track correspondence seamlessly right within the client profile.

Cost-Effective Scalability: Affordable infrastructure tailored specifically for growing boutique teams.

Features to Consider When Choosing a Pick

Choosing the right lead management software is a serious commitment. Based on my industry experience, prioritizing the right capabilities over flashy add-ons will save you countless headaches. Here is what you must look for:

LOS Integration: This is critical. The platform must sync seamlessly with systems like Encompass or Calyx to ensure data flows flawlessly backward and forward.

AI & Automation Capabilities: Can the tool automatically calculate DTI or pull Non-QM guidelines? Advanced AI tools drastically speed up initial workflows.

Compliance & Security: The mortgage industry handles highly sensitive financial data. Ensure the software strictly adheres to state and federal data protection regulations.

Pipeline Visibility: You need visual clarity to instantly see exactly which stage of the loan process every prospect currently occupies.

Speed-to-Lead Customization: Fast, intelligent lead routing rules will drastically improve your chances of reaching a borrower before a competitor does.

FAQs About Mortgage Lead Management Software

Q1. What is the difference between a mortgage CRM and a lead management system?

A Mortgage CRM focuses heavily on long-term relationship building and retaining past clients. A lead management system, however, specifically targets the top of the funnel. It handles capturing inbound inquiries, routing them to the right loan officers instantly, and managing the initial pre-qualification stages.

Q2. How does AI improve mortgage lead management?

AI completely transforms efficiency. It can automatically extract data to compute accurate DTI ratios, instantly parse complex underwriting guidelines, and offer real-time competitive quotes. This means loan professionals can pre-qualify prospects several times faster, turning cold inquiries into active applications rapidly.

Q3. Do these systems integrate with my existing Loan Origination System (LOS)?

Yes, most top-tier platforms integrate directly with major LOS providers via native connections or open APIs. Look for systems that allow you to seamlessly export borrower data in the standard FNM 3.4 format to avoid duplicate data entry and manual errors.

Q4. How much does mortgage lead management software cost?

Pricing varies widely based on your team size and feature requirements. Basic plans can start around $8 to $69 per user monthly. However, robust platforms featuring integrated dialers or advanced AI capabilities typically range from $119 to several hundred dollars monthly.

Q5. Is lead management software compliant with mortgage industry regulations?

Reputable platforms are designed to support compliance with regulations such as RESPA and TCPA, but full compliance ultimately depends on how your team uses the system.

Conclusion

Finding the best mortgage lead management software ultimately comes down to your specific operational style. If your main goal is deploying massive, automated marketing campaigns, you can't go wrong with Surefire CRM.

However, if you want to leverage cutting-edge technology to actively close 30% more loans while drastically reducing manual guideline lookup, Zeitro is unequivocally the most forward-thinking choice for 2026. Its AI-powered Digital 1003 and GrowthHub features convert leads far faster than any traditional CRM I've tested.

Don't let valuable prospects fade away because your current tech stack is lagging. I strongly encourage you to evaluate your team's biggest bottlenecks, compare features closely, and request personalized demos from these top providers. Upgrading your system today will secure your pipeline for years to come.

Is a fixed-rate mortgage right for you? A loan officer breaks down the pros, cons, types, and compares 15-year vs 30-year terms to help you choose wisely.

I've seen countless clients sit across my desk, totally overwhelmed by loan options. I completely get it. If there's one thing most homebuyers crave, it's peace of mind, and that's exactly what a fixed-rate mortgage delivers.

As a loan officer, I often recommend this straightforward product because it locks in your interest rate, giving you a high level of financial predictability for decades. In this guide, I'll break down exactly what a fixed-rate mortgage is, its pros and cons, and answer the most common questions I hear from borrowers every day.

Key Takeaways

Total Predictability: Your interest rate and principal-and-interest payment stay exactly the same for the entire life of the loan.

Best for Long-Term Buyers: It is often a good choice if you plan to stay in your home long enough to benefit from long-term stability, commonly estimated at around 5–10 years, depending on market conditions.

ARMs vs. Fixed: Unlike Adjustable-Rate Mortgages (ARMs), you are protected from future interest rate hikes.

Budgeting Made Easy: Knowing your core housing cost never changes makes long-term financial planning much simpler.

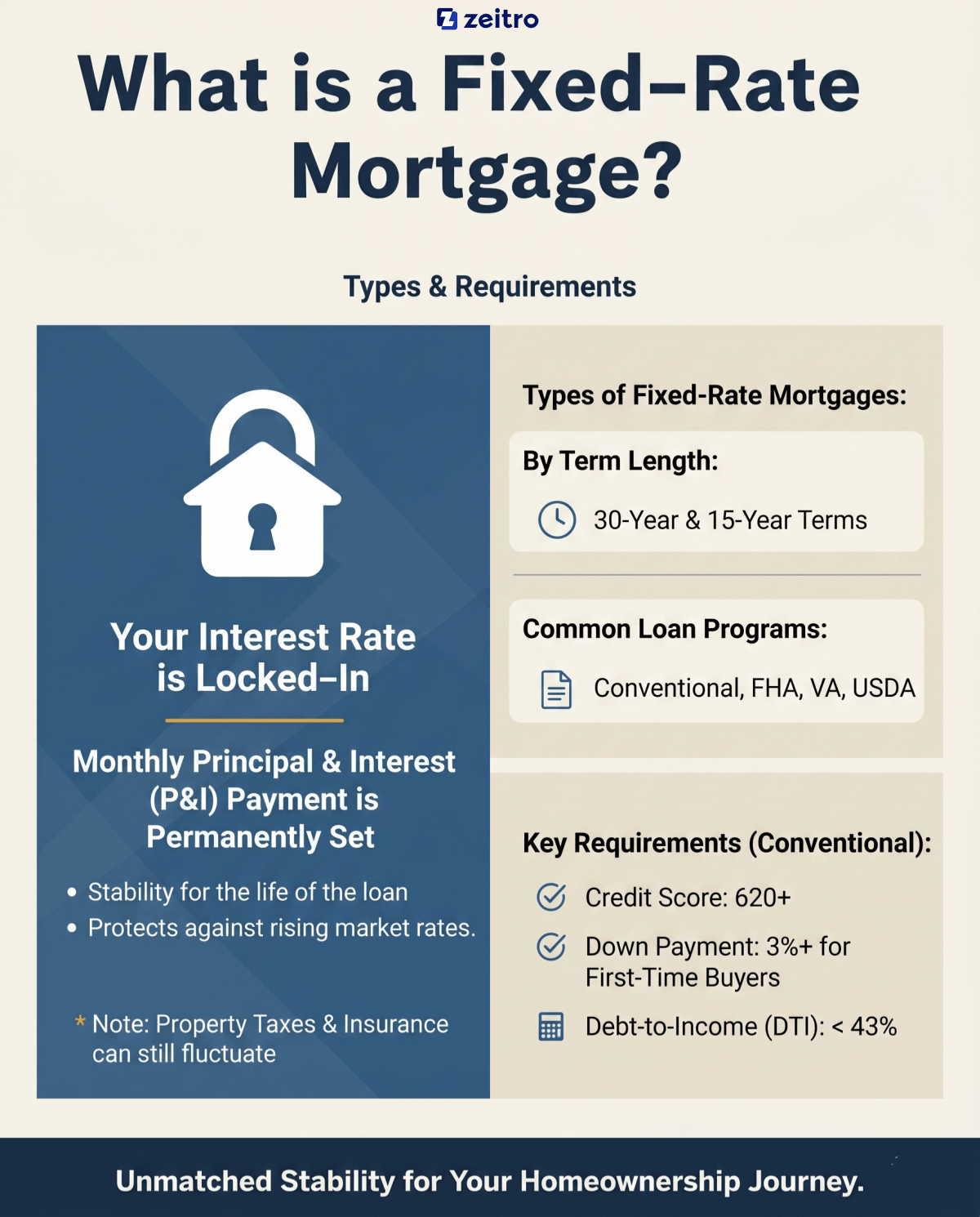

What is a Fixed-Rate Mortgage?

A fixed-rate mortgage is exactly what it sounds like: a home loan where your interest rate remains locked from the day you close until the day you pay it off.

Whether the broader economy crashes or market rates skyrocket to 10%, your rate won't budge. This fixed interest rate means your monthly principal and interest payment is permanently set. When I explain this to first-time buyers, I can literally see their shoulders drop with relief.

However, it's crucial to understand that while the lender guarantees your P&I won't change, your total monthly housing expense might still fluctuate. Why? Because property taxes and homeowners insurance, which are typically rolled into your monthly payment, can and often do increase over time. Still, locking in the core cost of your home for the life of the loan provides unmatched stability.

Types of Fixed-Rate Mortgages

Fixed-rate mortgages aren't one-size-fits-all. They come in several different shapes and sizes to fit your specific financial goals.

By Term Length: The most popular options are 30-year and 15-year terms, though 10-year and 20-year options exist. The 30-year gives you the lowest monthly payment, while the 15-year saves you a ton on interest.

Conventional Loans: The standard mortgage not backed by the government. It's the most common choice I see.

FHA Loans: Government-backed loans perfect for buyers with lower credit scores.

VA Loans: Exclusive, zero-down-payment loans for veterans and active military.

The 30-year conventional fixed-rate mortgage is by far the crowd favorite, but we can always tailor the type to your unique situation.

Requirements of Fixed-Rate Mortgages

Every loan program has its own rulebook, but generally, to get approved for a fixed-rate mortgage in today's US market, you'll need to meet these baselines:

Credit Score: For a conventional loan, you'll need a minimum score of 620. However, to snag the best interest rates, I always advise my clients to aim for 740 or higher. (FHA loans can sometimes accept scores down to 500-580).

Down Payment: Gone are the days of needing 20% down! First-time buyers can often qualify with just 3% down on conventional loans, or 3.5% for FHA.

These are general guidelines. Your specific requirements will depend on the lender and loan type.

How Does a Fixed-Rate Mortgage Work?

Understanding how your payments work behind the scenes is crucial. Here is how your fixed-rate loan actually operates over time:

The Amortization Schedule: This is a banking term for how your loan is paid off. Your fixed monthly payment is split between paying down the principal (the loan balance) and the interest (the lender's fee).

Early Years: In the beginning, the vast majority of your monthly payment goes toward interest. Only a small fraction chips away at the principal.

Later Years: As the years roll on, the balance shifts. You start paying much more toward the principal and less toward interest.

Consistent Total: Even though the ratio of principal to interest changes every single month, your total P&I payment remains exactly the same.

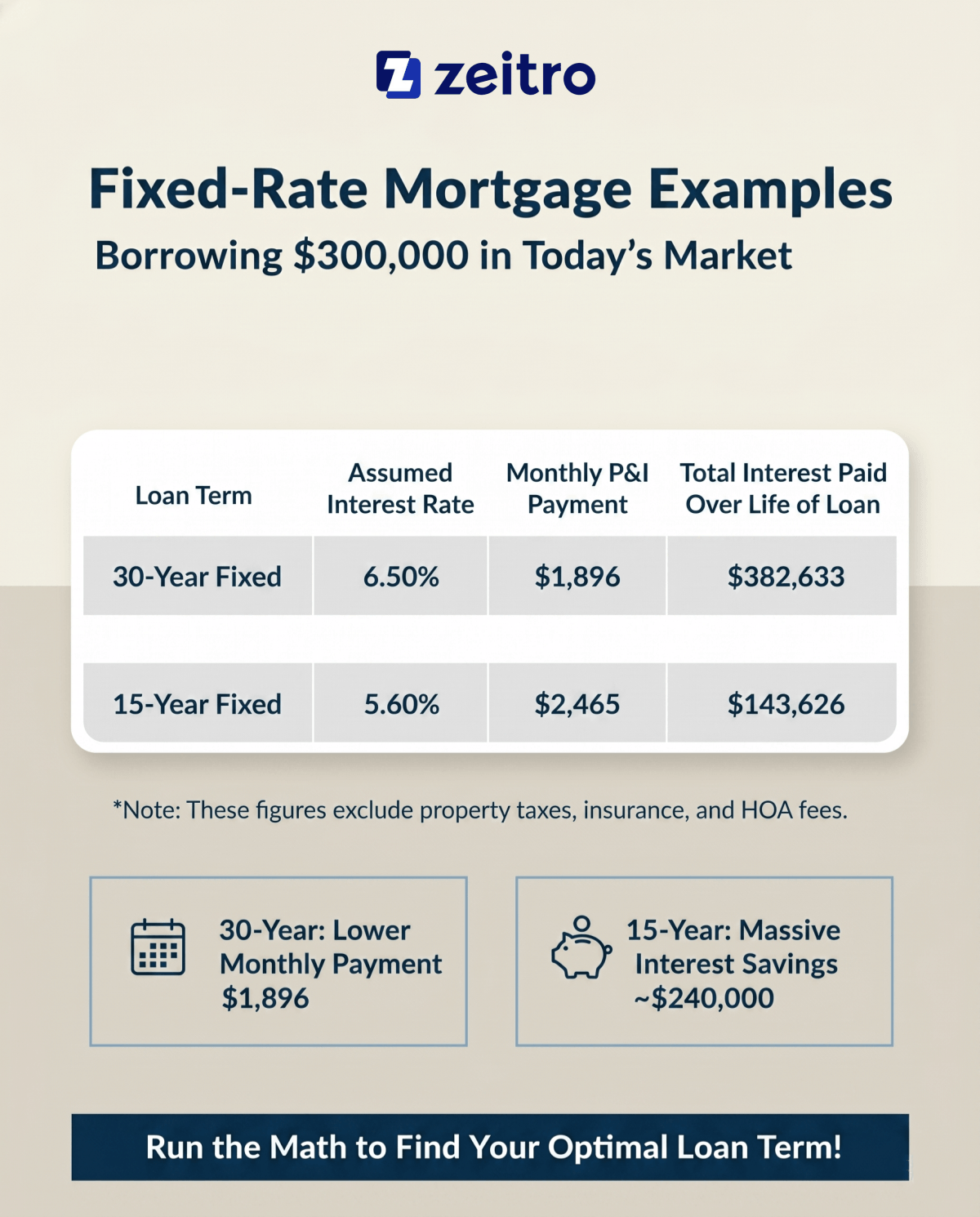

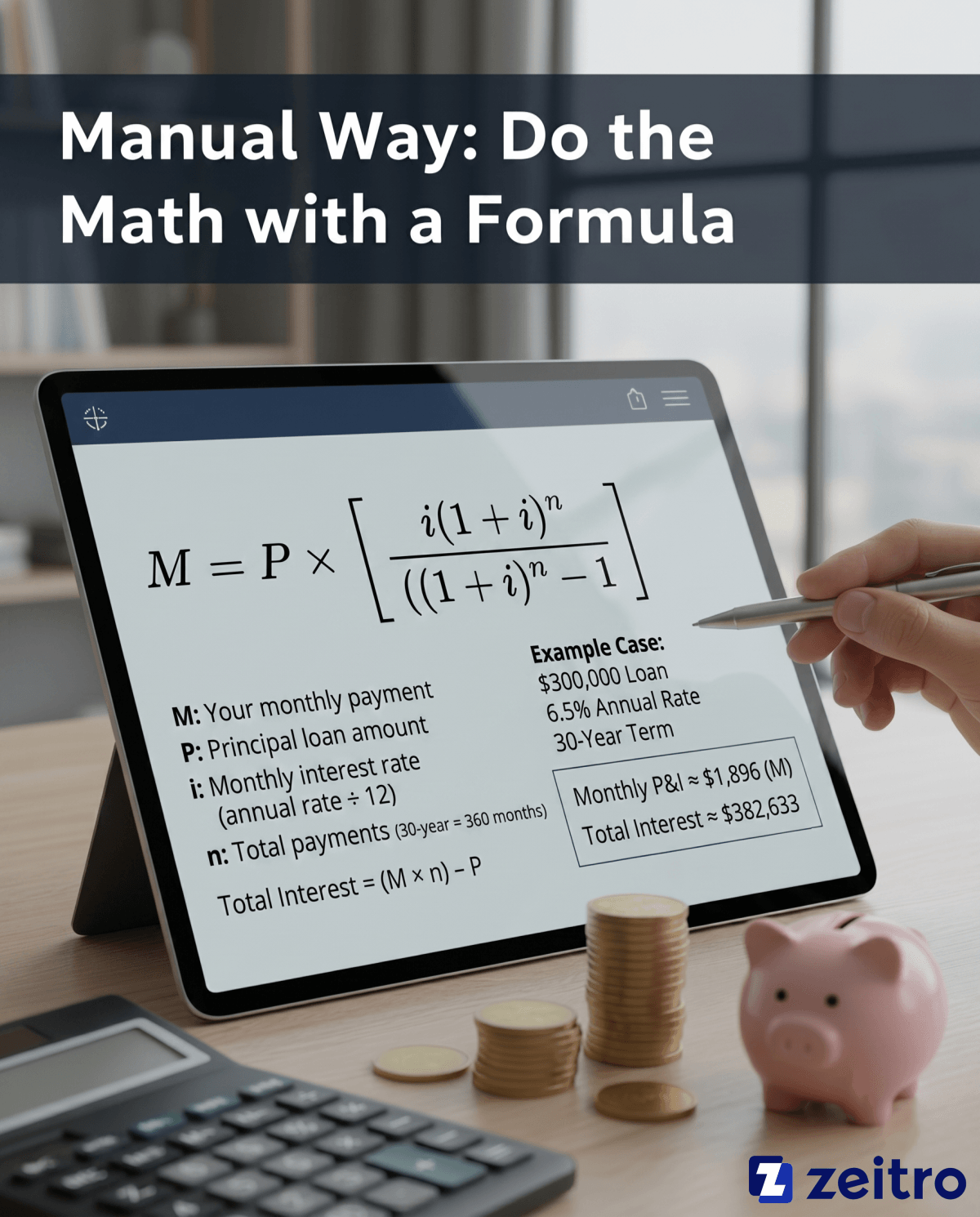

Fixed-Rate Mortgage Examples

To give you a real-world perspective, let's look at a typical scenario I might run for a client right now. Let's assume you are borrowing $300,000 to buy a home in the current market.

Here is how the numbers shake out depending on the term you choose, using hypothetical interest rates for illustration purposes:

Note: These figures exclude property taxes, insurance, and HOA fees.

As you can see, the 30-year gives you a much more manageable monthly payment of $1,896. However, the 15-year option, despite costing roughly $569 more per month, saves you nearly $240,000 in total interest! This is why running the math is so critical.

No mortgage is perfect. As a loan officer, I believe in absolute transparency. Here is the balanced truth about fixed-rate loans:

Pros:

Budget Predictability: You'll never lose sleep over rising interest rates. Your principal and interest payments are shielded from inflation, though other housing costs may still rise.

Simple to Understand: There are no confusing adjustment periods or index margins to track.

Long-Term Security: It's the safest vehicle for building equity over decades without payment shocks.

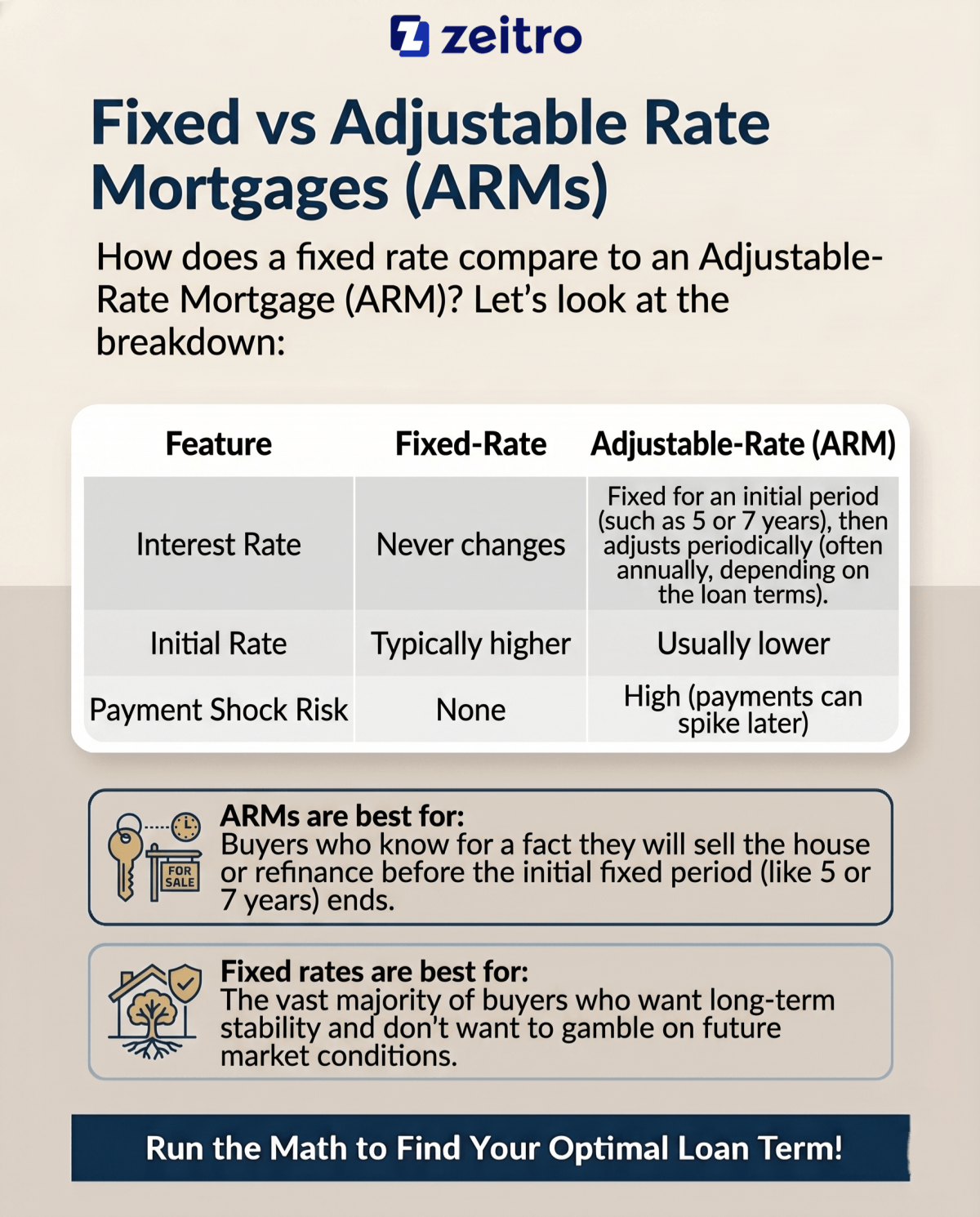

Cons:

Higher Initial Rates: Fixed rates typically start out slightly higher than the initial introductory rates offered on ARMs.

Refinancing Costs: If market rates drop significantly, your rate won't automatically adjust down. You have to actively refinance, which involves paying closing costs again.

Stricter Qualification: Because the rate is higher than an ARM's starting rate, it pushes your DTI up, meaning you might qualify for a slightly smaller maximum loan amount.

When to Get a Fixed-Rate Mortgage?

So, when do I actually tell a borrower to pull the trigger on a fixed rate? Usually, it comes down to these three scenarios:

You're Planting Roots: If you plan to live in the home for more than 7 to 10 years, a fixed rate is almost always the winner. You mitigate long-term risk.

You're Risk-Averse: If the thought of your mortgage payment randomly increasing by $400 a month in the future makes your stomach drop, secure a fixed rate. "Sleep equity" is real.

Rates are Historically Favorable: When the overall market dips, locking in a low fixed rate for three decades is one of the smartest financial moves you can make.

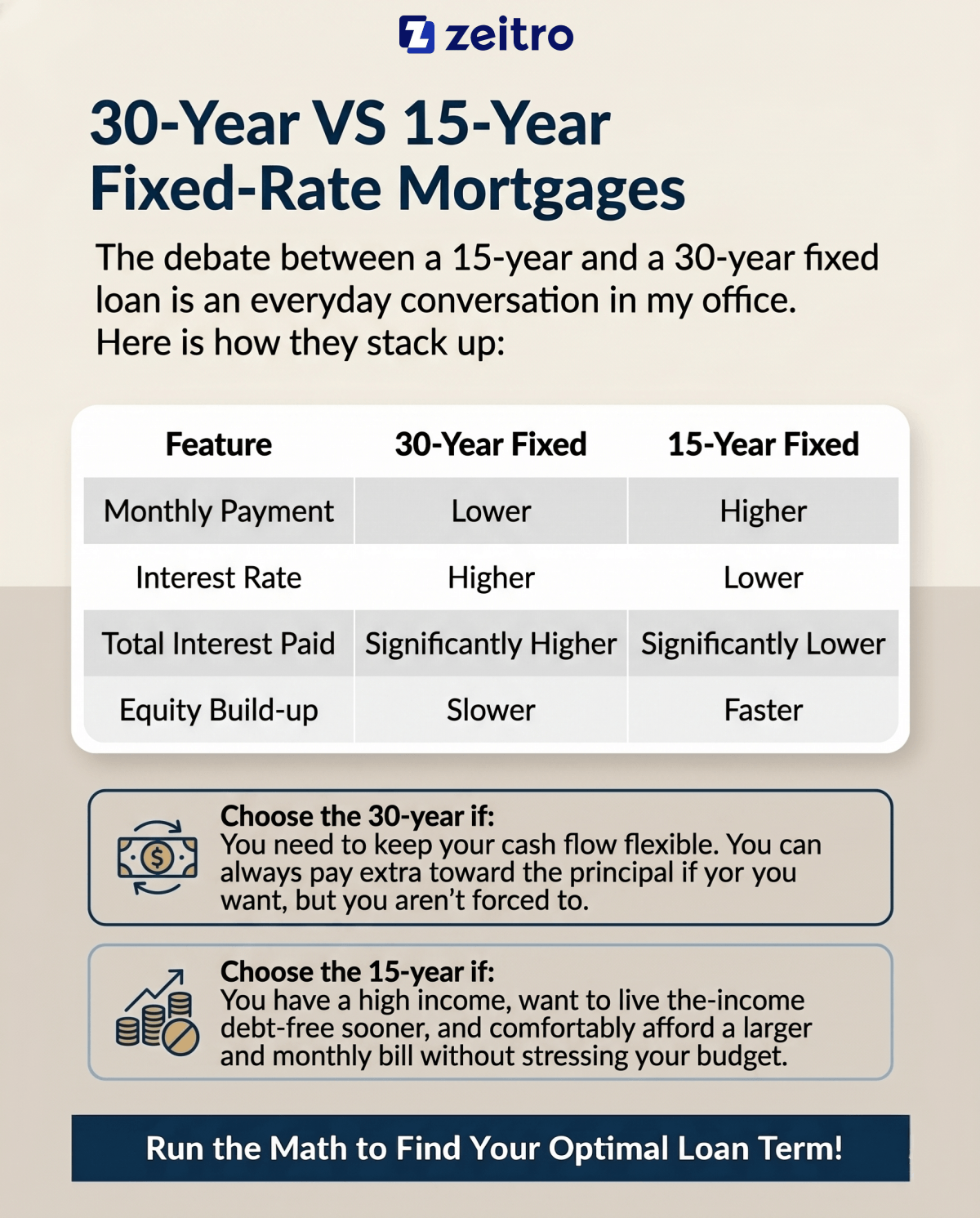

30-Year VS 15-Year Fixed-Rate Mortgages

The debate between a 15-year and a 30-year fixed loan is an everyday conversation in my office. Here is how they stack up:

Choose the 30-year if: You need to keep your cash flow flexible. You can always pay extra toward the principal if you want, but you aren't forced to.

Choose the 15-year if: You have a high income, want to live debt-free sooner, and comfortably afford a larger monthly bill without stressing your budget.

ARMs are best for: Buyers who know for a fact they will sell the house or refinance before the initial fixed period (like 5 or 7 years) ends.

Fixed rates are best for: The vast majority of buyers who want long-term stability and don't want to gamble on future market conditions.

FAQs About Fixed-Rate Mortgages

Q1. Can you refinance a fixed-rate mortgage?

Yes, absolutely. If the market cools down and interest rates drop below your current locked rate, you can refinance to a new, lower fixed-rate loan. Just remember that refinancing involves paying closing costs again, so you'll need to run a break-even analysis.

Q2. Can my monthly payment change on a fixed-rate mortgage?

Yes. While your actual loan principal and interest are permanently locked, your property taxes and homeowners' insurance, which sit in your Escrow account, adjust annually. If local tax assessments rise, your total monthly output will increase accordingly.

Q3. Is it better to pay off a fixed-rate mortgage early?

It depends. Paying it off early saves a massive amount in interest. However, you must weigh the "opportunity cost." If your mortgage rate is 4% but you can earn 8% investing that extra cash, investing is mathematically smarter. Also, check for prepayment penalties.

Q4. How is the fixed interest rate determined?

Your specific rate is a mix of macroeconomic factors, like the 10-year Treasury yield, and your personal financial profile. While I can't control the bond market, your credit score, down payment size, and loan type directly dictate how good a rate we can offer you.

Q5. Are fixed-rate mortgages assumable?

Usually, conventional loans are not assumable. However, government-backed fixed-rate loans, like FHA, VA, and USDA mortgages, often are. This means a qualified buyer can actually take over your remaining loan balance at your original low interest rate when you sell!

Conclusion

As a loan officer, I've navigated just about every market cycle, and the fixed-rate mortgage remains the ultimate tool for financial stability. It takes the guesswork out of homeownership, allowing you to budget with absolute confidence while building equity over time. Whether you opt for a 30-year term to maximize your monthly cash flow or a 15-year term to crush your debt early, locking in your rate is a powerful strategy.

Because everyone's financial fingerprint is unique, there is no universal right answer. I highly recommend chatting with a local, licensed mortgage professional to run a personalized cost analysis for your situation. Ready to see what you qualify for? Reach out to your loan officer today to get started.

Is an Adjustable Rate Mortgage (ARM) right for you? A loan officer explains how ARMs work, their pros, cons, and when to choose one over a fixed rate.

In my years working as a loan officer, Ive seen countless homebuyers feel completely overwhelmed by today's tricky interest rate environment. You aren't alone if you're stressing over monthly payments. Thats why I often recommend looking into an Adjustable Rate Mortgage (ARM).

Put simply, its a home loan where your interest rate is locked in at first, but later floats up or down based on the market. In this guide, Ill walk you through exactly how ARMs work, their pros and cons, and whether this strategy actually makes financial sense for your specific situation.

Key Takeaways

Introductory period: An ARM starts with a lower, fixed interest rate for the first few years before transitioning into a variable phase.

Market-driven: Once the fixed term ends, your new rate is calculated using a baseline Index plus a fixed Margin.

Rate caps: These built-in safety nets limit exactly how high your interest can spike.

Best use case: These loans can be a good fit if you plan to sell the property or refinance before the adjustable period begins.

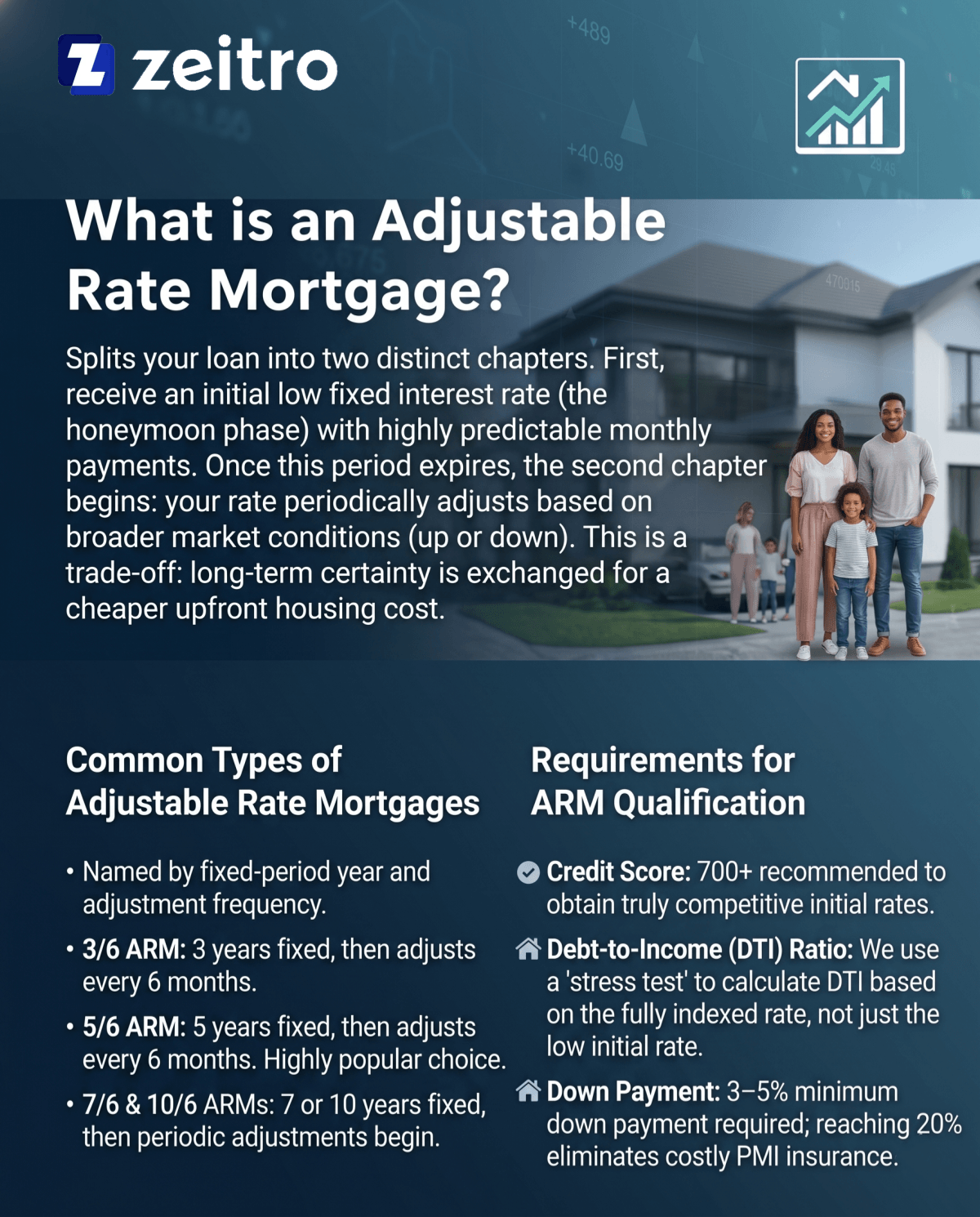

What is an Adjustable Rate Mortgage?

When you sit at my desk and ask for a traditional fixed-rate mortgage, you get the exact same interest rate for 30 years. An Adjustable-Rate Mortgage is fundamentally different. It splits your loan into two distinct chapters.

During the first phase, you receive an initial fixed interest rate, which is often lower than that of a standard fixed-rate mortgage. This introductory interest rate is typically lower than what you'd find on a standard fixed-rate loan, giving you highly predictable, manageable monthly payments right out of the gate.

However, once that initial honeymoon phase expires, chapter two begins. Your rate will periodically adjust based on broader market conditions. If national rates fall, your mortgage payment drops. But if the market heats up, your monthly obligations will increase. That unpredictability is the core tradeoff: you are exchanging long-term certainty for a cheaper upfront housing cost. Its a powerful tool, but as I always warn my borrowers, you have to be prepared for those future rate fluctuations.

Types of an Adjustable Rate Mortgage

Mortgage lenders use a two-number naming system to categorize these loans. The first number tells you how many years the rate is locked, while the second indicates how often it changes afterward. Many modern ARMs adjust every six months and are commonly tied to the SOFR index, although adjustment periods can vary depending on the loan structure.

Here are the most common options I write for clients:

3/6 ARM: Your rate stays the same for the first three years. After that, it adjusts twice a year.

5/6 ARM: You get five years of stability before the biannual adjustments begin. This is currently a very popular choice.

7/6 and 10/6 ARMs: These offer seven or ten years of fixed payments. They act very similarly to traditional 30-year loans but offer a slight discount on the initial interest.

Requirements of an Adjustable Rate Mortgage

Qualifying for a variable-rate loan actually requires jumping through a few more hoops than standard financing. From my underwriting experience, here is what we look for:

Credit Score: While conventional guidelines from Fannie Mae or Freddie Mac technically allow a 620 minimum, youll usually want a score of 700 or higher to get a truly competitive teaser rate.

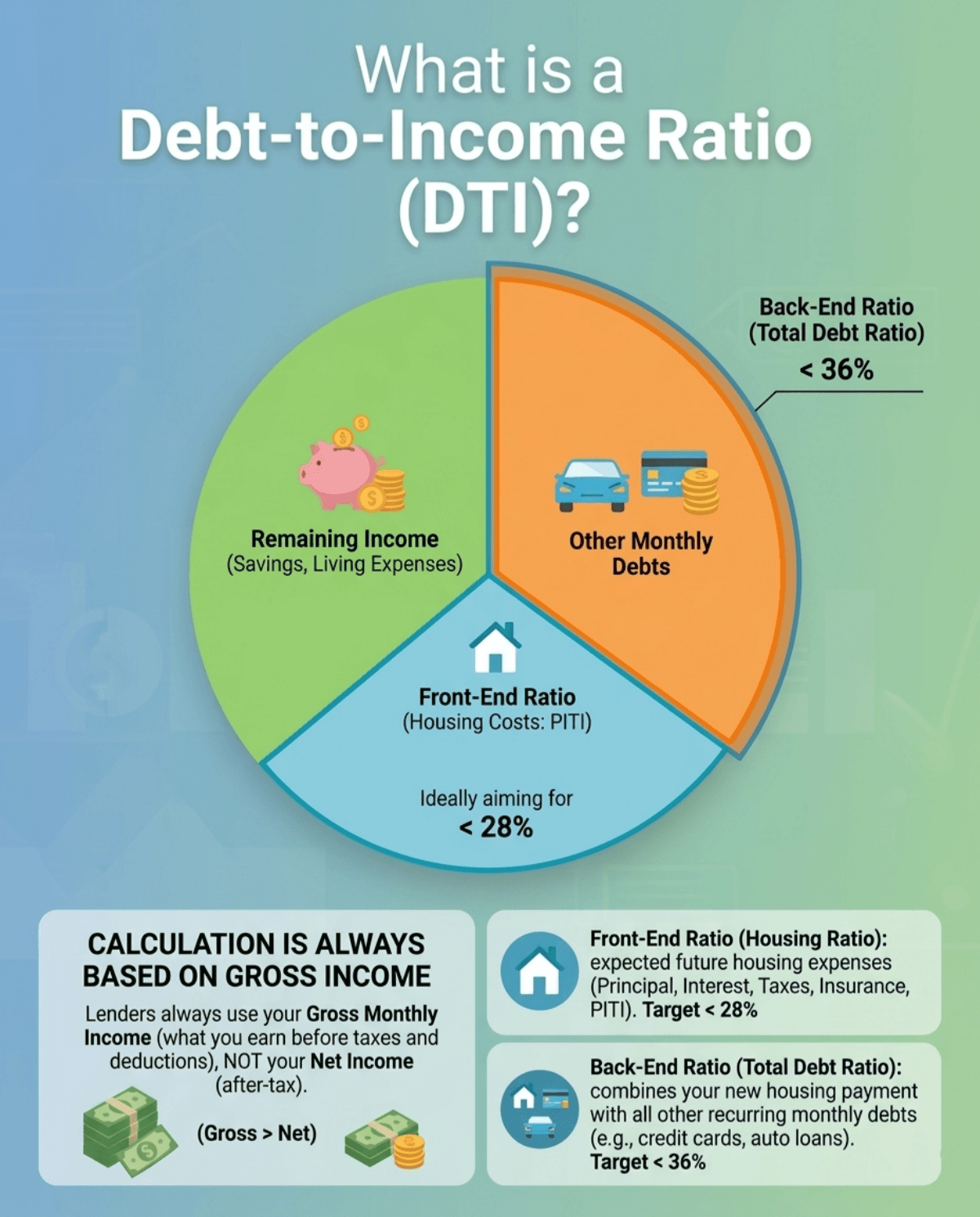

Debt-to-Income (DTI) Ratio: This is where it gets tough. Lenders don't just qualify you based on the low starting rate. We use a "stress test" by calculating your DTI based on the fully indexed rate (the current index plus margin), rather than the initial introductory rate. We want to make sure you won't default if your bill goes up.

Down Payment: You can secure an ARM with as little as 3% to 5% down, though reaching 20% eliminates costly private mortgage insurance (PMI).

How Does an Adjustable Rate Work?

Many homebuyers worry that lenders can just arbitrarily raise their rates. I always reassure them that the math is strictly regulated by your contract.

Once your introductory period ends, we determine your new bill using a very specific formula: Index + Margin = Fully Indexed Rate.

The Index: This is a public financial benchmark reflecting the current US economy. Today, the industry standard is the 30-day average Secured Overnight Financing Rate (SOFR), which fluctuates with market conditions and changes over time.

The Margin: This is the lenders fixed profit percentage, agreed upon when you sign your closing documents. It never changes.

If your margin is 2.75% and the SOFR index hits 3.60%, your new mortgage interest rate becomes 6.35%. It is entirely transparent.

What are ARM Rate Caps?

The biggest fear my clients have is "payment shock", waking up to an unaffordable mortgage bill. Thankfully, variable loans feature strict consumer protections called caps, which act as a ceiling for your rate.

We usually format these as three numbers on your paperwork, like 5/2/5.

Initial Cap (The first 5): Your rate cannot jump by more than 5% during the very first adjustment.

Periodic Cap (The 2): On any subsequent adjustment date, the rate can never increase by more than 2% at a time.

Lifetime Cap (The final 5): Over the entire 30-year lifespan of the debt, your interest will never exceed 5% above your original teaser rate.

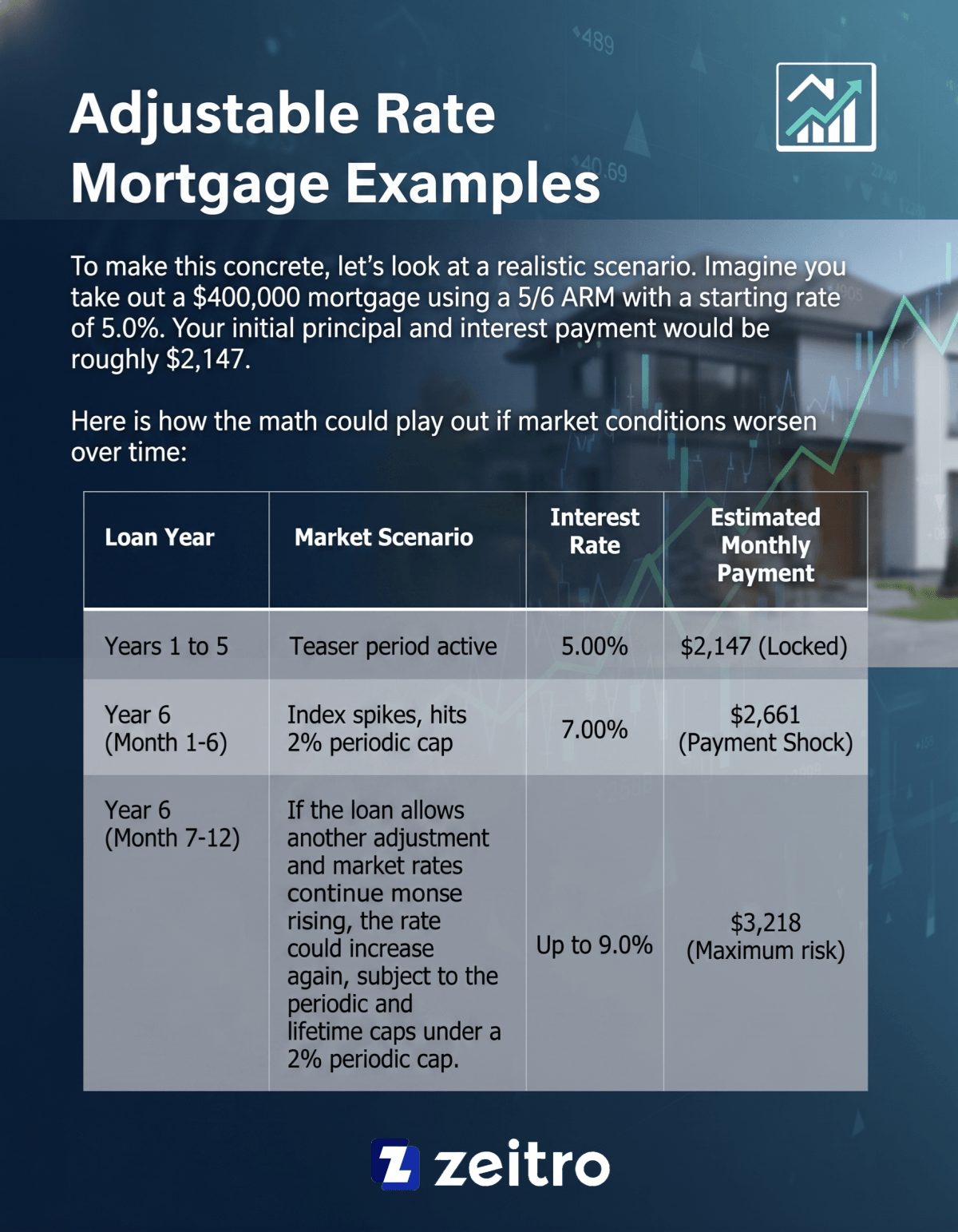

Adjustable Rate Mortgage Examples

To make this concrete, lets look at a realistic scenario. Imagine you take out a $400,000 mortgage using a 5/6 ARM with a starting rate of 5.0%. Your initial principal and interest payment would be roughly $2,147.

Here is how the math could play out if the market gets worse:

As you can see, by the end of year six, your housing cost could increase by over $1,000. This stark contrast highlights why having a solid exit strategy is absolutely crucial.

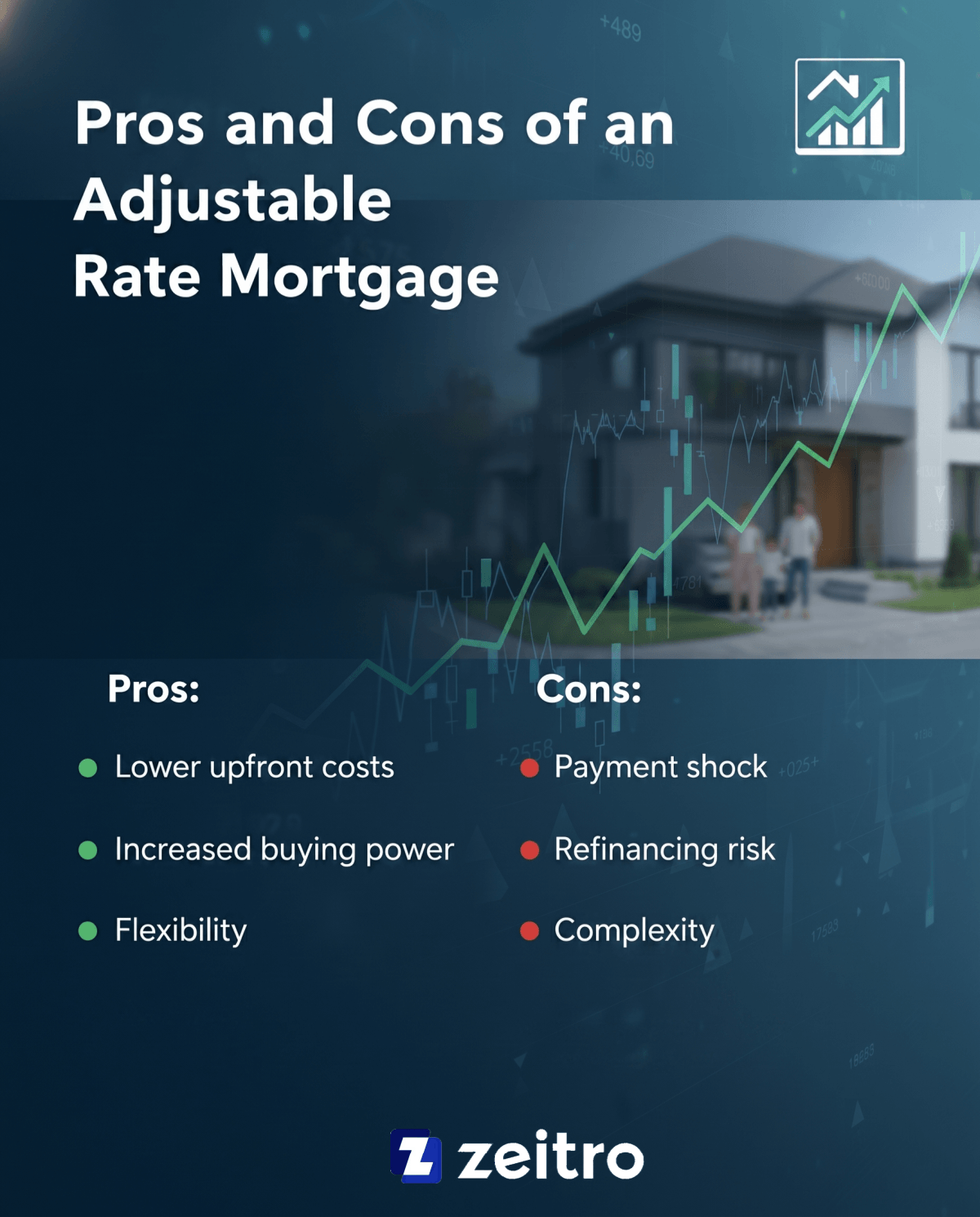

Pros and Cons of an Adjustable Rate Mortgage

As a mortgage professional, I never push a client into an ARM unless they fully understand both sides of the coin. Its a fantastic financial lever, but it's not without its dangers.

Pros:

Lower upfront costs: You secure a cheaper rate than standard 30-year fixed options, saving thousands during the initial phase.

Increased buying power: Lower initial payments mean you might qualify for a slightly more expensive home right now.

Flexibility: Its a brilliant short-term hack if you plan to move quickly or expect a massive boost in your salary down the road.

Cons:

Payment shock: The possibility of drastic monthly bill increases once the floating period begins.

Refinancing risk: If your property value drops, you might not be able to refinance out of the loan before the rate adjusts.

Complexity: The contracts are filled with index margins and cap structures that can be somewhat confusing to manage.

Who are Adjustable-rate Mortgages Best for?

So, when do I actively recommend this route to my borrowers? Generally, I suggest variable financing if you fit into one of these specific profiles:

Short-term homeowners: If you are buying a "starter home" and know for a fact youll upgrade and sell within five to seven years.

Future refinancers: Buyers who expect national interest rates to drop soon and plan to refinance into a fixed mortgage before their teaser period ends.

Aggressive savers: Clients who intend to put extra cash toward their principal every month to pay off the debt early.

High-trajectory earners: Medical residents or young professionals who reasonably expect significant income growth by the time higher payments begin.

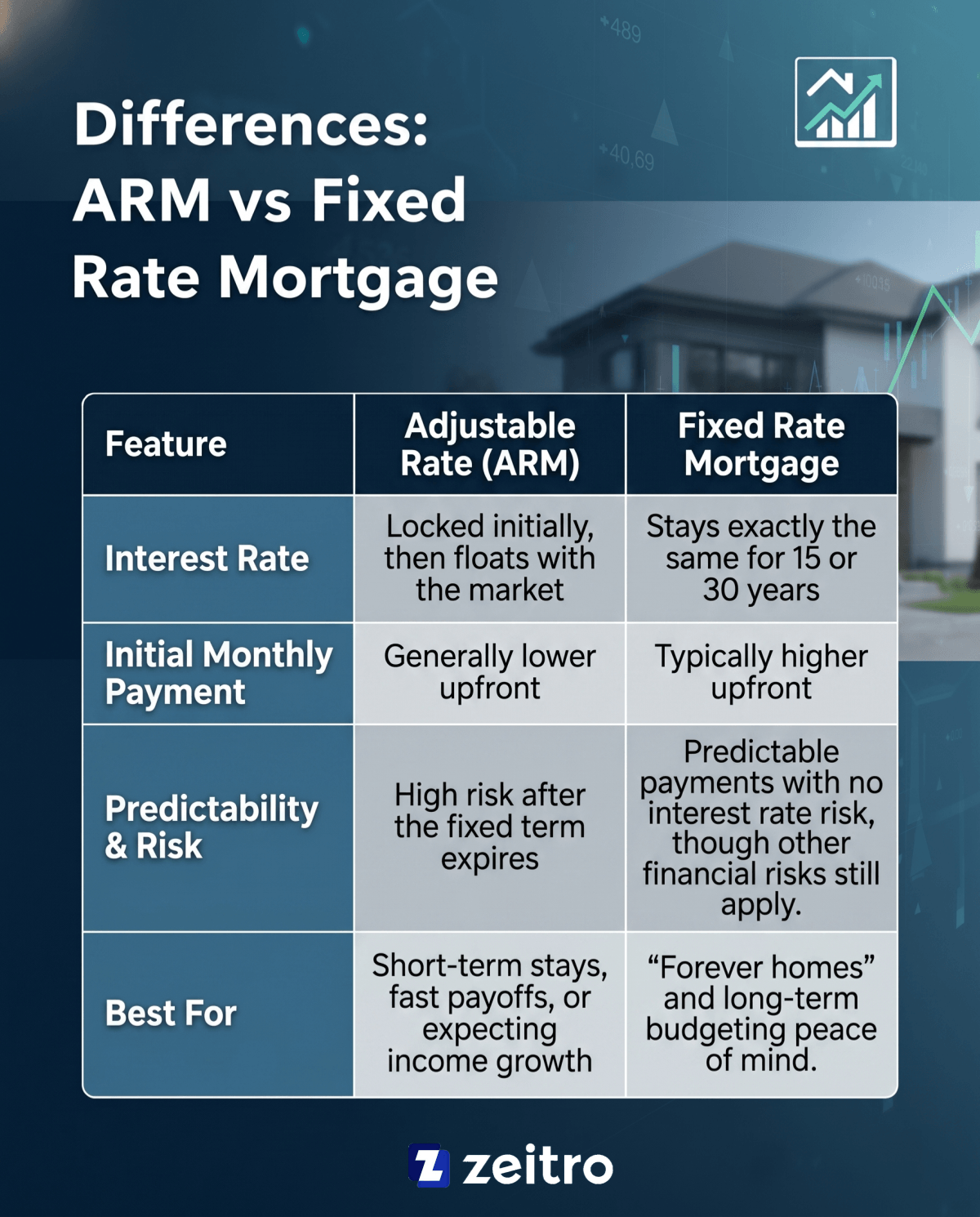

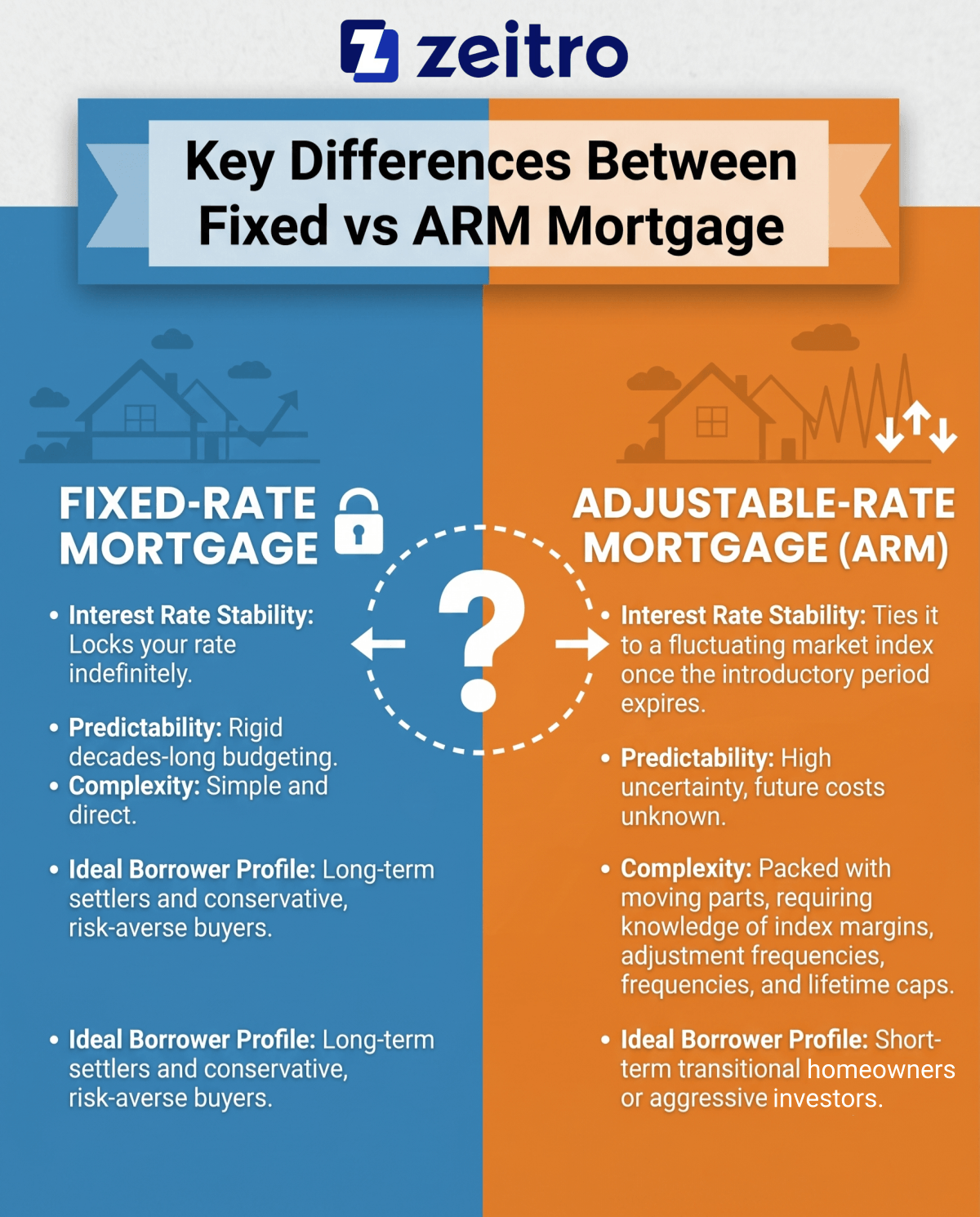

Differences: ARM vs Fixed Rate Mortgage

Making the final call between variable and fixed financing usually comes down to your personal risk tolerance. I created this simple comparison to help my buyers weigh their options quickly:

There is no universally "better" choice here. It entirely depends on your timeline and how well you sleep at night knowing your payment could shift.

FAQs About Adjustable Rate Mortgages

Q1. What are the downsides of an adjustable-rate mortgage?

The biggest drawback is unpredictability. Once your introductory period finishes, a high-rate environment can trigger "payment shock." If you aren't prepared for your monthly housing bill to potentially increase by hundreds of dollars, this financial product can put immense strain on your budget.

Q2. How to read ARM labels?

Loan labels use two numbers, like a "5/6 ARM." The first number (5) means your introductory interest rate is locked for five years. The second number (6) means that after those five years, your rate will adjust every six months based on current market indices.

Q3. Can I refinance an ARM into a fixed-rate mortgage?

Yes, absolutely. I frequently help clients use an ARM for the initial savings, then refinance them into a stable fixed-rate loan before their first adjustment hits. Just remember that refinancing requires a new appraisal and closing costs, so you need enough home equity to qualify.

Q4. Are ARM loans harder to qualify for than fixed-rate loans?

Yes, in many cases. Lenders won't just look at whether you can afford the cheap teaser rate. We underwrite your file using the fully indexed rate, the highest possible payment after adjustments, to ensure your debt-to-income ratio can handle a worst-case scenario.

Q5. What happens when my ARM adjusts?

You won't be caught completely off guard. Your lender will mail you a written notice weeks before the adjustment date. Your new rate is calculated by adding your contract's Margin to the current public Index, strictly limited by your established rate caps.

Conclusion

At the end of the day, an Adjustable Rate Mortgage is essentially trading future uncertainty for immediate financial relief. Its a highly strategic move that works beautifully for the right person, but it can be devastating if you don't have a solid exit plan.

Before signing anything, I strongly encourage you to run some numbers through a mortgage calculator to see your worst-case scenarios. Better yet, sit down with a local, trusted loan officer who can evaluate your unique income trajectory and timeline. With the right guidance, you can use these tools to confidently build your wealth.

Confused by fixed vs adjustable rate mortgages? Read our complete comparison guide to understand ARMs, fixed rates, and find the smartest option for you.

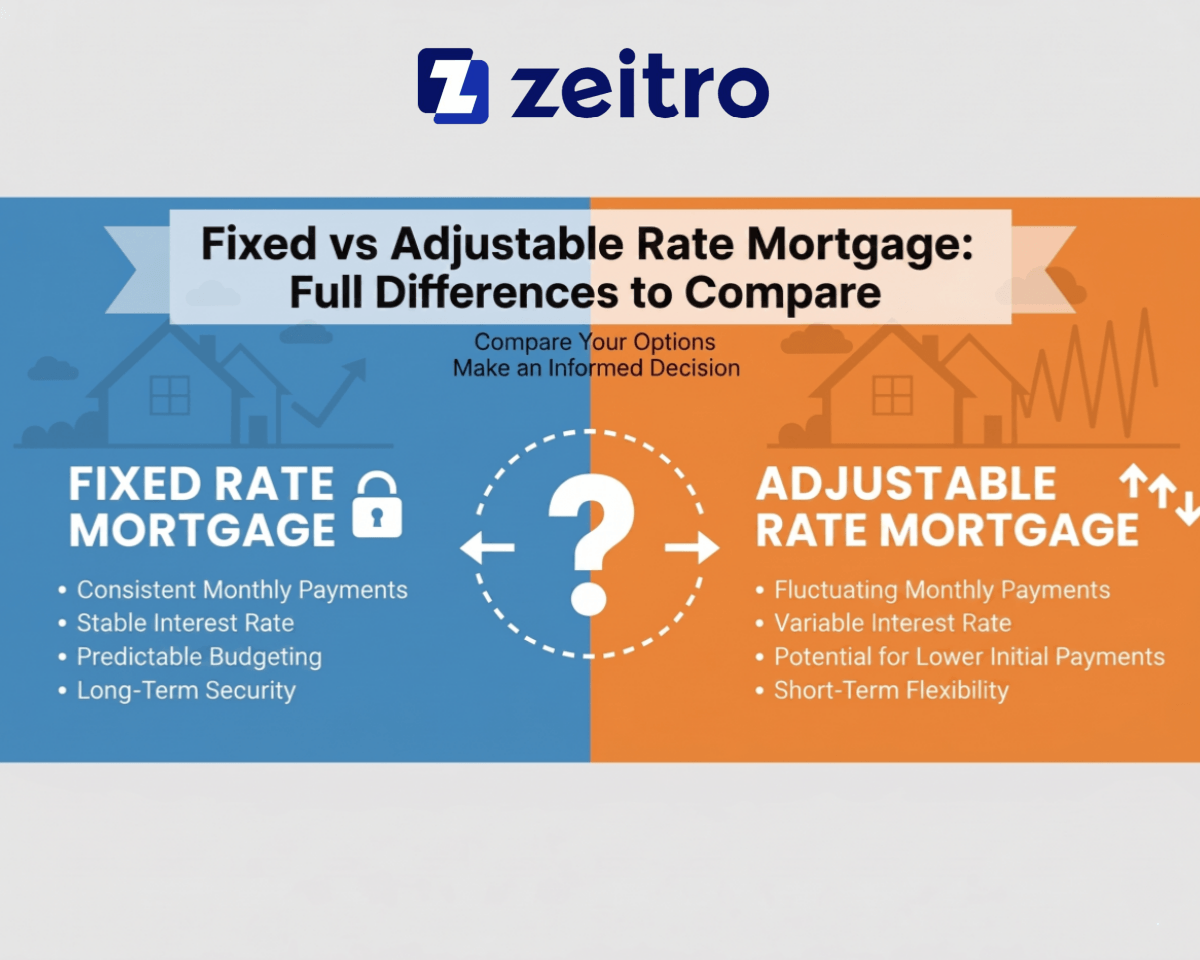

Choosing the right mortgage type can feel like navigating a stressful maze of financial jargon. Trust me, I've been there. If you pick the wrong one, you might overpay by thousands or face terrifying payment spikes later. That is why clearly comparing a fixed vs adjustable rate mortgage (ARM) is so critical.

In this guide, I will break down their full differences to help you make an informed financial decision. After reading, I highly recommend getting a free consultation with local loan officers for personalized advice.

Key Takeaways

Fixed-Rate Mortgages offer rock-solid stability. Your principal and interest payments never change, making long-term budgeting incredibly predictable.

Adjustable-Rate Mortgages (ARMs) provide cheaper upfront costs during an introductory period, but carry serious payment shock risks when market rates adjust later.

How to Choose depends entirely on your timeline and risk tolerance. If you plan to move within a few years, an ARM might save cash. For long-term stays, lock in a fixed rate.

What is a Fixed Rate Mortgage?

I like to explain a fixed-rate mortgage as the ultimate "set it and forget it" financial tool. Simply put, your interest rate and your monthly principal and interest payments remain fixed for the life of the loan, although total monthly housing costs may still change due to taxes and insurance, whether you choose a 15-year or a 30-year term.

Even if the housing market crashes or national interest rates soar to historic highs, your monthly bill stays exactly the same. When I was deciding on my own financing, the peace of mind this brought was unmatched. It offers unparalleled stability for homeowners who want zero surprises.

Protection from inflation: Your rate is locked, shielding you from future interest rate hikes.

Easy to understand: There are no complex formulas or hidden adjustment clauses.

Perfect for long-term living: Ideal if you plan to stay in your home for decades.

Cons:

Higher initial rates: They generally start with higher interest than an ARM.

Refinancing costs: If market rates drop, you will incur closing costs when refinancing, though these can sometimes be rolled into the loan or offset by accepting a slightly higher rate.

Stricter qualification: A higher initial rate might slightly lower the total loan amount you get approved for, assuming the same income level.

What is an Adjustable Rate Mortgage (ARM)?

An adjustable-rate mortgage (ARM) uses a two-part loan structure. It begins with an "introductory period" featuring a fixed, significantly lower interest rate. You'll usually see this advertised as a 5/1 or 7/1 ARM. The first number represents how many years the rate stays fixed, while the second indicates how often the rate adjusts afterward.

After the initial phase ends, you enter the "adjustment period," where your interest rate floats based on a broader market index. While responsible lenders apply rate caps to prevent your interest from rising infinitely, an ARM still exposes you to noticeable interest rate risk over time.

Pros:

Significantly lower starting rates: Early payments are much cheaper, easing initial financial pressure.

Great for short-term plans: If you plan to sell or move before the adjustment period kicks in, it's highly cost-effective.

Automatic drops: If the market dips during your adjustment phase, your rate may decrease during adjustment periods if the underlying index falls, subject to rate floors and adjustment terms.

Higher buying power: The lower initial payment might help you qualify for a slightly more expensive home.

Cons:

Payment shock: Your monthly payments could skyrocket once the fixed period ends.

Highly unpredictable: Long-term budgeting is less predictable, though rate caps allow borrowers to estimate worst-case scenarios.

Complex terms: Understanding the index margin and rate caps can be confusing.

Market risk: Even with rate caps, you are betting against future market trends.

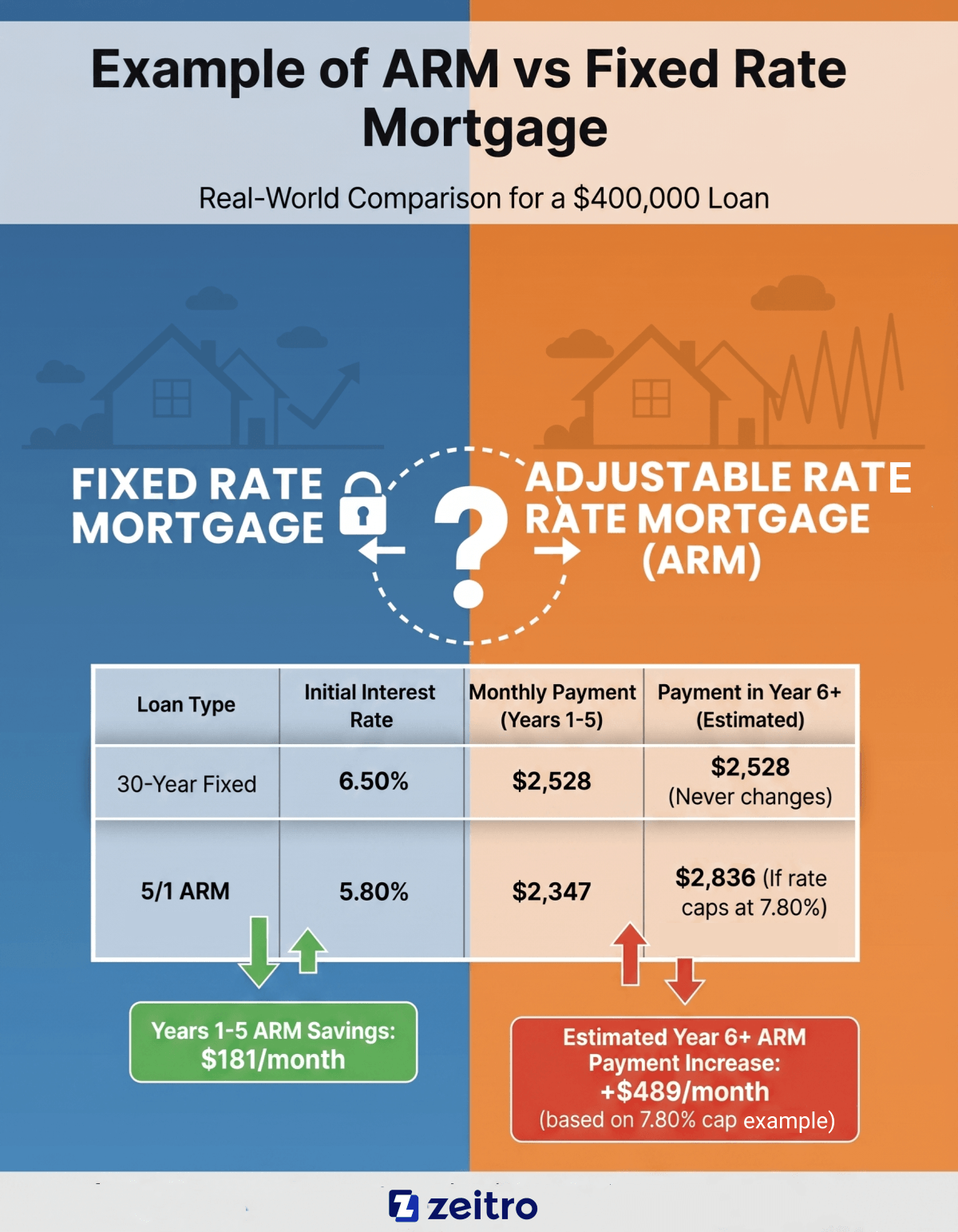

Example of ARM vs Fixed Rate Mortgage

To see how this plays out in the real world, let's look at the math. Imagine you are borrowing a $400,000 loan with a 30-year term. For illustration, assume a 30-year fixed rate around 6.5% and a 5/1 ARM at 5.8%, though actual rates vary daily by market conditions and borrower profile. For the first five years, the ARM saves you roughly $181 per month.

That's over $10,800 kept in your pocket! However, look what happens in Year 6. If the market index rises and your ARM adjusts up to 7.80% ((a typical ARM may include caps such as 2% per adjustment and a lifetime cap, though exact structures vary by loan)), your monthly payment could increase significantly (e.g., by several hundred dollars), depending on the new rate, remaining balance, and loan terms.

Disclaimer: For illustrative purposes only. Actual mortgage rates fluctuate with daily market conditions and your personal credit score. Always consult a professional before making a decision.

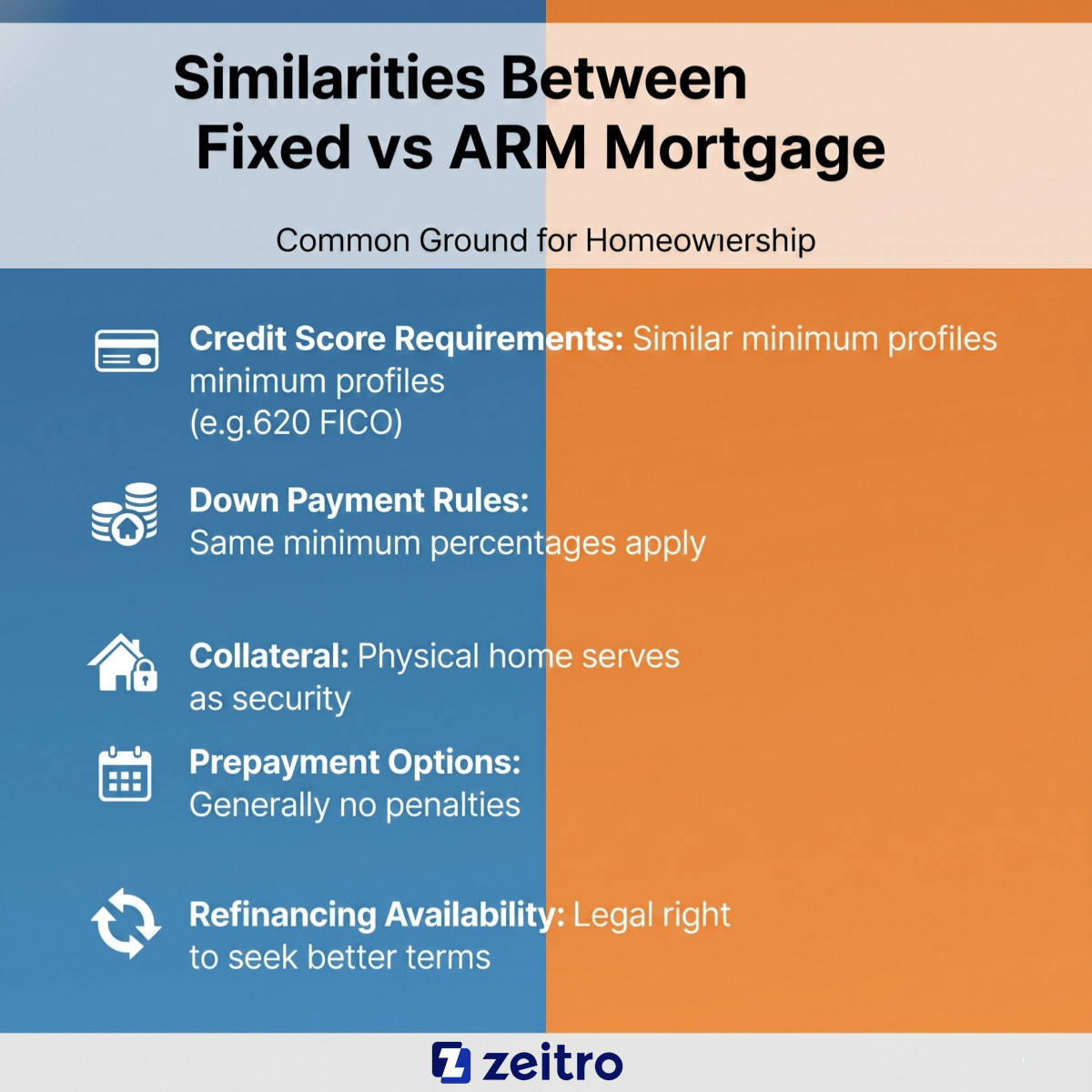

Key Differences Between Fixed vs ARM Mortgage

When deciding between these two paths, it helps to step back and look at the broader dimensions. I've found that the essence of the difference comes down to one question: How much future uncertainty are you willing to tolerate in exchange for cheaper costs today? You aren't just choosing a rate. You are choosing a risk profile. Here is a breakdown of the deepest contrasting factors.

Interest Rate Stability: A fixed loan locks your rate indefinitely. An ARM ties it to a fluctuating market index once the introductory period expires.